-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Regional Strategy – China: Bottoming Out, Overweight Equities

Thursday, November 15, 2012  13510

13510

Regional Strategy – China

Weekly Special - 2333 Great Wall Motor

Head of Research China's top picks are: Brightoil (933.HK) and CMBC (1988.HK).

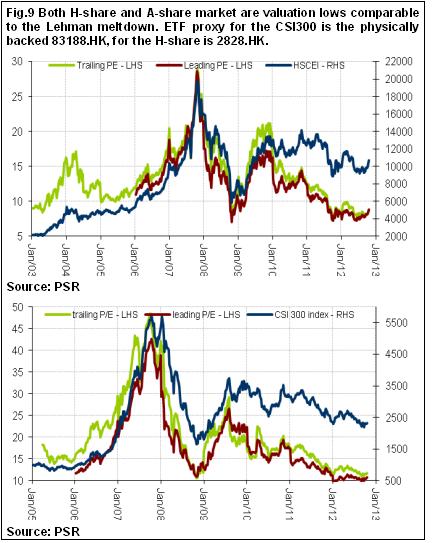

We are positive and overweight H and A shares, favouring A shares. PhillipETF recommends H-Share Index ETF (2828.HK) as a proxy for the H-share HSCEI and ChinaAMC CSI 300 Index ETF (83188.HK) as a proxy for the A-share CSI300.

China Bonds: Neutral/Overweight for short term.

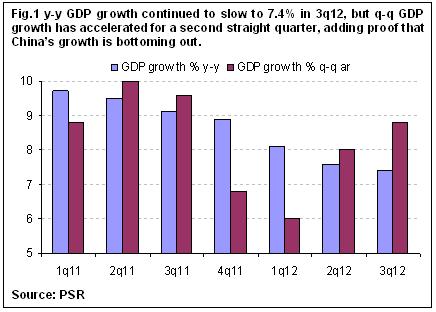

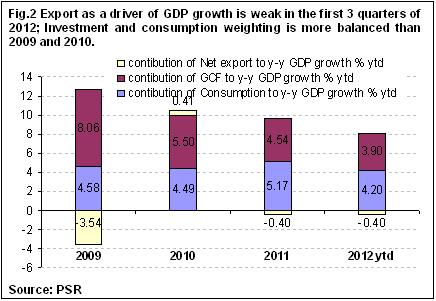

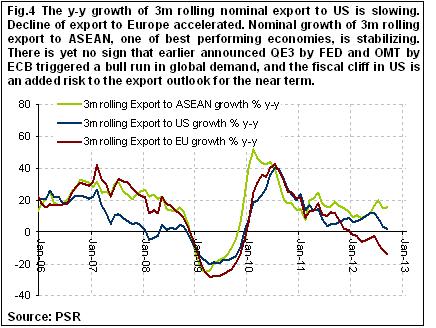

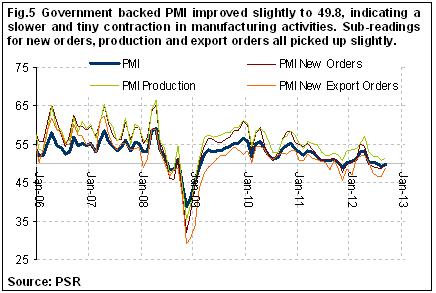

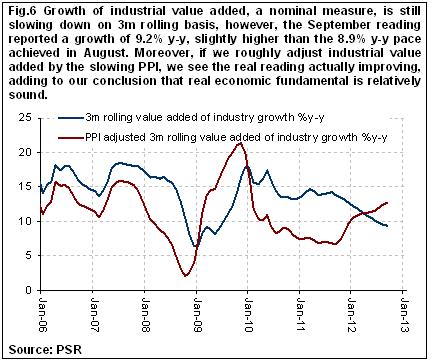

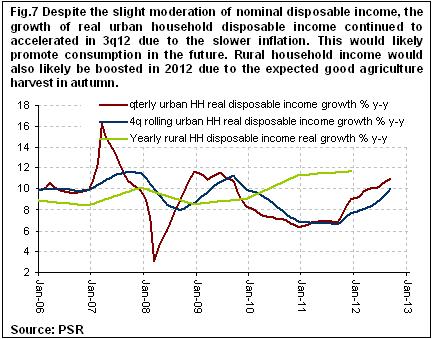

China's GDP growth has slowed down to 7.4% y-y in 3q12, compared to the 7.6% y-y growth in 2q12. However, on q-q basis, GDP growth has accelerated for two consecutive quarters, reporting 2.2% q-q in 3q12, higher than the market estimated 2.0% q-q and the 1.8% q-q growth achieved in 2q12. FAI and Retail sales growths have achieved moderate accelerations in both nominal and real terms. FAI rose by 20.5% y-y ytd in September, compared to the 20.2% y-y ytd pace in August. Retail sales growth accelerated to 14.2% y-y in September, faster than the 13.2% y-y pace in August. External demand would likely remain weak in the near term due to the prolonged Europe crisis and a tentative US as the fiscal cliff approaches – despite the September export data achieved a relatively significant pickup in growth due to pre Christmas order, reporting 9.6% y-y gain, compared to 2.0% y-y gain in August, on a smoothed %y-y 3mma basis, exports actually declined. September Statistics for industrial production and manufacturing PMI also showed moderate improvement.

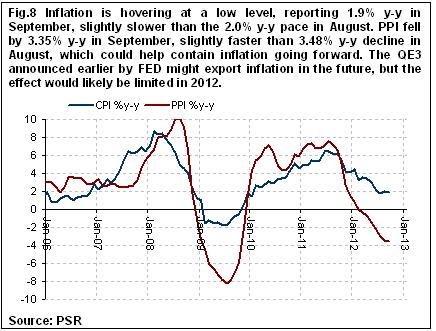

The earlier announced infrastructure project investment, which summed to over 1 trillion RMB, will help keep growth on even keel. The government's engagement in transforming a business tax system to an appreciation tax system will help improve enterprises` income. Inflation remained at a low level in September, reporting 1.9%, compared to 2.0% in August. Property price also remained tame: In September only 12 out of 70 cities saw yearly increase in new home price, and 55 saw decrease, compared to 15 and 53 respectively in August. Tame inflation and property price growth does grant scope for further monetary loosening, but a surge in the banking system's foreign currency exchanging for RMB with PBoC might have already done the job for extra liquidity. We do not rule out the possibility of a further 25 bps cut in RRR in the remaining months of 2012. We maintain our forecast of 7.8% y-y GDP growth and 2.5% inflation for 2012.

For the Equity market, as we have been guiding our China strategy reports, we see attractive valuations in both H share and A share market, whose P/Es are at or close to their historical low. Therefore, it is a good time to adopt a buy and hold strategy. We were Overweight on a 3 to 5yr horizon but Marketweight on a shorter horizon due to a previously unclear bottoming. However, due to the recent better-than-expected macro data, we are of the view that the market would gradually regain confidence, and a rally is likely on its way. In fact, the H-share HSCEI index has trended up since September and the A share CSI300 index is only showing a nascent sign of rally. As we hold a positive view for the short term and expect the sentiment discrepancy between H and A share market to correct (thus favouring CSI300 index slightly more), we are simply Positive on an absolute basis both H and A shares, and also Overwieght them relative to global peers. Bond market is a neutral/overweight against peers for short term perspective. And we hold a positive outlook for CNY in the long run.

Economic Metrics and Growth Outlook:

Growth & Inflation Forecast:

As we have expected, the earlier announced infrastructure projects and efforts in boosting consumption by the government has started taking effects. We maintain our forecast for the whole year GDP growth at 7.8% y-y with inflation of 2.5% over the year.

Asset Strategy

Equity Market: As we have been guiding our China strategy report, we see attractive valuations in both CSI 300 and HSCEI indices due to their close to historical low leading and trailing P/E ratios, even lower than the Lehman crisis. But due to an inconclusive economic bottoming, we have been recommending Overweight on valuation grounds only for investors with a longer term 3-5yr perspective, Marketweight for everyone else. But now, from a shorter term perspective, the well-performing macro data in September would lend support to a positive outlook (see economic metrics part above), and we expect the market would gradually regain confidence. Therefore, we are turning positive on China on an absolute basis and are simply Overweight on both HSCEI and CSI 300 indices. As both indices have underperformed relative to global peers, we do expect them to outperform in a play on catchup.

As a proxy to the CSI300, the main A-share benchmark index, we recommend the physically backed ETF, ChinaAMC CSI300 ETF (83188.HK). For H-share we recommend H-Share Index ETF (2828.HK) which tracks HSCEI. Over the long term, the two indices track each other well. However, for the near term, we observe a discrepancy in two indices: The HSCEI index has been trending up since early September, while the rally for CSI300 index has just completed a nascent form. The discrepancy is attributable to the different sentiments over the two markets between international investors and China's local investors. We are holding a positive outlook for the near term and expect the discrepancy to somewhat correct itself, therefore we favour CSI300 index slightly more over HSCEI. In addition, the HSCEI ETF (2828.HK) is HKD dominated while CSI300 ETF (83188.HK) is CNY dominated. As HKD is pegged to USD, the open-ended QE3 would likely depreciate HKD, meaning potential further haircut on the return from the H-share investment.

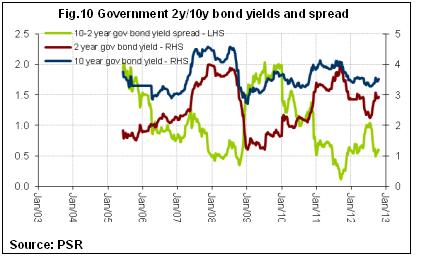

Bond Market: We observe some pickups in the 2 yr and 10 yr government bond yield, reflecting that the market is correcting its expectation about further monetary loosening. The tame inflation and property price do grant the central bank enough scope for further monetary loosening, but the recent surge of banking system's exchanging foreign currency for RMB with central bank, which is a way PBoC uses to inject RMB liquidity, might have done the work. That reduces our expectation for RRR cut in the very near term. Despite this, we still do not rule out the possibility of a further 25 bps cut by the end of this year as the economy is still consolidating its strength.

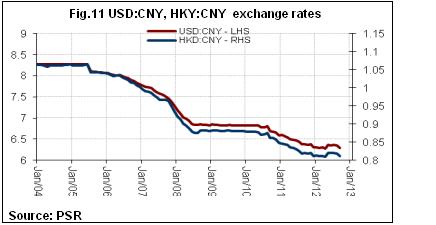

Currency Outlook: We hold a positive outlook for CNY against major trading currencies in the long term as CNY is still moderately undervalued. For the near term, the government has an incentive to maintain CNY stable or weak to bolster the nation's faltering export growth. Therefore, we assign a neutral rating to CNY against major trading currencies in the short term. To sum up, we expect CNY exchange rate to remain relatively stable in the short term, but tilt upward in the long run. As for HKD, which is pegged to USD, the open-ended QE3 would likely depreciate HKD against other major trading currencies.

STOCK PICKS:

Head of Research China's top picks are: Brightoil (933.HK) and CMBC (1988.HK).

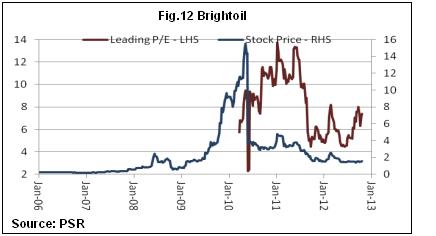

Brightoil (933. HK)

Brightoil includes four core business divisions: offshore bunkering, oil storage, tanker transport, upstream exploration and production. International supply and offshore bunkering are main sources of the corporate income, and fuel supply increased from 1.8 million tons in 2009 to 8.9 million tons in 2011, with rapid business growth. The business income of offshore bunkering in 2011 reached HKD39.5 billion, substantially increasing by 624% over 2009.

Brightoil extended its offshore bunkering business to global nine key ports over the past four years. Singapore and China are major areas for the Company to provide offshore bunkering and oil sales for international fleets, which reflects the Company's great efforts to extend its port business in Singapore and China. Currently Brightoil is Singapore's second largest offshore bunkering provider. the Company revenue in Singapore stood at HKD29.9 billion in 2011, which accounted for 75% of the group gross revenue.

Brightoil and Petro China are cooperating to develop Dina 1 gas field in Xinjiang Tarim Basin Tuzi gas field. Currently the gas field has completed final testing, and is expected to come on stream in Q4 2012. Daily output of natural gas and condensate will be 550,000 m2 and 25t respectively, beyond previously expectation. Dina 1 gas field will be the start of upstream business development for Brightoil, and future larger Tuzi natural gas field will provide sufficient and steady cash flow income for the Company, to become the core drive for the corporate profit growth.

Brightoil income soared by 190% to HKD36.3 billion in H1 2012 as a result of sharp increase in the offshore bunkering business and oil product trading. Gross margin declined by 5 percentage points to 3% mainly because the supply port extended overseas, causing cost rise and increasing proportion of oil trade with low gross margin. Profits attributable to shareholders stood at HKD965 million, increased by 64% year-on-year. However, the Company's net profit growth mainly came from HKS794 million, increased fair value of financial derivatives, while net margin of main businesses substantially declined.

Brightoil businesses cover offshore bunkering, oil storage, marine transport and upstream natural gas, nowadays with absence of comparative listed companies. In combination with valuation level of oil exploration, port and oil transport companies, we grant Brightoil 10.4-time expected P/E in 2013, and 12-month target goal is HKD1.88, hence “buy” rating granted.

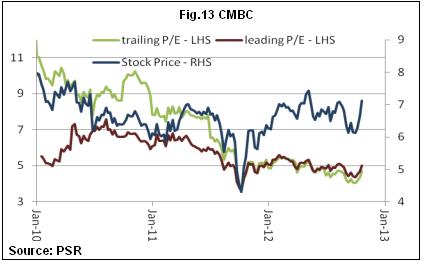

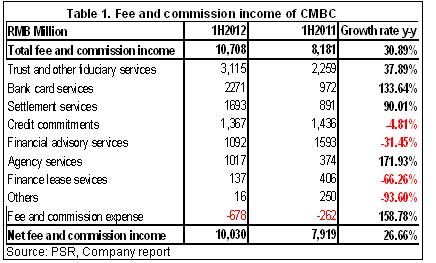

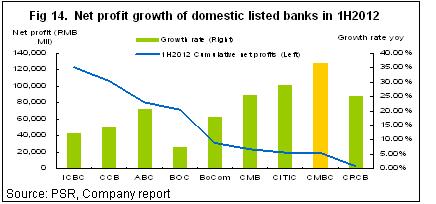

CMBC (1988.HK)

As at the end of 1H2012, net profits of CMBC (or the Group) recorded to RMB19.053 billion, increased by 36.89% y-y, better than our previous expectation.

The Group's total assets increased by 16.37% to RMB2.59 trillion compared with the end of 2011, equivalent to BVPS of RMB5.28 with the growth rate of 8.87%.

One of strong spots of CMBC's business is micro lending. In 1H2012, the Group's total loans decreased from the affection of market environments, but micro lending still kept increasing, which recorded to RMB253.041 billion with the growth of 8.03%, and the portion of such loans to total personal loans increased from 64.33% in 2011 to 65.29%.

Due to bear markets in internal and external economic environment, domestic enterprises, especially for small and medium-sized enterprises are facing more challenges in operation, which caused the quality of loans to deteriorate, and the Group's NPL ratio started to go up from 0.63% in 2011 to 0.69% in 1H2012, but still kept in a low level.

CMBC was downgraded by several large international investment banks because they concerned about its future development, the price was shorted and touched the annual lowest point as HK$5.35 in September. After that, the major shareholders of CMBC continued to increase their holdings in order to stabilize the price. The bank's management also hold the meeting to explain the operating performance to investors for removing the doubts in the market.

For recent activities of investors for shorting CMBC's shares, our view is that the business of CMBC still continues to develop stably with strong profit growth on fundamentals. Micro lending is only small part of total loans although it continued to increase. It's not only CMBC alone, but all banks are facing the deterioration of the quality of loans due to systematic risks from current bear markets, additionally, NPL ratio of CMBC is still quite low and would be controlled even it was expected to increase continually in future.

Therefore, overall, considering strong profit growth and sharp decrease of share price recently, we upgrade CMBC to Buy with 12-m target price of HK$7.30, 17.7% higher than the latest closing price and equivalent to P/E3.9x and P/B0.97x in 2013 respectively. The valuation now is quite attractive.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()