-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

CATL (300750.CH) - King of Power Battery Industry, expect to keep benefitting from Matthew's Effect

Wednesday, February 26, 2020  14368

14368

CATL(300750)

| Recommendation | Buy |

| Price on Recommendation Date | $154.410 |

| Target Price | $185.300 |

Weekly Special - 002050 Sanhua

Investment Summary

Company profile

CATL is a leading power battery system supplier in the world and focuses on R&D, manufacturing and sales of power battery systems and energy storage systems for new energy vehicles. The main business includes power battery system, energy storage system and lithium battery material system (mainly ternary precursor). Specially, the power battery system includes battery core, module and battery pack, which are applied to passenger vehicles and commercial vehicles. In addition, the Company also entered into battery recovery business by acquiring Guangdong BRUNP, invested in holding foreign lithium mine enterprises to bind raw material suppliers, and achieved closed-loop layout of upstream and downstream industry chains.

Shareholding Structure

The sponsor shareholders of the Company and employee holding platform accounted for 59% of the Company's shares, with relatively concentrated shares and stable shareholding structure. The Company launched equity incentives three times in 2015, 2018 and 2019, with employees deeply bound to interests of the Company.

Financing Overview

The Company was established in 2011. After changing into a joint-stock company in 2015, the Company obtained a total capital of RMB16.28 billion through eight rounds of financing. The Company listed on IPO in June 2018 and raised RMB5.46 billion to construct 24GWh power battery new capacity project; in June 2019, the Company issued RMB10 billion of corporate bonds to further maintain orderly progress of capacity expansion.

History

The Company was born out of power battery business department of ATL, the world leader in consumer batteries (polymer lithium batteries) and Apple's mobile battery supplier. At the beginning of establishment, the Company undertook the technology accumulation, manufacturing experience and brand channels in consumer battery of ATL. Depending on the first order in 2012 and successful cooperation with BMW Brilliance, the Company became the only domestic manufacturer to enter into power battery supply chain of multinational automobile enterprises, and became famous at that time.

Starting from 2014, due to vigorous support of the country for new energy vehicle industry chain and sharp increase of domestic lithium battery demand, the Company has been able to rapidly grow. Judging from the shipments, CATL has ranked the first in the world from 2017. The installed power battery capacity in China reached 56.9GWh and 62.2GWh in 2018 and 2019, with CATL of 23.53GWh and 31.71GWh, respectively. Its market share was 41% and 51%, and the gap between the second place BYD (20% and 17%) and the third place Guoxuan Hi-Tech (5% and 5%) was widening.

Low Customer Concentration for Dispersing Risks

For customer structure, the Company almost covered all mainstream car enterprises: Domestic commercial vehicle leader YUTONG, passenger vehicle leaders SAIC, GAC and Geely, as well as new comers as NIO and Weltmeister. In terms of overseas customers, the Company has cooperated with BMW for a long time and is also the supplier of VW, Daimler, Toyota, Honda and Volvo. Recently, the cooperation agreement signed with Tesla was announced. Compared with competitors Samsung and Panasonic, customers of CATL are distributed more dispersedly, which is conducive to dispersing risks.

Technical Leading Advantages with Obvious Cost-Scale Effect

In recent years, the scale of CATL increased continuously with further outstanding technical advantages, thus resulting in gradually appeared scale effect and obvious competitive advantages. Currently, the power battery cost of the Company has decreased to RMB0.75/Wh, mainly due to dilution of fixed costs by scale effect and increase in automation rate, besides the decrease in raw material price.

1. Technical advantages: Early synergy with ATL improved R&D efficiency. Then, the Company also obtain efficient cash for high R & D input through capital market financing, enabling new product design and technological innovation, and the energy density of its battery increased year by year. As of H1 2019, the Company had a total of 4,678 R&D personnel, accounting for 17% of employees. R&D expenditure accounted for 7% of total revenue, and was fully expensed. The Company and its subsidiaries had 1,909 domestic patents and 59 overseas patents, with a total of 2,571 patents under application.

2. Scale-cost effect: Due to excellent performance, the products of the Company were very popular, and the number of matching vehicle models was far ahead of peers. Demand and capacity expansion formed a virtuous circle. The capacity of the Company increased from 7GWh in 2016 to approximately 40GWh in 2019. The Company has production bases in Ningde, Qinghai and Liyang at present, and begins to establish its first overseas production base in Germany. The Company plans to achieve a total capacity of 150GWh to 160GWh in 2022, with accelerating capacity expansion.

In general, we expect that the unit cost of products of the Company has room for further reduction, mainly due to technical upgrading and forward-looking layout brought about by R&D investment, scale effect brought about by production increase, supply chain management, equipment localization substitution, as well as labour efficiency improvement.

Healthy Financial Indicator Leading Industry

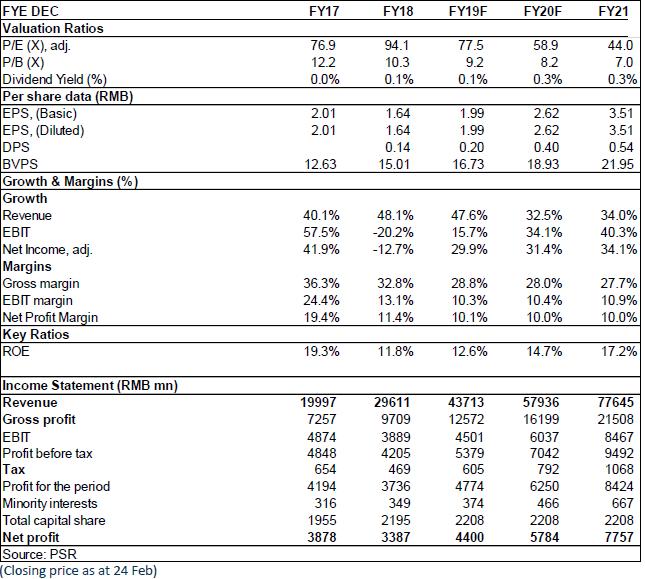

Depending on increase in shipments, the result of CATL also showed explosive growth. The revenue increased 32-fold from RMB890 million in 2014 to RMB29.6 billion in 2018; the net profit attributable to the parent company increased 61-fold from RMB54.4 million to RMB3.39 billion.

Meanwhile, the financial indicators of the Company were sound. The gross margin from 2014 to 2018 was 25.7%/38.6%/43.7%/37%/32.8%, respectively. The decrease since 2017 was mainly due to price reduction caused by subsidy decline, but still 10 ppts higher than that of competitors. In terms of solvency, the debit ratio continuously increased due to rapid expansion, but still lower than average level, at a reasonable ratio. The Company had strong bargaining power to the upstream and downstream, which guarantees good cash flow. Net cash flow from operating activities was approximately twice that of interest-bearing debts, cash in hand was approximately five times that of interest-bearing debts, and balance sheet was strong.

Investment Thesis

At present, the electric vehicle policies of many countries in the world especially European were accelerated. Large car manufacturers would accelerate their new energy plans. With continuous expansion of follow-up scale and release of bonuses for engineers, the cost control advantages of leading enterprise would be highlighted, and power battery industry is expected to show a pattern that the strong would get stronger and stronger. CATL would benefit deeply from the global electrification trend and may exceed market expectations. Risks are unexpected sales volume of electric vehicles, sharp increase in raw material price or sharp decrease in product price.As for valuation, we expected diluted EPS of the Company to RMB 1.99/2.62/3.51 of 2019/2020/2021. And we accordingly gave the target price to RMB185.3, respectively 93/71/53x P/E for 2019/2020/2021. "Buy" rating. (Closing price as at 24 Feb)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()