-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Great Eagle Holdings Ltd (41.HK) - Geographically Diversified Property Investor

Thursday, December 29, 2016  24751

24751

Great Eagle Holdings Ltd(41)

| Recommendation | Accumulate |

| Price on Recommendation Date | $33.650 |

| Target Price | $38.600 |

Weekly Special - 2333 Great Wall Motor

Geographically Diversified Property Investor

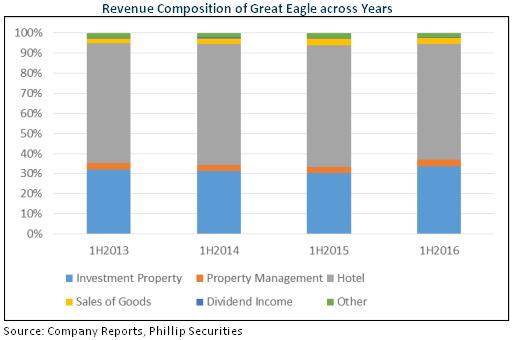

Great Eagle is a diversified property investor, with its major revenue coming from its hotel operating business, which operates hotels in major cities around the world. Apart from the hotels directly operated by Great Eagle, Great Eagle's main assets include Champion REIT (2778.HK) and Langham Hospitality Investment (1270.HK), each of whom hold valuable assets of different types in prime locations such as Central and Mong Kok. The assets held by Champion REIT and Langham Hospitality Investment are vastly different, with Champion REIT holding mainly commercial and retail properties in Central and Mong Kok and Langham Hospitality Investment holding the hotels in Tsim Sha Tsui, and Mong Kok. According to the below chart, the revenue composition has been fairly constant across the years, with investment property and hotel segments contribute to the majority of the revenue. In particular, the hotel segment alone contributes to 58% of the revenue.

Hotel Portfolio Spans across the Globe

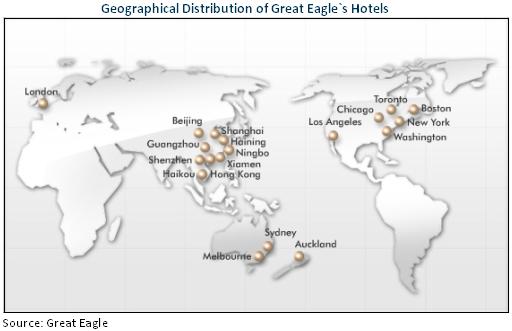

Great Eagle has established strategic presence for its hotel business in major cities around the world. Langham Hotels can be found in almost every continents and in top cities such as London, Toronto, Boston, New York, Washington and Chicago and these hotels are directly owned by Great Eagle instead of owned indirectly via Langham Hospitality Investment. Besides, the company plans to expand its presence by setting up hotels in Tokyo and San Francisco.

Great Eagle's hotels are well-positioned in the prime location and the heart of the cities. In particular, the London hotel is located at Regent Street, which is the primary shopping area while the New York hotel is located at Fifth Avenue and is just a few minutes` walk away from the Empire State Building. With such a prime location, Great Eagle's hotels regularly achieve high occupancy rate and are able to charge high room rate in recent years and in 1H2016, the Lodnon hotel's occupancy rate reached the 81.8%, the highest in 4 years and the room rate was 274 pound per night, one of the top tier rates in London.

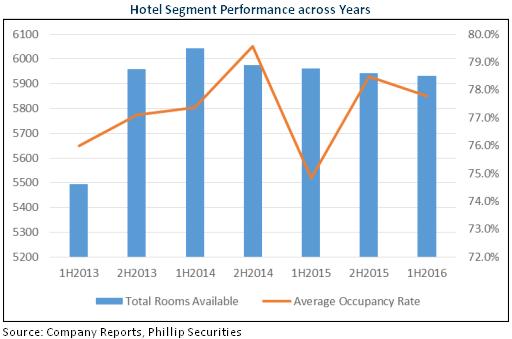

The number of hotel rooms available has increased significantly in 2013 and has stayed fairly stable afterwards. The general occupancy rate of the hotels has also shown improvement in 1H2016 in comparison with 1H2015.

Apart from the current hotels, Great Eagle has been actively expanding its hotel portfolio. In June 2016, Great Eagle has completed the acquisition of a land for hotel development in Tokyo. The hotel is expected to commence construction in 2017 and the expected GFA is 36,000 square metres. Besides, Great Eagle has projects in USA and Shanghai. The projects will provide more than 1000 hotel rooms in total and about 815 hotel rooms will be gradually available in 2017 and 2018.

Hong Kong Tourism Outlook

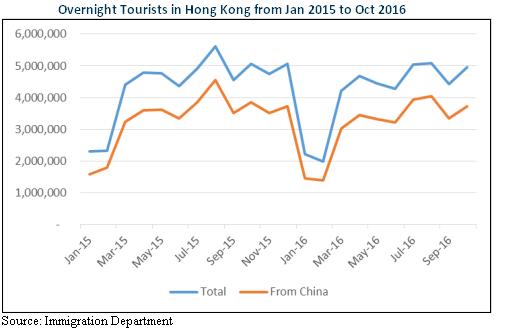

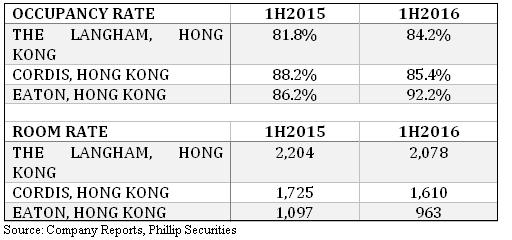

The hotels in Hong Kong of Great Eagle alone contributed to 8% of the total revenue of the group. The revenue for Langham Hospitality Investment, the operator of the Hong Kong hotels of Great Eagle, however has a YoY drop of 0.3% in 1H2016. The drop in revenue is caused by the drop in total overnight tourist visiting Hong Kong in 1H2016 from 22,926,968 to 21,843,257, a drop of 4.7% which is in turn caused by the drop in overnight tourists from China, which in the same period has dropped from 17,172,526 to 15,839,514. The decline in number of tourist has narrowed between July and October and the total number of tourist has dropped from 20,170,577 to 19,511,664, a 3.7% decline, which is a lower percentage decline than the one in 1H2016.

The occupancy rate of the hotels in Hong Kong has increased in general despite the reduction in the total number of visitors. However, the room rate has dropped, with Eaton having the greatest drop of up to 12%.

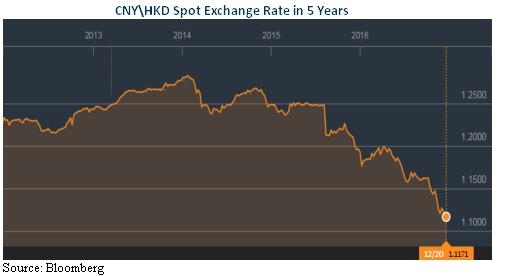

The reduction in total number of overnight tourists visiting Hong Kong is solely contributed by the reduction in Chinese overnight visitors. In fact, the number of non-Chinese overnight visitors have increased in general throughout 2016. The reason for the reduction in Chinese tourists is partly contributed by the depreciation of Renminbi. According to the diagram below, ever since CNY\HKD reached its peak of around HKD1.2834 per unit of CNY, CNY has depreciated about 13% to the level of 1.1171 today. Because of the reduction in purchase power, the number of Chinese tourists coming to Hong Kong has reduced.

With the expectation that USA continuing its rate hike in the coming years, we expect Renmibi to depreciate further. The tourism of Hong Kong, which is mainly driven by the northern incoming people, is expected to suffer from the depreciation and the possibly a drop in incoming Chinese tourists. Hence the occupancy rate and room rate charged by the hotels will continue to face pressure.

Great Eagle's Profitability

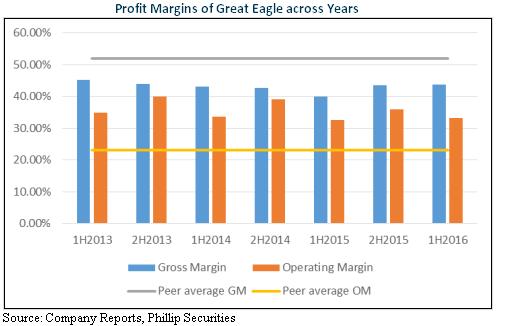

Great Eagle's gross profit margin has ended its 3-year consecutive drop and has rebounded to 43.66%, the highest in 2 years.

Great Eagle's gross profit margin is lower than that of its peers engaging in the hotel sectors. By examining the gross profit margin of Langham Hospitality Investment (1270.HK), which solely composes of hotel asset, the gross margin is much higher than the current 43%. Since Great Eagle's business consists of investment property and sale of goods, the gross margin is therefore dragged down due to the lower margin in other business. After accounting for all other expenses, Great Eagle in fact has higher operating margin than its peers.

Valuation

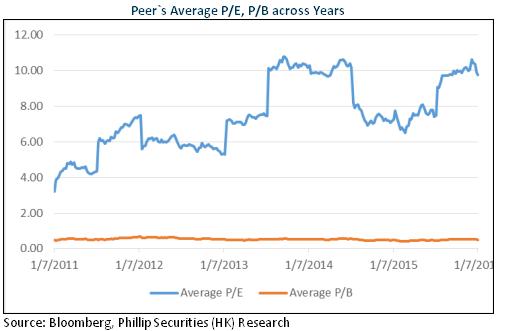

The peer average P/E and P/B are 7.50x, and 0.53x respectively. Great Eagle's target price is therefore $38.60, with Accumulate rating assigned. (Closing price as at 27 Dec 2016)

Risk

Rapid depreciation in Renminbi

Delay in opening of new hotels

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()