-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

COLI (688.HK) - Reaching the standard in advance shows the strong competition advantage

Wednesday, November 13, 2013  2643

2643

COLI(688)

| Recommendation | Accumulate |

| Price on Recommendation Date | $23.100 |

| Target Price | $24.600 |

Weekly Special - 2333 Great Wall Motor

Investment summary

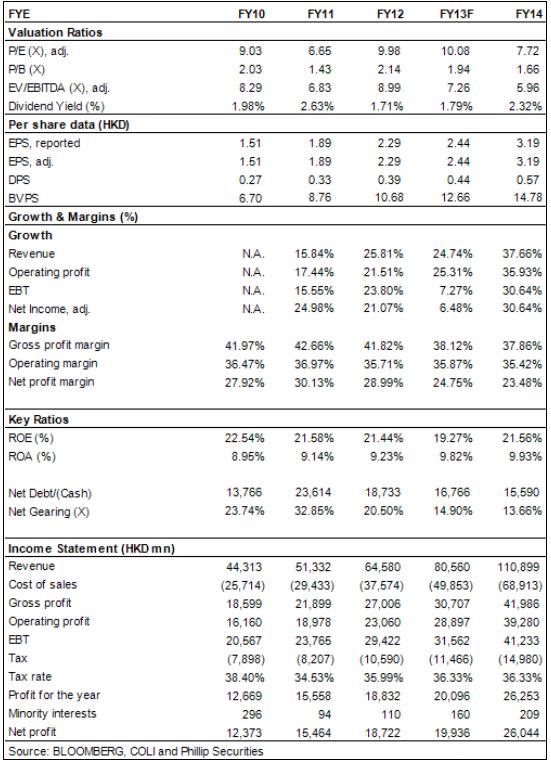

In the first ten months of 2013, China Overseas Land & Investment Co., Ltd (hereinafter referred to as COLI) has realized the contract sales volume of 121.6 billion Hong Kong Dollars(hereinafter ”HKD”), which has reached this year's annual sales target of 120 billion HKD Dollars in advance after the implementation of up-regulation. Besides, the contract sale area adds up to 8.08 million square meters, with the average sales price reaching 15050 HKD/ square meter.

Measured over the course of 2013, the rich and steady houses available to be launched on the market and the consumers` strong need all guarantee the strong and steady increase of COLI's sale. Among the first ten months, there were 8 months` sale over 10 billion, and the average monthly sale was 12.1 billion. If everything goes well, the whole year's sale of COLI will be over 140 billion HKD, and the growth of sale will be over 26%, which approximates the growth in 2012.

As to the sale prospective in 2014, we think that the strong increase of newly-built area in this year will guarantee the rich available resources of next year. Although the uncertainty on the consumers` needs is relatively high, the double-digit increase is still predictable, and the structural changes of area are being more and more obvious.

In the first half year of 2013, the profit increase of mainland real estate business developed by COLI drove the whole performance to be perfect. The sales in the first half year increased by 27% to 32.2 billion HKD on year-on-year basis, of which the mainland real estate sale covered a proportion of 92%, and the sale in Hong Kong and Macao covered a proportion of 5%. Business profit increases by 7.8% to 13.2 billion HKD on a year-on-year basis, and the real estate business profit of mainland is 10.1 billion HKD, covering a proportion of 76.5% of the whole business profit, while the business profit of Hong Kong and Macao area is 0.22 billion HKD, covering a proportion of 1.7%. The whole gross profit rate reaches 36.3%, which is relatively good in the industry. Profits attributable to shareholders increase by 31.6% to 11 billion HKD which equals to 8.82 billion yuan on year-on-year basis; and the core profits increase by 26.7% to 8.06 billion Hong Kong Dollars equaling to 6.45 billion yuan on year-on-year basis.

In the first ten months of 2013, the newly increased land reserve in COLI added up to 9.56 million square meters, of which 9.226 million square meters were newly-increased equity land reserve. Since the second-half year, COLI had 4.94 million square meters of newly-increased land reserve, which is more than first-year's 4.62 million square meters. It shows the enhancement of the management's optimistic perspective.

Benefiting from the prospective-meeting of strong sale increase and carry-over revenue, COLI's balance sheet gets to be optimized. At the end of June, the cash on the account of the group has increased from last year's 41 billion to 51.8 billion, and the comprehensive net lending rate has decreased from 20.5% at the end of last year to 14.9%. In the first half year, the average borrowing costs of the company was kept at 3.8%, which was at the lowest level in the real estate industry. In addition, because of the influence of increased borrowing amount, the overall financial expenses increased by 26% and reached 1.11 billion HKD compared with that of 2012 in the same period.

In this high-prosperity round, COLI maintained the strong expansion ability, and the performance grew rapidly with the core market share continuing to rise. It maintained a strong competitive power, and was the leader among the stocks of real estate in Hong Kong. We kept the net asset value per share of COLI at 29 HKD and the target price in 12 months is 24.6 HKD which is a 15 % discount compared with the NAV, and is equivalent to 7.7 times of the expected PE ratio in 2014. We maintained the "Accumulate" rating of the COLI.

With a strong performance the sales achieved, reaching the standard ahead of two months.

On November 8, the COLI announced that, the company achieved the real estate contract sales volume of 9.85 billion HKD in October, with the contract sales area of 720,000 square meters. In terms of the area of the sales projects, in October, the Yangtze river delta region was the area with the largest contract sales volume and contract sales area of China Overseas, with the sales contract volume achieving 4.905 billion HKD and the contract sales area being 315,900 square meters.

Therefore, in the first ten months of 2013, the contract sale of COLI added up to 121.6 HKD, which has reached this year's annual sales target of 120 billion HKD Dollars in advance after the implementation of up-regulation. Besides, the contract sale area adds up to 8.08 million square meters, with the average sales price reaching 15050 HKD/ square meter.

The sales volume of the COLI included the sales performance of China Overseas Grand Ocean (81. HK),which was targeting at the third or fourth tier cities. Among them, China Overseas Grand Ocean's contract sales volume was 14.6 billion HKD, with the contract sales area of 1.39 million square meters, and the average sales price of 10,500 HKD per square meter. Apart from the sales performance of this part, the average sales price of COLI was about 16,000 HKD per square meter, which was 52% higher than that of China Overseas Grand Ocean and reflected the different market positioning.

Measured over the course of 2013, the rich and steady houses available to be launched on the market, and the consumers` strong need all guarantee the strong and steady increase of COLI's sale. Among the first ten months, there were 8 months` sale over 10 billion, and the average monthly sale was 12.1 billion. If everything goes well, the whole year's sale of COLI will be over 140 billion HKD, and the growth of sale will be over 26%, which approximates the growth in 2012.

As to the sale prospective in 2014, we think that the strong increase of newly-built area in this year will guarantee the rich available resources of next year. Although the uncertainty on the consumers` needs is relatively high, the double-digit increase is still predictable, and the structural changes of area are being more and more obvious.

The performance of the first-half was ideal

In the first half year of 2013, the profit increase of mainland real estate business developed by COLI drove the whole performance to be perfect. The sales in the first half year increased by 27% to 32.2 billion HKD on year-on-year basis, of which the mainland real estate sale covered a proportion of 92%, and the sale in Hong Kong and Macao covered a proportion of 5%. Business profit increases by 7.8% to 13.2 billion HKD on a year-on-year basis, and the real estate business profit of mainland is 10.1 billion HKD, covering a proportion of 76.5% of the whole business profit, while the business profit of Hong Kong and Macao area is 0.22 billion HKD, covering a proportion of 1.7%. The whole gross profit rate reaches 36.3%, which is relatively good in the industry. Profits attributable to shareholders increase by 31.6% to 11 billion HKD which equals to 8.82 billion yuan on year-on-year basis; and the core profits increase by 26.7% to 8.06 billion Hong Kong Dollars equaling to 6.45 billion yuan on year-on-year basis.

Continuously supplementing the land reservation

In the first ten months of 2013, the newly increased land reserve in COLI added up to 9.56 million square meters, of which 9.226 million square meters were newly-increased equity land reserve. Since the second-half year, COLI had 4.94 million square meters of newly-increased land reserve, which is more than first-year's 4.62 million square meters. It shows the enhancement of the management's optimistic perspective.

With regard to the strategy of land acquisition, CAVOF tended to prefer the east region of China with better sales performance. Since the second half year, CAVOF has won 7 cases of land acquisition in the eastern China with the total equity development area of 769,500 square meters which costs 8.5 billion yuan.

In view of the rise of land reserve in the second half and the increase of new construction area, the available resource of the company in the next year is going to rise with a strong certainty. It's quite important to keep low inventory and to raise the sales rate in 2014 for COLI to keep active in the strategy.

Continuously optimizing the financial structure

Benefiting from the prospective-meeting of strong sale increase and carry-over revenue, COLI's balance sheet gets to be optimized. At the end of June, the cash on the account of the group has increased from last year's 41 billion to 51.8 billion, and the comprehensive net lending rate has decreased from 20.5% at the end of last year to 14.9%. In the first half year, the average borrowing costs of the company was kept at 3.8%, which was at the lowest level in the real estate industry. In addition, because of the influence of increased borrowing amount, the overall financial expenses increased by 26% and reached 1.11 billion HKD compared with that of 2012 in the same period.

Risks

Regulation of the policy risks;

Demand side is weak;

The development process is slow.

Estimation

In this high-prosperity round, COLI maintained the strong expansion ability, and the performance grew rapidly with the core market share continuing to rise. It maintained a strong competitive power, and was the leader among the stocks of real estate in Hong Kong. We kept the net asset value per share of COLI at 29 HKD and the target price in 12 months is 24.6 HKD which is a 15 % discount compared with the NAV, and is equivalent to 7.7 times of the expected PE ratio in 2014. We maintained the "Accumulate" rating of the COLI.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()