-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Yonyou (600588.SH) - Robust growth of Cloud services in hope of domestic replacement

Tuesday, July 23, 2019  10475

10475

Yonyou(600588)

| Recommendation | Accumulate |

| Price on Recommendation Date | $26.870 |

| Target Price | $29.580 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

Yongyou is a leading provider of enterprise services in China, offering cloud, software and financial services. The result in first quarter was doing well, where the revenue grew by 16.6%, and the cost control improved. Besides, the growth of revenue from cloud services remained robust, up by 95% YoY, and paid enterprise customers increased by 46.3% YoY. We give a TP of RMB $29.58, 6.4% lower than previous, downgrading to “Accumulate” recommendation, with 10.1% potential upside. (Closing price at 18 Jul 2019)

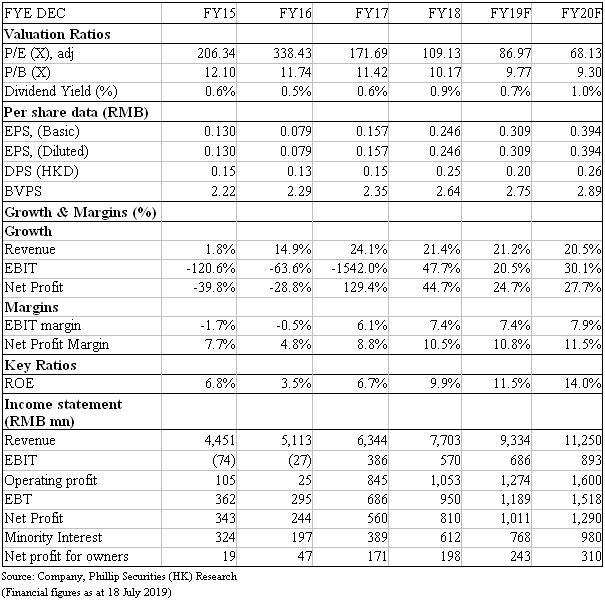

Result update

The group announced its first quarter results for 2019. During the period, the revenue was RMB 125 million , up 16.6% YoY; the operating loss was RMB 155 million, an increase of about RMB 40 million over last year. In addition, gross profit margin decreased by 1.6% to 62.5%, but the cost control improved. Selling and administrative expenses to revenue decreased by 3.5% and 4.7% respectively. Net profit was RMB 102 million, which turned into a profit from last year, mainly due to the sale of SuiRui Technology this year. The net loss attributable to owners after deducting non-recurring gains was RMB 54.77 million, a decrease of 51.2% YoY.

Revenue from Cloud services reached RMB 125 million, a YoY increase of 95%. Currently, there are about 4.77 million cloud service enterprise users and about 380,000 paid enterprise customers, increased by 46.3% YoY.

In other business areas, revenue from software business was RMB 864 million, up 20.6% YoY; payment service revenue was RMB 74 million, up 230.1% YoY; however, revenue from Internet investment and financing information service business decreased 29.7% YoY to RMB 197 million.

Launch and strength the cloud products, build up a cloud ecosystem

The Group launched NC Cloud 1903, which adopted the latest hybrid cloud technology architecture to provide hybrid cloud solutions for large enterprises. It is believed that the new products will help the group enter the cloud market of large enterprises. Besides, the Group has also strengthened the marketing of NC Cloud, which is expected to make NC Cloud sales scalable. For U8 Cloud which is targeting the medium-sized companies, the Group will accelerate its research and development and strengthen its promotion in the industry.

The Group continued to build up a cloud ecosystem and launched 52 models in the cloud market, including cloud-based eco-products such as IoT services, business travel services, and cloud customer service small business editions. The total number of eco-partners in cloud market exceeded 3,500, and the total number of products and services exceeded 5,500.

We expect the Group to increase its investment in research and development in the cloud business, which may reduce the net profit margin in the short term, but it is expected to create a long-term competitive advantage.

Visiting from Huawei may implies the acceleration of domestic replacement

Media reported that the Huawei ERP team visited Yonyou Industrial Park in Beijing. Therefore, it is speculated that Huawei may abandon SAP, their current ERP system, and adopt a domestic one. We think it is likely to happen. Under the China-United trade war, Huawei became one of the targets United States wants to restrain. US prohibited companies in US from providing any services to Huawei. In order to reduce the dependence on foreign software, we believe that Huawei has sufficient incentives to shift their current foreign ERP system into domestic. Although there is no confirmation at present, this visit reflects the intention of Huawei.

Valuation

Based on the net profit attributable to the owner in 2020, we derive a TP of RMB $29.58, 6.4% higher than the previous TP, reflecting a 20x P/E in light of the rapid growth in cloud services. Although increase in research and development on cloud services may reduce the net profit margin in the short term, but it is expected to create a long-term competitive advantage. Since the sharp rise in share prices recently, we have downgraded to the “Accumulate” rating, with a potential upside of 10.1%.

Risk

1. Slower-than-expected growth in cloud products

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()