-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Koradior (3709.HK) - Multi-brand Strategy with Effective Marketing and Promotion

Tuesday, February 14, 2017  24505

24505

Koradior(3709)

| Recommendation | Buy |

| Price on Recommendation Date | $9.010 |

| Target Price | $11.680 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

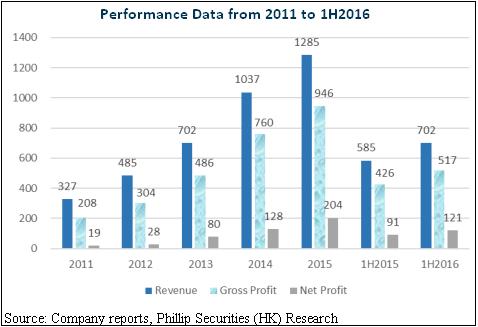

- Good historical performance. Revenue and net profit increased at CAGR of 40.8% and 80.0% respectively from 2011 to 2015. Total revenue increased by 20.03% and the net profit increased by 32.29% YoY in 1H2016.

- The company carries out multi-brand strategy. It`s building multi-brand platform through self-brand building, acquisitions and the agent business of foreign brands.

- The company has nationwide sales network and the shop expansion process is relatively fast.

- Ways of marketing and promotion implemented by the company are effective.

Company Overview

Koradior engages in the design, promotion, marketing and sales of their self-owned branded products, Koradior, La Koradior and Koradior elsewhere that target affluent ladies between the ages of 30 and 45. In 2015, Koradior was awarded “Forbes China Potential Enterprises Award” by Forbes China. Koradior was also awarded “The Most Influential Brand” by Shenzhen Garment Industry Association in 2015.

Total revenue increased to RMB701.59 million in 1H2016, representing a 20.03% YoY increase; the net profit for 1H2016 was RMB120.54 million, representing a 32.29% YoY increase.

The revenue came from self-operated retail stores, distributors, e-commerce platform and so on. The revenue from self-operated retail stores has the highest proportion. The revenue from self-operated retail stores accounted for 84.4% of total revenue in 1H2016 and it accounted for 85.0% of total revenue in 2015.

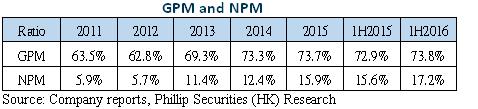

Following charts show the performance data from 2011 to 1H2016(RMB mn). Revenue and net profit increased at CAGR of 40.8% and 80.0% respectively from 2011 to 2015.

Sales Network

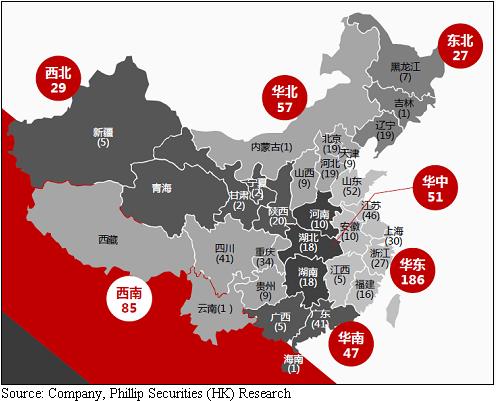

The company`s products are sold across nationwide sales network, most of the network consists of self-operated retail stores, covering over 100 cities in 29 provinces, autonomous regions and municipalities in China. As at 30 June 2016, there were 482 retail stores in total: 433 are self-operated stores and 49 are operated by distributors. In 1H2016, the company opened 45 new stores and closed 21 stores, with a net increase of 24 stores. The picture below shows Koradior`s domestic sales network:

Multi-brand Strategy

The company carries out multi-brand strategy. The company is building multi-brand platform through self-brand building, acquisitions and the agent business of foreign brands.

The table below shows the introduction to the company`s self-owned brands Koradior, La Koradior and Koradior elsewhere.

In June 2016, the company acquired 65% equity interests in Shenzhen Mondial Industrial Co., Ltd. which is a high-end ladies` apparel corporation in Shenzhen. The “CADIDL” brand under the company has a history of nearly 20 years and targets business ladies between the ages of 30 and 40 who have higher artistic taste and quality requirement for their apparel in Tier I and Tier II cities in China.

Fosun International bought into Koradior at the end of 2015. Introduced by Fosun, Koradior has established strategic cooperation relationship with Qingdao Kutesmart and has adopted O2O and direct sales model to officially launch the new brand “DE KORA” for tailor-made fashion. DE KORA targets young consumers aged 25-35 graduated within 10 years to create a global platform for personal customization. They will build airport flagship store to enhance customers` brand awareness and brand recognition.

In addition, the company is setting up a brand management company with well-known retail experts to explore Chinese market for foreign brands via agent business.

According to the company, the market size of middle and high-end ladies-wear industry is nearly 140 billion and the market concentration is relatively low at present. The middle and high-end ladies-wear industry is in large-scale development stage now and the industry consolidation process is accelerating. There are a lot of M&A opportunities when the companies are establishing the advantage of scale. M&A is one of the long-term development strategy of the company, and they will continue to proceed.

Effective Ways of Marketing and Promotion

The Group has placed advertisements at Shenzhen Airport, Shanghai Pudong International Airport, Shanghai HongQiao International Airport and Chengdu Airport. Let`s take a look at the passenger flow of the four airports. According to Wind, the passenger flow of Shenzhen Airport is 41.97 million in 2016, with a 5.7% YoY increase. Shanghai Pudong International Airport, Shanghai Hongqiao International Airport and Chengdu Airport recorded passenger flow of 60.10 million, 39.09 million and 42.24 million respectively in 2015; and the numbers as at end of October 2016 were 55.49 million, 33.59 million and 38.48 million YTD.

In addition, as the sole fashion brand from China officially invited by the Milan Fashion Week in Italy, La Koradior made its debut in September 2015. The company also invited Miranda Kerr, a top model worldwide, and signed with her to be the company`s brand spokesperson. In March 2016, their self-owned brand “Koradior elsewhere” attended the A/W 2016 Shenzhen Fashion Week. The Group also placed brand imaging advertisements in selected top nationwide circulated fashion/lifestyle magazines and publications, such as “VOGUE” etc. The Group also co-sponsored the film “Only You” directed by Zhang Hao and starring Tang Wei and Liao Fan. And the Group also became the sole apparel brand placed in Les interprètes, a TV drama starring by Yang Mi with high audience rating.

Financial Analysis

Compared with FY2015, the trade receivable turnover days, trade payable turnover days and inventory turnover days all decreased in 1H2016. Trade and bills receivables turnover days was 43 in 1H2016, compared with 47 in 2015. Trade and bills payables turnover days was 56 compared with 69 in 2015. Inventory turnover days was 246 compared with 249 in 2015.

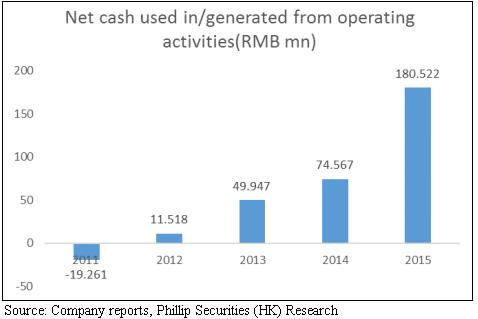

As at end of June 2016, the equity debt ratio was 17.75% compared with 9.82% at the end of Dec 2015. The chart below shows the net cash generated from operating activities in recent years:

Cash and cash equivalents on 30 June 2016 was 598 million RMB (end of 2015: 437 million RMB). The cash flow of the company is healthy and the company has sufficient cash on hand, which is good for future expansion strategy.

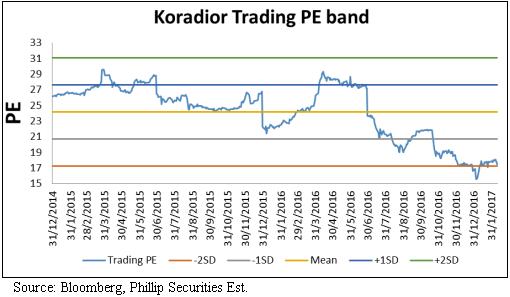

Valuation

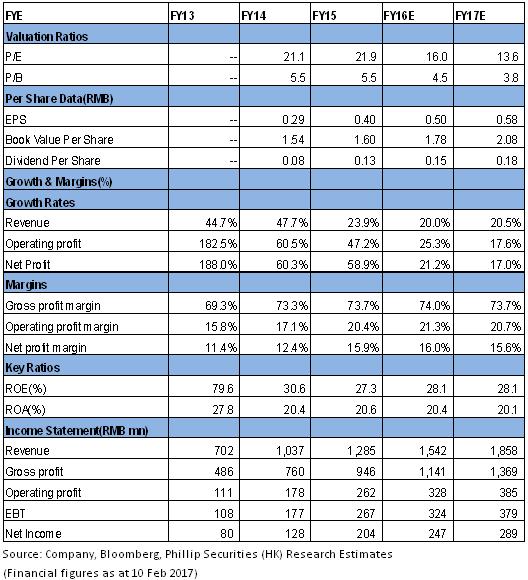

Buy Rating is given with TP of HK$11.68. We expect net profit growth of 21.2/17.0%, driven by 20.0%/20.5% revenue growth. The stock price experienced correction recently and we think the price is undervalued. Our TP of HK$11.68 represents 20.7/17.7x FY16E/FY17E P/E. (Closing price as at 10 February)

Risk

The ladies-wear industry in China faces intense competition from both international and domestic brands;

Changes in fashion trends and consumer tastes.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()