-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Daqin Railway (601006.CH) - Artery of coal transport; bridgehead of railway revolution

Monday, December 8, 2014  16543

16543

Daqin Railway

| Recommendation | BUY |

| Price on Recommendation Date | $9.480 |

| Target Price | $11.300 |

Weekly Special - 002050 Sanhua

-As far as the traffic volume is concerned, DaQin is China's biggest coal railway transport company, bearing the national strategic mission of "Coal transmission from West to East ". The company's cargo volume takes up about one-sixth of that of the national railway, and coal volume accounts for about one-third of that of the national railway. Daqin's primary clients include all big coal enterprises in the central and western region, the four major power distribution network groups of China, the five great power generation groups, the ten big steel groups and a large amount of industrial and mining enterprises. The company possesses the world-class heavy-haul equipments and technology systems, Datong-Qinhuangdao line under whose enjoys the good reputation of "China's first route of heavy-haul transport".

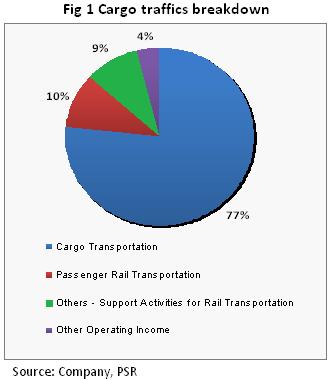

-The revenue of Daqin mostly comes from freight, passenger transport and others. Among them, freight takes up approximately 80% of the total revenue, and passenger and others respectively accounts for 10%. As the shortest railway connecting Datong and Qinhuangdao, superadded relatively high transport efficiency and implementation of special transport price, the multiple operational metrics and profitability of DaQin Railway are all ahead of the others in the same industry.

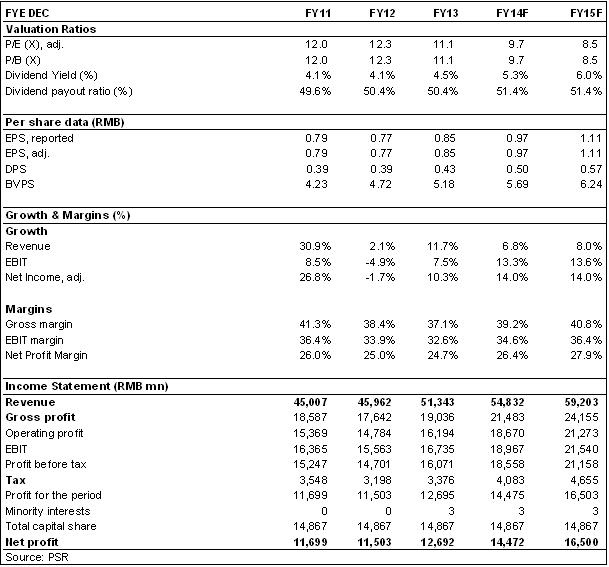

-DaQin altogether achieved 14.2 billion Yuan in the third quarter, up 6.2% yoy, and net profit affiliated to the parent company made of 3.98 billion Yuan, up 26.4% yoy, corresponding EPS being 0.27 Yuan. Gross margin sharply increased by 4.37 ppts yoy and by 1.8 ppts qoq to 40.3%.

How we view this

The growth of company’s operating revenue mainly came from the increase of freight rates, while savings of a series of costs and outlays made the growth of profit exceed that of revenue. We believe that company's holding abundant cash will provide a guarantee for maintaining stable high dividend rates in the next few years.

We think the adjustment of China energy structure will be a long and lengthy process in which coal would still play an important role. On the other hand, China's large-scale railway construction makes the China Railway Administration will always have a funding gap and financing demand in the future. Under the background of the continuous promotion of freight price rise and railway reform, as a high-quality asset of China railway, the company has sufficient future development impetus. For passenger transport, the high-speed railway network extension and the coming launch of Beijing-Tianjin-Hebei integration planning will make Daqin's passenger business also face new development opportunities..

Investment Action

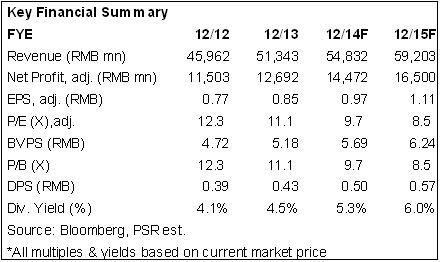

In the valuation, our target price is RMB 11.3 Yuan, equivalent to 11.6/10.2xP/E of 2014/2015F EPS. Considering the extremely appealing dividend payout rate, buy rating is given for the first time.

Company Profile

Controlled by Taiyuan Railway Administration, Daqin Railway(Daqin)is a regional, diversified railway transport enterprise and bases its business on the transportation of coal, coke, iron and steel, ores and passenger. The Company was founded in 2004, and in the earlier stage, it was mainly engaged in Datong-Qinhuangdao line with an overall length of 658 Km. It purchased assets such as Feng-sha-da, Bei-tong-pu Railway and so forth in 2005, and was listed on IPO of domestic A-shares in the stock market in July, 2006, releasing 3,030 million shares and raising RMB 15,000 million. In 2010, the Company publicly additionally released 1,890 million A-shares and raised RMB 16,500 million to purchase the assets belonged to its big shareholder Taiyuan Railway Administration.

At present, the Company operates 9 trunk lines, namely Datong-Qinhuangdao, Bei-tong-pu, Nan-tong-pu, Hou-yue, Shi-tai, Feng-sha-da, Tai-jiao, Jiang-yuan and Hou-xi, and 9 branch lines like Kouquan. The transportation network passes through Sanjin from the north to the south and stretching across Shanxi Province, Hebei Province, Beijing City and Tianjin City, with an operating mileage of 2,725 Km.

A Great Artery of Coal Transport

It is engaged in the passenger and cargo transport of Shanxi Province and part of the cargo freight of Hebei, Beijing, Tianjin, Inner Mongolia and Shaanxi, which is the largest coal transport enterprise, overload coal transportation and a critical channel of “transporting coal from the west to the east” strategy. Cargo freight volume covers one sixth of the freight and one third of the coal transported via railway across China. Its customers are mainly coal companies in central and western China, the major four power grids, five power generation groups, ten iron and steel companies and tens of thousands of industrial and mining enterprises.

"Transporting coal from the west to the east " is mainly carried out via the three large railway transport of the North, the Middle and the South, of which, the North part mainly consists of Railways such as Datong-Qinhuangdao, Shen-Huang, Feng-Sha-Da, taking up 55 percent of the whole capacity of "coal transported from the west to the east" of China. Among them, Datong-Qinhuangdao and Feng-Sha-Da take up 43.8 percent of the whole capacity of "coal transported from the west to the east", and Datong-Qinhuangdao line takes up 16 percent of the state's total coal railway capacity. The Company's coal turnover reached 590 million tons in 2013. Its cargo shipment reached 284 million tons from January to June in 2014.

In the aspect of passenger transport business, the Company operates 62.5 pairs of passenger trains which are trains run from Taiyuan to 17 cities such as Beijing, Tianjin, Shanghai, Guangzhou, etc. and trains run from Datong to 8 cities such as Beijing, Tianjin, Hangzhou, Xi`an, Shenzhen, etc., with 2,187 passenger transport kilometers, including 15 lines, and 92 railway stations for selling ticket. Other business mainly includes providing locomotive traction, passenger traffic line and maintenance service for other railway transportation enterprises.

The Company has a world-class haulage equipment and technology system, and Datong-Qinhuangdao Railway is titled of " the first heavy haulage railway in China ", which is equipped with a series of modern leading railway equipment system such as electric locomotives with HXD-type high-power meters, CRH5-type bullet trains, C80-type dedicated trains for coal transport and so forth.

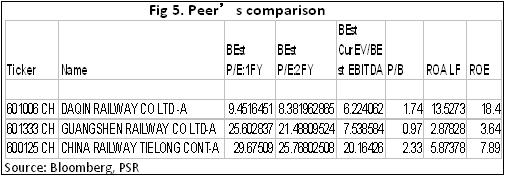

Operation analysis: taking a leading position over the peers

The Company’s revenue mainly comes from freight transport, passenger transport and other revenues, among which freight transport takes about 80% of the total income, passenger transport and other business respectively take about 10%. Main business cost of the Company includes such six aspects as employee compensation, depreciation, electricity and fuel, charges of freight car use, service charges of freight and passenger transportation, and materials, which accounts for more than 80% of the total cost.

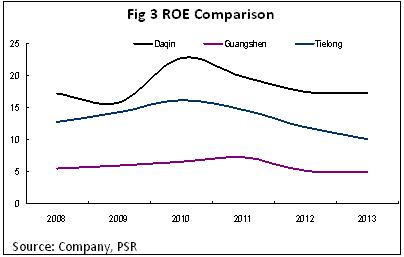

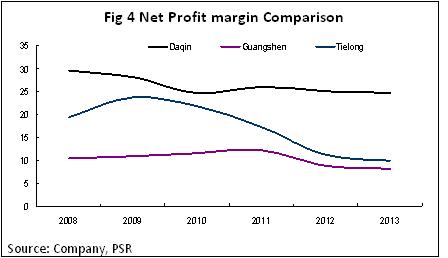

As the shortest railway connecting Datong and Qinhuangdao, with higher transportation efficiency and special freight rate, DaQin takes a leading position over the peers in several operating indicators and profitability. As shown in the figure below, ROE and net profit margin of DaQin are all much higher than its peers. Besides, the free cash flow margin and dividend payout ratio (50%) of DaQin are also significantly higher than its peers.

2014Q3 saw increased gross margin

The third quarter result of 2014 released by DaQin showed that, it totally achieved revenue of 14.2 billion Yuan in the third quarter, up by 6.2% year on year, and the net profit belonging to the parent company was 3.98 billion Yuan, a great increase of 26.4% year on year, corresponding EPS of 0.27 Yuan. It recorded an accumulative income of 40.58 billion Yuan in the first three quarters, up by 7% year on year, and the net profit belonging to the parent company was 11.16 billon Yuan, up by 16% year on year, and the earnings per share were 0.75 Yuan, a year-on-year increase of 15.4%.

In the third quarter, benefiting from the yoy reduction of costs, the Company's yoy gross margin sharply grew by 4.37 percentage points and the qoq increased by 1.8 percentage points to 40.3%. The growth of revenue primarily came from the increase of freight rate, while the savings of a series of costs and outlays of company made the growth of profits exceed that of incomings. The cash flow generated by operating activities in the first three quarters significantly increased by 26% yoy to 15.3 billion Yuan. We believe that holding abundant cash provides a guarantee for maintaining stable high dividend payout rates in the next few years.

Go ahead on the road of Railway reform; open up a new pattern of development

We believe that the adjustment of domestic energy structure will be a long and lengthy process in which coal would still play an important role. On the other hand, China's massive railway expansion construction makes the railway always have a financial gap and financing demand. Also, a ceiling occurs in the existing financing channels of railway bond and medium term note. Under the background of the continuous promotion of freight price rise and railway operating mechanism reform in the future, as a high-quality asset of China Railway; the Company has sufficient future development room.

For the Company's passenger business, the high-speed railway network extension and the coming launch of Beijing-Tianjin-Hebei integration planning make the Company's passenger service face new development opportunities.

Valuation and Rating

In the valuation, our target price is RMB 11.3 Yuan, equivalent to 11.6/10.2xP/E of 2014/2015F EPS. Considering the extremely appealing dividend payout rate, buy rating is given for the first time.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()