-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Anton Oilfield Service (3337. HK) - Earnings guidance of 2014 lacks highlights

Friday, October 10, 2014  23663

23663

Anton Oilfield Service(3337)

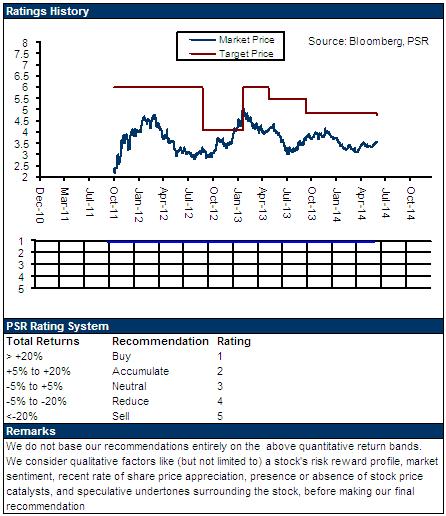

| Recommendation | Neutral |

| Price on Recommendation Date | $2.290 |

| Target Price | $2.200 |

Weekly Special - 002050 Sanhua

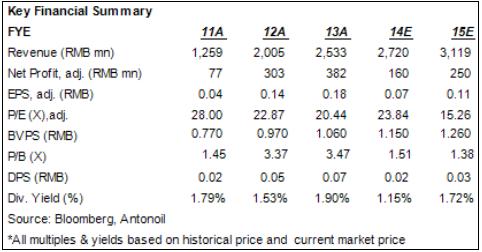

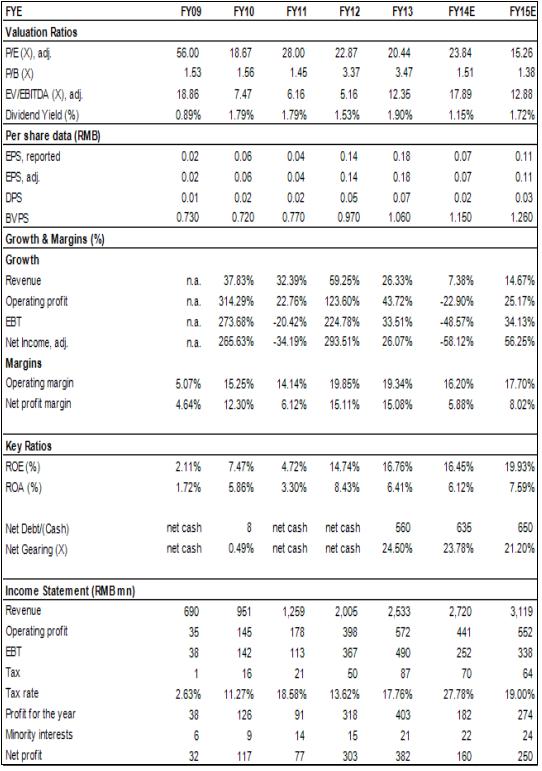

-Recently, Antonoil published the earnings guidance for the year of 2014. Antonoil is expected to see a slight increase of revenue in 2014, but it still bears relatively big cost pressure because of the increase of manpower, depreciation and interest cost due to the human resource, equipment, and funds reserved in advance by the company for the sake of long term development. Besides, calling of accounts receivable will promote significant improvement of the operating cash flow in the second half of the year in comparison with that in the first half of the year.

-The guidance has a positive view of the industry development prospects. Antonoil believes, the domestic demand for natural gas will continue increasing, and the overseas market business will continue keeping high speed growth, so in the long run, the revenue will still hold a high-speed increase. At the same time, the net profit margin will fluctuate in a short term due to changes of the market, but in the long run, along with the increase of capacity utilization rate, the net profit margin is expected to come back to the previous normal level.

-The declining of newly added orders and orders in hand makes the operation of Antonoil face a severe test, and the duration of the negative impact of the anti-corruption campaign on the company is longer than we have expected. We expect that, in the next half year PetroChina will continue to slow down its release of land oil service orders to private oil service companies, and Antonoil needs to increase efforts to obtain oil and gas services orders from other pipelines, but overall sluggish situation of orders in 2014 has already been established.

How we view this

The company's earnings guidance of 2014 also lacks more highlights, and the market reflection is neutral. In addition, the orders of Antonoil in the second quarter are disappointing, furthermore, the negative impact of the anti-corruption campaign on the upstream capital expenditure of PetroChina still continues. In the aspect of industry competition structure, though the announcement of the Big Tiger case has eliminated some uncertainties and made the market activity increased, the oil and gas services companies are still facing the challenges brought about by the new interest structure dividing.

Investment Action

Because of reform of state-owned enterprises, internal cost control, and implementation of marketization of major oil companies, it is difficult for Antonoil to get rid of the difficulty in a short term. We cut its 12m TP to HK$2.2, giving a “Neutral” rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()