-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

United Laboratories (3933.HK) - Rapid Future Growth in Insulin Business

Friday, December 9, 2016  25060

25060

United Laboratories(3933)

| Recommendation | Accumulate |

| Price on Recommendation Date | $4.460 |

| Target Price | $5.140 |

Weekly Special - 2333 Great Wall Motor

Expected Return to Profits in 2H

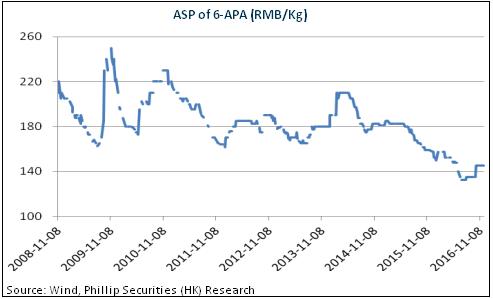

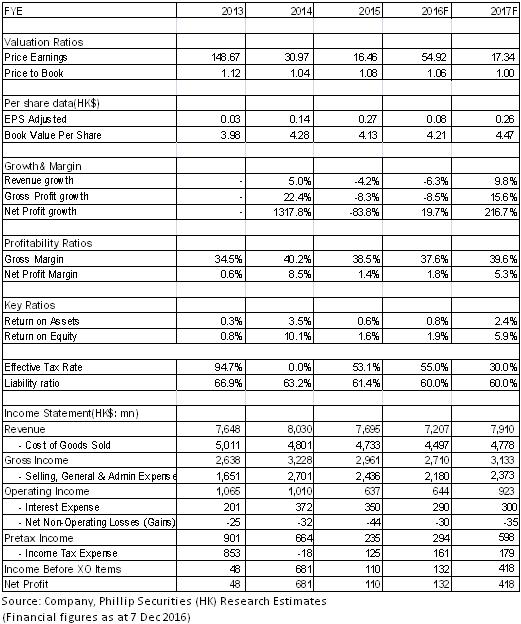

The United Laboratories (TUL) mainly engages in the production and sales of pharmaceutical preparations, raw materials, pharmaceutical intermediates and capsules. In 1H 2016, the company's revenue dropped by 8.6% to HK$3.5 billion, recording a loss of HK$15.1 million, due to the decrease in sales volume and price of the main products. First, the price of the company's main intermediate 6APA and part of the APIs fell. Second, in 1H 2016, TUL's raw material plant in Zhuhai City expanded and upgraded a by-product recovery system starting from March, leading to the decline in amoxicillin production, from 700 ton/month to 200 ton/month. Eventually, the company's sales of 6APA and semi-synthetic penicillin were down by 8.7% and 18.1% Y-o-Y, respectively.

Nevertheless, relevant projects in Q3 have been completed, and some of the previous orders have not been fulfilled. With the gradual release of production capacity, the main product sales will be back on track. At the same time, after more than five years of falling, the recent prices of 6APA, amoxicillin and cephalosporin antibiotics have indicated a slower downtrend, and some varieties even showed signs of recovery. Thus, we expect that the company's intermediates and APIs will gradually return to profits.

Rapid Future Growth in Insulin Business

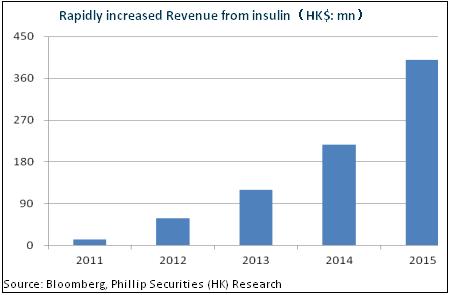

TUL established the production base of insulin APIs and preparations in Zhuhai in 2010, the largest in China so far, and a total of eight new production plants as of June 2016. Currently, the production scale of the insulin API is up to 3 ton/year, including one ton of second generation insulin, one ton of insulin glargine and one ton of insulin aspart, and 300 million preparations can be produced each year. The diabetes segment is expected to be the company's future focus of development and layout. Moreover, the proportion of Chinese patients with diabetes using insulin to control blood glucose is much lower than 30%, the proportion of developed countries. In addition, the foreign-funded companies have dominated the China's market of the second and third generations of insulin. With the consideration of China's medical insurance control, broad prospects lie before import substitutes of insulin.

In addition, TUL is also expected to become the first domestic enterprise providing both second and third generations of insulin. The company has passed One-in-Three Review (production on-site inspection report, production site sampling inspection report and technical review report for comprehensive views), and is expected to be China's second enterprise producing insulin glargine, contributing to the revenue in 2017. Meanwhile, the aspart insulin has completed clinical trials and is submitting for the production approval. The company's growth rate of insulin sales and revenue was up to 57.8% and 84.3%, respectively, in 2015, and we expect that the rapid growth will continue, being the company's main growth driver.

Cost of Capital May Reduce by Issuing Convertible Bonds

The company recently proposed to issue a USD130 million of convertible bonds with an initial conversion price of HK$5.35. The bonds represent 10.38% of the enlarged share capital if fully conversed to the new shares. This move is to provide lower financing costs for the company because the company's short-term debts were due, which have higher financing costs.

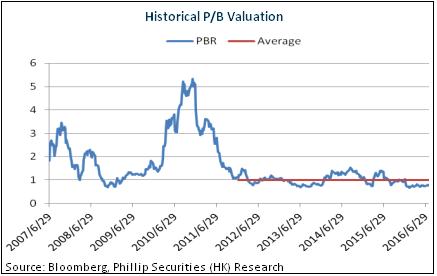

In short, with the stabilization of the antibiotic business and the rapid growth of the insulin business, we expect the company's performance to be significantly improved. We give an estimation of 1.15x BVPS in 2017 and the target price of HK$5.14, with the "Accumulate" rating initially. (Closing price as at 7 Dec 2016)

Risks

Fluctuations in the API prices;

Risks of approval policies.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()