-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Fortune Real Estate Investment Trust (778.HK) - Take away from investor presentation

Tuesday, August 21, 2012  11881

11881

Fortune Real Estate Investment Trust(778)

| Recommendation | BUY |

| Price on Recommendation Date | $5.440 |

| Target Price | $6.530 |

Weekly Special - 2333 Great Wall Motor

Company Overview

Fortune Real Estate Investment Trust (“Fortune REIT”) is a real estate investment trust constituted by a trust deed (the “Trust Deed”) entered into on 4 July 2003 (as amended) made between ARA Asset Management (Fortune) Limited, as the manager of Fortune REIT (the “Manager”), and HSBC Institutional Trust Services (Singapore) Limited, as the trustee of Fortune REIT (the “Trustee”). Listed on 12 August 2003 on the Singapore Exchange Securities Trading Limited (the “SGX-ST”) with a dual primary listing on The Stock Exchange of Hong Kong Limited (the “SEHK”) on 20 April 2010, Fortune REIT was Asia’s first cross-border REIT and also the first REIT to hold assets in Hong Kong. Fortune REIT holds a portfolio of sixteen retail properties in Hong Kong, comprising approximately 2.45 million square feet of retail space and 1,989 car parking lots.

Interim result highlights

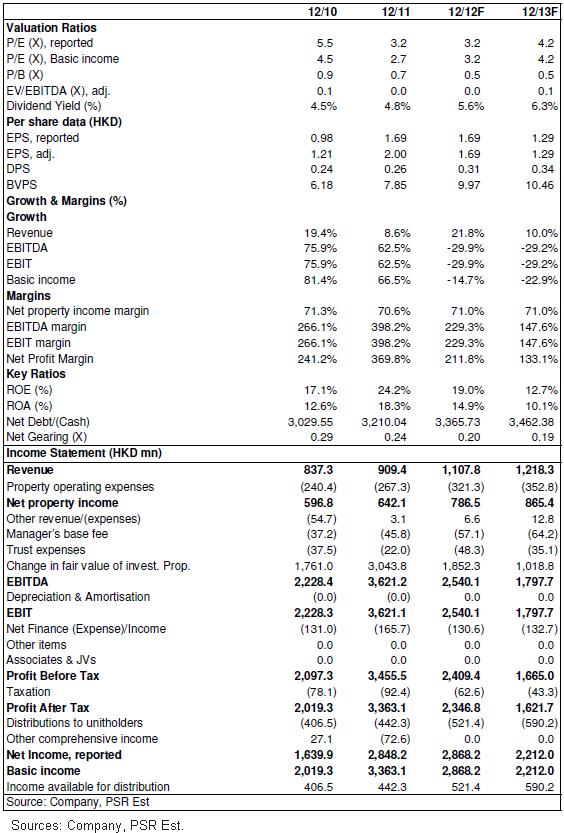

Net property income: HK$ 382.1 mn, up 19.6% y/y

Income available for distribution: HK$268.3 mn, up 24.9% y/y

Distribution per unit: HK$15.82 cents, up 23.6% y/y

Gearing ratio: 24.5% (1H2011: 18.8%)

Summary

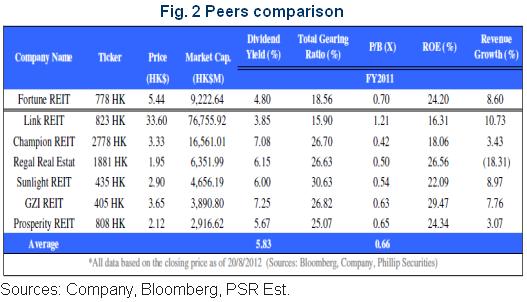

On dividend yield basis, Fortune REIT is currently trading at approximately 24% discount to Link REIT (823 HK). As we forecast that DPS of Fortune REIT will increase at an annual rate of approximately 10% from FY2012 - FY2013, we expect the current yield spread between Fortune REIT and Link REIT to reduce further as Fortune REIT is currently undervalue.

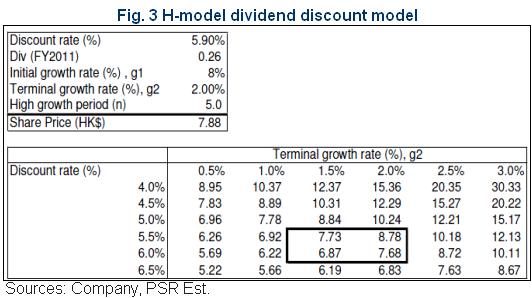

Meanwhile, as at 30 Jun 2012, the dividend yield of HS REIT index was 5.9%. As the HS REIT index hold a diversified portfolio of REITs, it's dividend yield may proxy the required rate of return (discount rate) of Fortune REIT. By using the H-model dividend discount model, the theoretical share price of Fortune REIT is HK$7.88.

We forecast the FY2012 leading dividend yield of Fortune REIT to be 4.7% with DPS of HK$31 cents. The last price of HK$5.44 implies a leading dividend yield of 5.6% and represents a approximately 20% upside potential. We upgrade our 12-month target price of Fortune REIT to HK$6.53 with a “BUY” rating.

Properties portfolio analysis

After the acquisition of two new properties, Fortune REIT holds a portfolio of sixteen retail properties in Hong Kong, comprising approximately 2.45 million square feet of retail space and 1,989 car parking lots. The retail properties are Fortune City One, Ma On Shan Plaza, Metro Town, Fortune Metropolis, Belvedere Square, Waldorf Avenue, Provident Square, Caribbean Square, Jubilee Square, Smartland, Tsing Yi Square, Nob Hill Square, Centre de Laguna, Hampton Loft, Lido Avenue and Rhine Avenue.

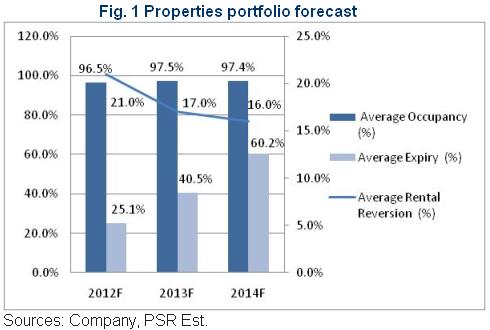

The 1H2012 results is encouraging. Net property income came in HK$ 382.1 mn, up 19.6% y/y. Portfolio occupancy came in 96.5% (FY2011: 97.0%); average rental reversion was 20.6% (FY2011: 15.2%), among the highest level in years; average passing rent was HK$31.0 psf. (FY2011: HK$32.2 psf.). In our forecast, we remain optimistic to the short-term prospect of the properties portfolio. It is mainly due to the strong resilience of retail properties in Hong Kong real estate.

Organic growth driver – AEIs

AEIs has always been the major organic growth engine for Fortune REIT. AEIs at Fortune City One is the largest scale in portfolio. Total CAPEX amounted HK$100 mn. It was commenced at 3Q2011 and expected to be completed by 4Q 2012. As of 30 Jun 2012, over 70% of the project has already completed. Another AEIs at Jubilee Square was commenced at 2Q 2012 and expected to be completed by 1H 2013. Total CAPEX came in HK$15 mn.

Most gross revenue of Fortune REIT stemmed from Fortune City One, accounting of 28.4% of total gross revenue in FY2011. We believe the AEIs at Fortune City One will have a material impact for the revenue growth of Fortune REIT. We forecast the rental expiry and the rental reversion of Fortune City One to be 20.2% (1H2012), 48.0% (FY2013) and 31.8% (FY2014) and 35.9% (1H2012), 29.1% (FY2013) and 27.4% (FY2014) respectively. Although the AEIs at Jubilee Square is much smaller in scale, we expected an improvement in occupancy and a higher ROI from the AEIs. Although management stated the no AEIs is scheduled for newly acquired Belvedere Square and Provident Square, a CAPEX of HK$50mn to HK$100mn per year is expected for Fortune REIT.

Inorganic growth driver – Acquisitions

The rosy 2012 interim results is partly fueled by the acquisition of Belvedere Square and Provident Square. According to the management, this acquisition contributed about 10% revenue growth to the interim results. We believe this success can be replicated in FY2013/14. There are three vital factors for the success of acquisitions. i). A low interest rate environment that is expected to persist till 2014 ii). The property market boom iii) A robust Hong Kong retail sector.

The total consideration for the acquisition of Belvedere Square and Provident Square was HK$1.9 billion. HK$830mn was funded by revolver of existing facilities at 0.91% over HIBOR. Another HK$1100mn will be funded by term loan of new facilities at 2.0% over HIBOR. With the currently 12M HIBOR of 0.871%, the estimated effective interest rate for the acquisition will be approximately 2.41%. The 2010 annualized net property income yield for the new properties is 4.2%. This implies Fortune REIT could immediately enjoy a yield spread of 1.79% upon completion.

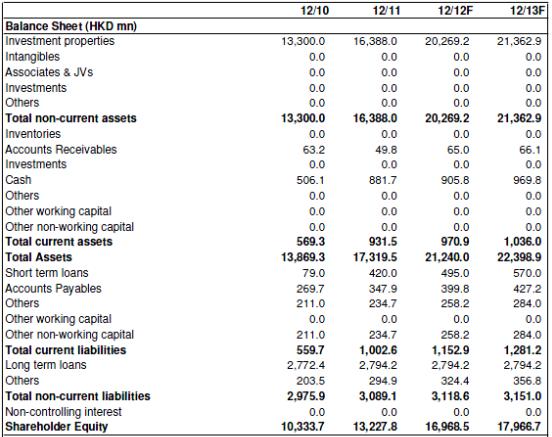

Meanwhile, the booming property market buoyed the valuation of the properties portfolio. From FY2009 to FY2011, portfolio valuation surged from HK$11,500 mn to HK$16,388 mn, representing a CAGR of 21.1%. The soaring valuation reduced the gearing ratio of Fortune REIT. As at 30 Jun 2012, the gearing ratio of Fortune REIT was 24.5%. Debt headroom was HK$3 billion before the 35% gearing limited, which paving the way for future acquisitions. As a result, we expected further acquisition to be announced by Fortune REIT in FY2013/14.

Solid fundamentals

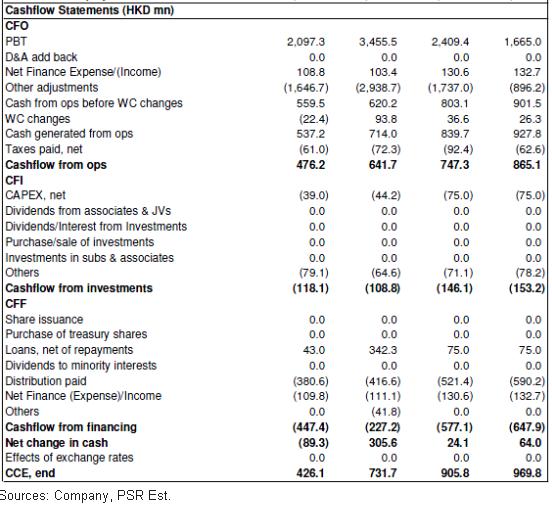

As at 30 Jun 2012, gearing ratio of Fortune REIT came in 24.5% (FY2011 industrial average: 22.8%), 10.5% below the 35% gearing limited. The available liquidity totaled HK$975 mn; in which HK$310 mn from committed RCF and HK$665 mn from cash on hand. Meanwhile, effective interest cost reduced to 2.77%. (FY2011:3.65%) The growth of net property income and cash flow was robust from FY2009 – 1H2012. It is worth noticing that the both growth rate were in the same pace, which ensure the distribution ability of Fortune REIT. Furthermore, market cap of Fortune REIT exceeded US$1 billion in July 2012. This will allow more international institutional investors to invest in Fortune REIT. As Hong Kong dollar is currently pegged to U.S dollar, it reduced the currency risk for foreign investors and made Fortune REIT an ideal save heaven for global capital.

Valuation

On dividend yield basis, Fortune REIT is currently trading at approximately 24% discount to Link REIT (823 HK). As we forecast that DPS of Fortune REIT will increase at an annual rate of approximately 10% from FY2012 - FY2013, we expect the current yield spread between Fortune REIT and Link REIT to reduce further.

Meanwhile, as at 30 Jun 2012, the dividend yield of HS REIT index was 5.9%. As the HS REIT index hold a diversified portfolio of REITs, it's dividend yield may proxy the required rate of return (discount rate) of Fortune REIT. By using the H-model dividend discount model, the theoretical share price of Fortune REIT is HK$7.88.

We forecast the FY2012 leading dividend yield of Fortune REIT to be 4.7% with DPS of HK$31 cents. The last price of HK$5.44 implies a leading dividend yield of 5.6% and represents a approximately 20% upside potential. We upgrade our 12-month target price of Fortune REIT to HK$6.53 with a “BUY” rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()