-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Tasly Pharmaceutical Group (600535.CH) - Positive Results for DSP FDA Phase III Trials

Friday, January 13, 2017  12954

12954

Tasly Pharmaceutical Group

| Recommendation | Accumulate |

| Price on Recommendation Date | $40.040 |

| Target Price | $46.000 |

Weekly Special - 002050 Sanhua

Positive Results for DSP FDA Phase III Trials

At the end of December, Tasly announced the results of the Phase III FDA randomized, double-blinded, international multi-center clinical trials of compound Danshen dripping pills (DSP): DSP has, at the primary clinical endpoint, a significant dose-effect relationship and can increase the effect of TED; the secondary endpoint of observation on curative effect supports the primary clinical endpoint, and an evidence-effect chain is formed. In the trial, a clinical study of DSP was carried out to interpret its formula basis, and its clinical safety is proved once again. No serious adverse events associated with the protocol or with DSP were observed throughout the trial period. Other general adverse events were infrequent, minor, and self-healing, and there was no difference in the incidence rate of adverse events among study groups.

The results showed that DSP can be proved to be effective under the FDA standard, and it is feasible to produce Chinese patent medicines approved by FDA under the strict GMP/GAP in the modern TCM production system. This is China's first Chinese patent medicine that completed the phase III clinical trial of FDA, marking TCM's major step toward internationalization and modernization. We expect the company will begin its listing application, and DSP to pass FDA certification and be listed in 2018.

The United States has a vast market for chronic angina pectoris, and the FDA has only certified two new drugs over the past 20 years. The latest is ranolazine (market size over USD600 million), but the side effects are great. DSP, as a botanical drug causing minor side effects, can be used for a long time and is more affordable, and is expected to take its share in the US angina pectoris market. Meanwhile, phase III results are expected to further promote DSP sales in the domestic market, since the FDA phase II trial data in 2010 has caused the revenue from DSP to increase by more than 20% in 2011 and 2012. In addition, the company will become China's international TCM platform, through which many products, such as Qilin pill, are expected to enter markets of developed countries.

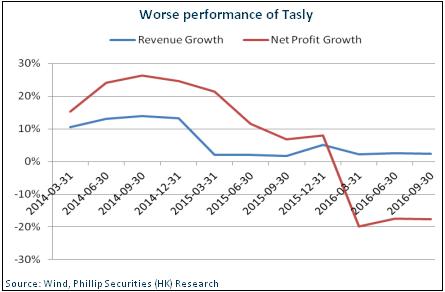

Channel Adjustment Basically Completed

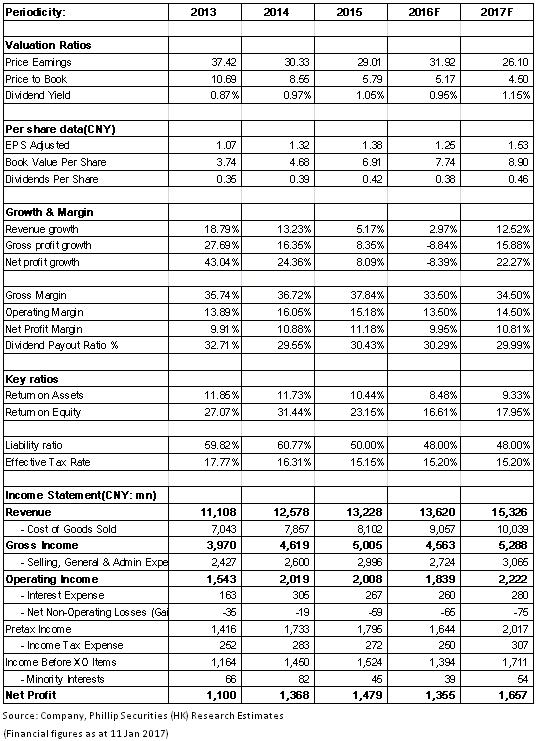

In the past two years, the growth rate of the company slowed down obviously. In the first three quarters of 2016, the revenue from the pharmaceutical industry decreased by 14.5% YoY, and so did the profit, mainly due to the company's channel structure adjustment and the strengthening of accounts receivable management. However, the company's sales volume of principal products in the hospital market has maintained growth. We expect that the company's channel adjustment has been basically completed through channel destocking in 2016. Moreover, since 2008 the tender price cut of principal products has not been not significant, indicating a slight impact on the company by the controlled medical insurance fee. It is highly probable that the pharmaceutical industry will resume its growth in 2017. Also worth mentioning is that the company's Puyouke (recombinant human prourokinase for injection), Yiqi Fumai, Salvianolic acid and other varieties are expected to enter the National Drug Reimbursement List and to achieve rapid sales growth.

Bright Prospects for Leader in TCM Modernization

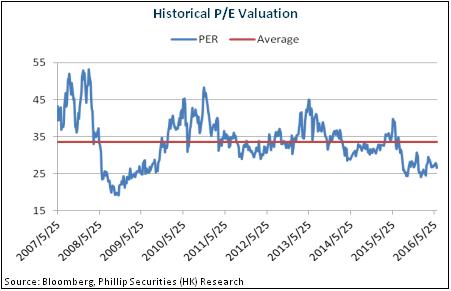

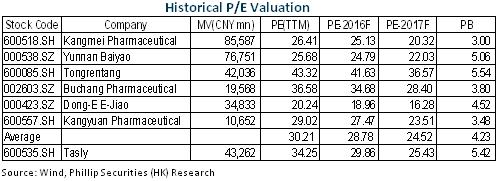

Tasly may well be the first TCM enterprise going abroad and become a leading enterprise in TCM modernization. The significantly increased brand influence, coupled with the end of channel adjustment, the company will resume its upward trend on results. In light of comparable companies, we give Tasly an estimation of 30x PE in 2017 and a 12-month target price of RMB46, with the "Accumulate" rating. (Closing price as at 11 Jan 2017)

Risks

Tender price limit;

Progress in FDA certification below expectations;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()