-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

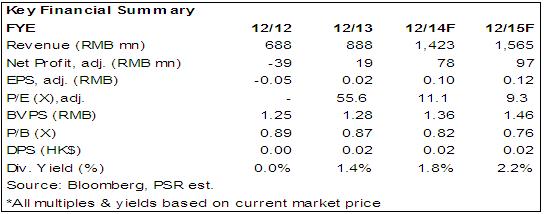

Mobi Development Co., Ltd (947.HK) - 4G Drives the Outbreak of the Performance

Tuesday, June 17, 2014  7790

7790

Mobi Development Co., Ltd(947)

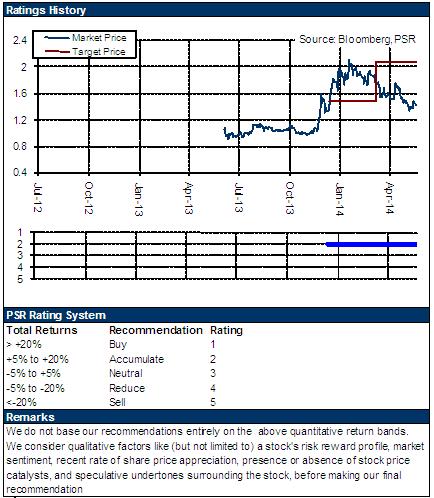

| Recommendation | Buy |

| Price on Recommendation Date | $1.400 |

| Target Price | $2.000 |

Weekly Special - 3606 Fuyao Glass

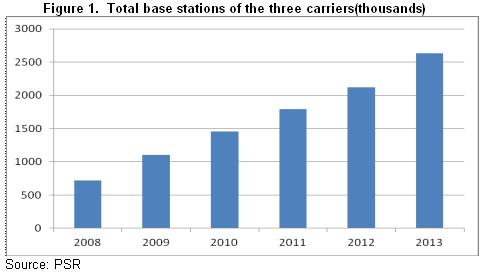

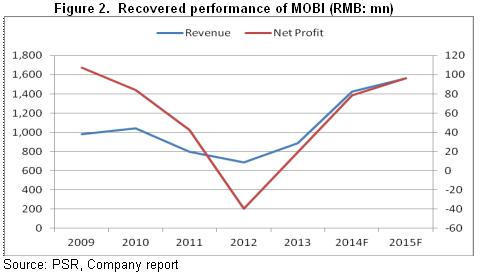

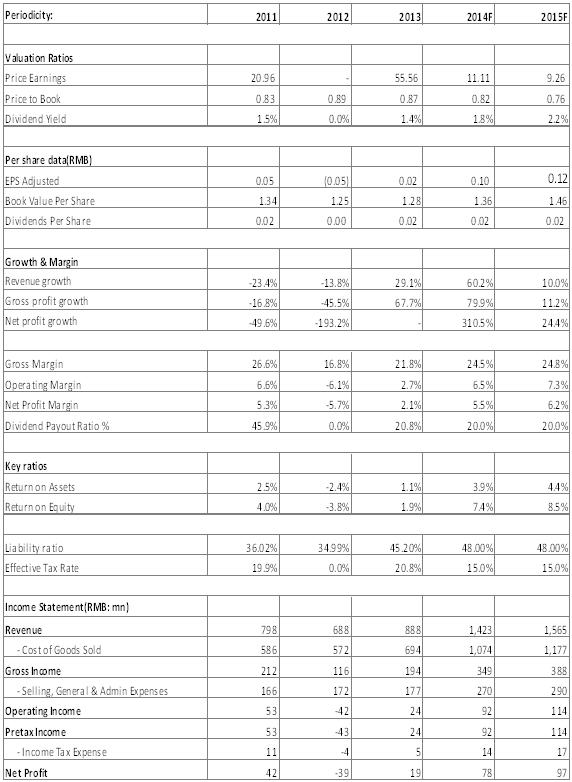

Since the second half year of 2013, especially the issuance of 4G license, domestic 4G construction has been sped up significantly. Mobi Development has grown into a supplier of aerial systems and subsystem products of radio-frequency base stations for leading equipment manufacturers with the largest share, and the share advantage has been further expanded. From the perspective of production and supply, the company has made multiple preparations, besides the substantial increase of operating personnel, it has also established a strategic partnership with the world's leading test and measurement company, Agilent Technologies Inc., which aims to establish a long-term partnership in the aspect of test and measurement devices and other technological aspects, and assists the company in expanding the capacity. In general, under the two-wheeled driving of both demand and supply, we expect that the company will realize rapid growth of performance in 2014, close to the peak in 3G era.

At the end of April, the Ministry of Industry and Information Technology indicated that three basic telecommunication enterprises were discussing to organize a communication facility company jointly, which took responsibility for planning the construction of communication towers as a whole, further enhancing the level of constructing and sharing telecommunication infrastructure together. For this reason, the market worries that corresponding demands will shrink, leading to the worry about the growth of Mobi Development and other companies. However, in terms of the current situation that the country just plans to found the State Tower Company, it is still a relatively long process to realize the reduction of demand on towers, therefore, its medium and long-term influence is extremely limited.

MIMO technology may guide the new development of the company. Currently, domestic companies with MIMO technology and mass production capacity are numbered, only Huawei, Mobi, etc., while most of other companies still lie in the stage of initial research and development. Therefore, the company will possess a starting technological superiority. Secondly, in the era of 4G, radio frequency resources are expensive and limited, so the most effective method of enhancing network performance is multi-input multi-output (MIMO) technology, especially in the aspect of sharing base stations in the future, it is more likely to accelerate such processes. Thirdly, MIMO antenna has strong profitability. Its cost is expected to increase several decades of percents, while the price is expected to rise by several times.

Investment Action

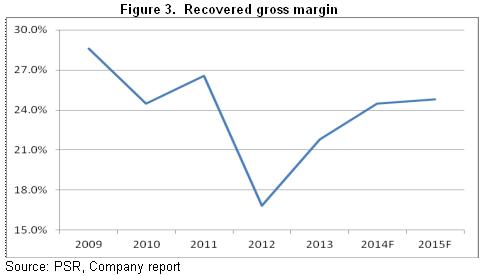

4G can provide the company with the opportunity of regaining growth. The company made a profit instead of suffering a loss in 2013, and it is expected to accelerate its growth and worth looking forward to the performance in 2014. In the aspect of valuation, the company's valuation has been decreasing since it was listed, and the price-to- book ratio was as low as 0.36 times previously. We think the company's valuation is expected to return to a normal level under the new market opportunity and competitive situation. We temporarily give it 1 times corresponding to the valuation of book value per share in 2015, with the target price of 2 HKD and the "Buy" rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()