-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Guangzhou Baiyunshan Pharma (600332.CH) - Private placement will lend Wong Lo Kat a hand in expanding

Monday, January 19, 2015  22726

22726

Guangzhou Baiyunshan Pharma(600332)

| Recommendation | Hold |

| Price on Recommendation Date | $31.120 |

| Target Price | $31.750 |

Weekly Special - 002050 Sanhua

Guangzhou Baiyunshan Pharma (Baiyunshan) has formed three business segments of Massive Health, Big South Pharmaceutical, Big Commerce, becoming a highly potential leader in health industry. The Company has apparent advantages for its brands, and has greatly evident advantages for Chinese patent medicine resources in the South China, even in the whole country.

The Company announced an equity plan to issue 419 million shares for A shares, covering 24.5% of the post-issued total capital stock , at a price of RMB 23.8 per share, with the scale up to RMB10 billion. After winning over in the first trial of rights for the red-canned decoration, combined with the investment of RMB4 billion by private placement, Wong Lo Kat's adequate capital is positive for a substantial enhancement and its share may enlarge. Meanwhile, its earning capability is expected to go upwards benefiting from scale effect and expense ratio decreasing.

On October 28, the Company's anti-ED generic drug Jinge was officially listed. We believe, by virtue of its high cost performance ratio, coupled with advantages of brands, quality and OTC channels, Jinge is expected to burgeon up to RMB 500 to 1,000 million in coming 3 to 5 years. Compared with the branded drug, the price of Jinge decreases by 30% for the same dose, and the price for the single medication even declines by more than 60%, which highlights its price advantage.

Rating “Hold” for reasonable evaluation

Though the private placement lends Wong Lo Kat a hand in expanding the market, Jinge perhaps will be a magnet in growing, Baiyunshan still doesn`t have a brand realizing net profit of more than RMB 100 million except the brand Wong Lo Kat, so its original high-quality brands remain to be explored. Not taking the private placement into consideration temporarily, we grant it 25X 2015EPS, and the target price can be CNY 31.75, with “Hold” rating initially.

Brand advantages support growth spurt

After the amalgamation in July 2013 and going listed on the stock market as a whole, Baiyunshan has formed three business segments of Massive Health, Big South Pharmaceutical, Big Commerce, becoming a highly potential leader in health industry. The Company's business in the three segments is rather balanced, with their revenue contribution in 1H14 at 39.2%, 37.3%, and 23.5% respectively.

It's worth being pointed out that the Company enjoys apparent advantages for its brands. Guangzhou Pharmaceutical Group Co., Ltd currently has authorized the company to use the brand Wong Lo Kat, which has a brand value of RMB 108.015 billion in 2010, becoming the top brand in China. Meanwhile, the reputation and praises for its brand "Baiyunshan" are renowned throughout China. Besides, Zhongyi, Chan Li Chai, Qixing, Jingxiu Tang, Pan Gaoshou that are subordinate to the company are all century-old. Moreover, Baiyunshan has Chinese patent medicines such as Huatuo Resuscitative Pill, Zhongyi Diabete Pill, Xiasangju, Fritillary Bulb Extract Oral Liquid, Bak Foong Pills, Zhui Feng Tou Gu Pill etc., and has greatly evident advantages for Chinese patent medicine resources in the South China, even in the whole country.

On this base, the Company has actualized speeding up in recent years. Adding up with before-amalgamated Guangzhou Pharmaceutical and Baiyunshan, the CAGR of its revenue and net profit from 2009 to 2013 was respectively 28% and 34%. In the first three quarters of 2014, the company achieved the revenue and net profit of RMB 14.64 billion and RMB 856 million respectively, with 10.8% and 17.7% YOY change, showing persistent growing trend.

Private placement will lend Wong Lo Kat a hand in expanding

Baiyunshan announced an equity plan to issue 419 million shares for A shares, covering 24.5% of the post-issued total capital stock, at a price of RMB 23.8 per share, with the scale up to RMB10 billion, to be in locked-deposit for three years, and big shareholders along with relative parties etc. will fund RMB 6.5 billion in total, and Yunfeng Fund and the employees will fund RMB 500 million respectively, which shows their confidence for the company's long-term development. What is worth noting is that the company will invest RMB 4 billion by private placement to the Wong Lo Kat health business, which can help enhance Wong Lo Kat's competitiveness. However, other projects such as R&D, e-commerce businesses etc. are mainly focused on a long-term development, but may cause dilution effect in a short-term.

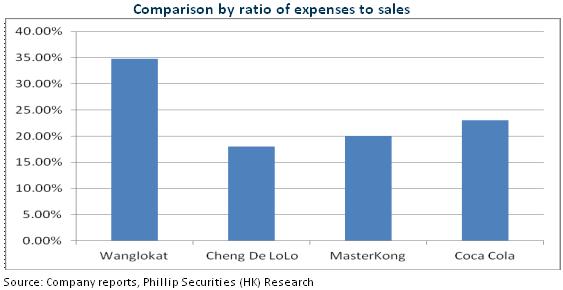

The Company announced the first-trial verdict of the red can packaging decoration dispute case that Guangzhou Pharmaceutical Group Co., Ltd won the lawsuit in December, 2014, and then JDB immediately expressed the appeal to the Supreme People's Court. The final verdict is expected to be clear in 1Q15, and we are still optimistic. Since the failure in the red can decoration right verdict, JDB's dealers have been faced with the risks of banned sales and stock loss. In contrast, plus the input of 4 billion Yuan, Wong Lo Kat's adequate capital is positive for a substantial enhancement, the market share of Wong Lo Kat is expected to continue to rise, thus changing the current structure of the two sides with basically equal market shares.

At the same time, its profitability is also expected to rise. First, it will benefit from the release of scale effect; second, the homogeneity competition between JDB and Wong Lo Kat made the operating expense ratio of both sides all exceed 30%. But after the court ruling, it is not rational for JDB to continue the long-term high input, and it may be forced to take the strategy of dissimilation competition. So, at that time, expense ratio may have the space to decrease. It is also worth noting that, Guangzhou Pharmaceutical Group Co., Ltd previously pledged to transfer Wong Lo Kat series of trademarks to the listed Company according to law within two years of the transferable date after the settlement of the legal dispute of Wong Lo Kat trademarks. We expect that the Company may obtain the ownership of Wong Lo Kat trademarks in 2015 and then will not need to pay the trademark licensing fees, and also will further improve the net profit margin ratio.

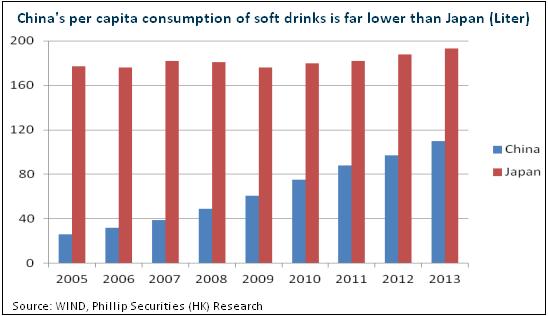

Compared with international market, China's per capita consumption of soft drinks is still low, for example, it is only about 60% of Japan's level, which indicates that it still has the space to increase. Furthermore, carbonated drinks suffer a declined popularity due to health consideration, and are expected to be replaced by other drinks including tea drinks to some extent. Therefore, Wong Lo Kat is expected to realize a continuous growth of more than 10%.

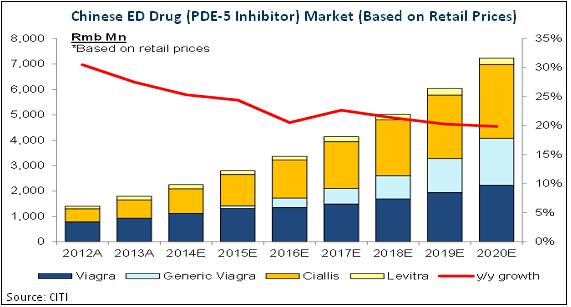

Jinge is expected to face soared demand

On October 28, the Company's anti-ED generic drug Jinge was officially listed. We believe, by virtue of high cost performance ratio, coupled with advantages of brands, quality and OTC channels, Jinge's sales is expected to increase to RMB 500 million to 1 billion in the next 3 to 5 years.

In July, 2014, Pfizer Viagra's patent of ED application in China expired. Generally speaking, due to the price disadvantage after patent expiration, many original drugs are difficult to survive, and the market share of generic drugs in China accounts for about 97%. Compared with the original products, the price of the Company's Jinge decreases by 30% for the same dose, and the price for the single medication even declines by more than 60%, which highlights the price advantage.

In China, there are about 140 million ED patients. But since the pricing of anti-ED drugs is high which requires more than 100 Yuan for 1 time (1 pill), it greatly depresses the demands of domestic patients. In future, with the declining of price, the demands may be released, and the potential market size may reach the level of ten billion Yuan. But the market size at present is only 1 to 2 billion Yuan which manifests that it still has a great space of growth. In addition, the Company's Jinge was developed under the guidance of the "Viagra Father," Dr. Ferid Murad, thus ensuring the product quality from the source.

Catalyst

The right to use the trademark of Wong Lo Kat be injected into the Company;

Positive progress obtained with the lawsuit;

The implementation of equity incentive plan.

Risks

Lawsuit failure;

Difficult integration for diversified businesses.

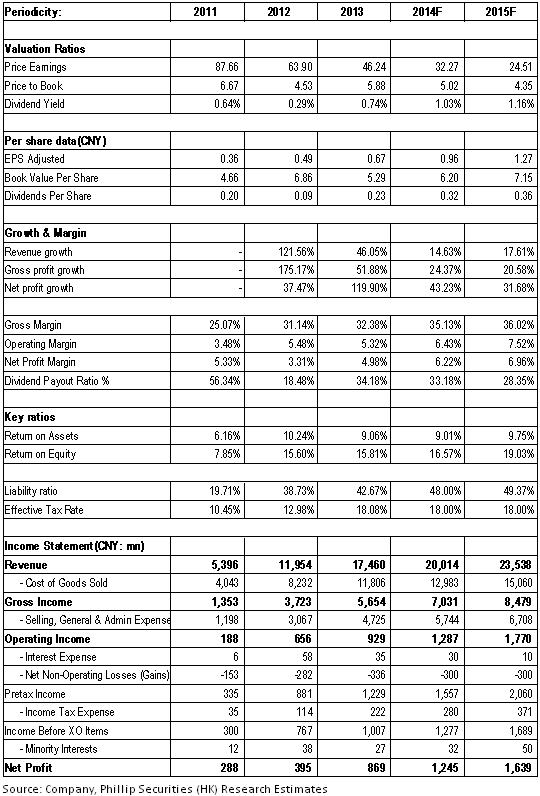

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()