-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

GCL New Energy (451.HK) - Rapid Increase of Installed Capacity

Thursday, June 18, 2015  8615

8615

GCL New Energy(451)

| Recommendation | Buy |

| Price on Recommendation Date | $0.760 |

| Target Price | $1.610 |

Weekly Special - 2333 Great Wall Motor

A Power Plant Platform under GCL

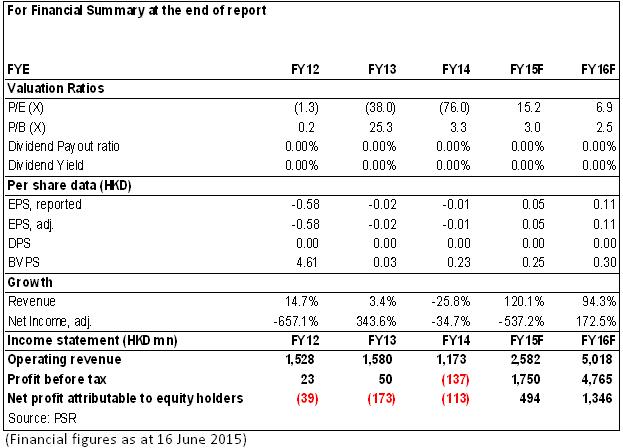

The company is a platform for PV power plant EPC and operation under GCL-POLY, was listed through buying a shell on May 9, 2014 and included in MSCI Hong Kong Index Constituent Stocks on Nov. 13. In 2014, the company recorded revenues of HK$1.173 billion, with loss attributable to the shareholders being HK$113 million. The main reason was that PV projects only contributed HK$800,000 to its revenues for the whole year while its business results relied mostly on previous Printed Circuit Board (PCB).

Rapid Increase of Newly Installed Capacity

By the end of 2014, the company had an installed capacity of 615MW, and planned to increase installed capacity in the next three years by 2GW, 2.5GW and 3GW respectively through self-construction, joint development and acquisition. Among new projects to be implemented in 2015, 30% is for self-construction and most are joint development and acquisition but the company plans to increase the proportion of self-construction power plants and is enlarging its team. It is estimated that the company can generate and connect 500MW to the grid in H1 this year, taking the power plant capacity connected to the grid up to 1.1GW.

High Efficiency of Power Generation

There is no power restriction issue in the company's projects connected to the grid, with equity IRR above 12% and Generating Equipment Availability Hours of about 1200 hours. When choosing projects In the future, the Company will avoid those in West China where there are long hours of sunshine and more power restrictions, and put more projects in the middle of the country. In additions, the company also has projects of distributed power generation, such as “Fishing and PV Generation” and “Grazing and PV Generation”, which generate high yields, electricity sale income, agriculture income and subsidy from the government. It is promising for the distributed generation to spread widely.

Multiple Modes of Financing

Besides bank loans to get financed, the company has also issued convertible bonds, which helped reduce the financing cost. What's more, it also formed a joint venture of assets management with Galaxy Capital to raise fund, as well as the fund support from GCL-POLY. For the future, the company plans to raise funds in the form of Yield Co. The diversified modes of financing help the company have lower financial cost than other companies in the industry.

Valuation

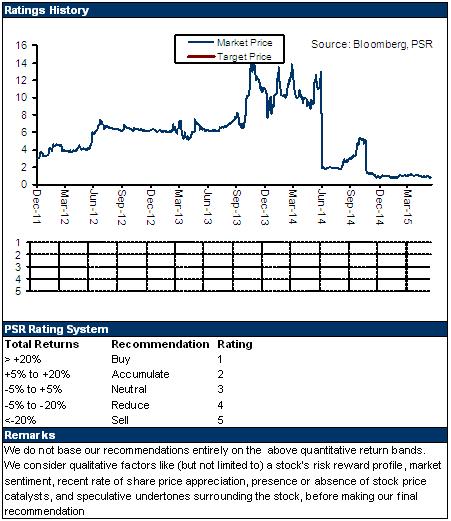

With the backing up of GCL, the company has technology advantages in PV power plant construction and operation while enjoying the preference of material supply from GCL-POLY and GCL System Integration. The three years to come will see the company have a significant increase of installed capacity. Calculated on the basis of 2.6GW and 35% net profit margin to be achieved supposedly at the end of 2015, the company is estimated to record revenues of HK$3.333 billion from electricity sales and net profit of HK$1.167 billion for the electricity sale operaion. Without considering convertible bonds, its current stock price is 8.8X PE. We set its target price for the next 12 months at HK$1.61, equivalent to 15X PE expected for 2016. We give the company a “Buy” rating. (Closing price as at 16 June 2015)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()