-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CR Double-Crane (600062.CH) - Sales from Major Products Will Grow Rapidly

Wednesday, November 23, 2016  20848

20848

CR Double-Crane(600062)

| Recommendation | Accumulate |

| Price on Recommendation Date | $23.080 |

| Target Price | $27.520 |

Weekly Special - 002050 Sanhua

Steady Growth in the First Three Quarters

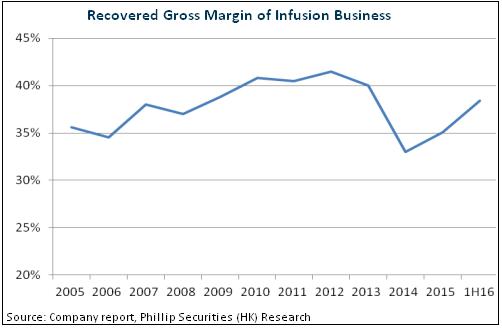

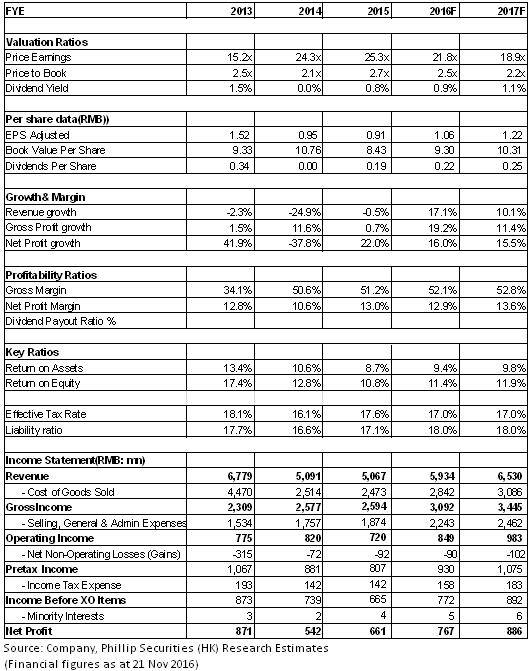

In the first three quarters, China Resources Double-Crane Pharmaceutical Co., Ltd. achieved a revenue of RMB4.15 billion, representing an increase of 9.3% YoY, a net profit of RMB600 million, increased by 7.8% YoY, and a net profit excluding non-recurring gains and losses of RMB570 million, soared by 43.3% YoY. The total gross margin amounted to 51.9% YoY, slightly increased by 0.4%. Specifically, the revenue from the Infusion businesses reached RMB1.58 billion, down 11.3% YoY. But thanks to structural optimization and the increased proportion of nutritional and therapeutic infusion business which has high gross margin rate, the gross margin rate of infusion businesses increased by 4% YoY.

In addition, the revenue from non-infusion businesses reached RMB2.49 billion, soared by 29.5% YoY. Since the company merged and acquired China Resources Saike Pharmaceutical Co., Ltd. and Jinan Limin Pharmaceutical Co., Ltd. in 2015, the extensive growth has become one of the main growth engines. Specifically, the revenue from cardiovascular, endocrine, pediatric medication businesses increased by 25.3%, 6% and 12.7% YoY, respectively. The company's overall expense remained stable, while ratio of marketing expense ratio and administrative expense ratio were 22% and 11.8%, both increased by approximately 0.5% YoY.

Sales from Major Products Are Expected to Grow Rapidly

First, the company continues to carry out structural adjustment of infusion businesses. The proportion of nutritional and therapeutic infusion business has increased from 16.6% in 2011 to 25%. The proportion of plastic-bottle infusion has decreased from nearly 80% in 2011 to around 40%, but that of soft-bag infusion has increased to 20% and that of soft-bag (817) and other infusion was approaching 30%. And CR Double-Crane is the only company with BFS manufacturing technique (blow molding - filling - sealing). Though currently the production is subjected to insufficient bids, it is expected to gradually increase. And now the type of package material consists of more than 50% of the infusion package materials in Europe, so its future market demand will be huge. Structural adjustment will also contribute to the continuous improvement of profitability.

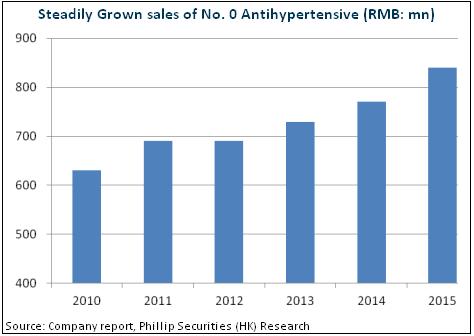

Second, since China cancelled the price ceiling for low-cost drugs and included their prescription in the hospital performance assessment in 2014, the price of No. 0 Antihypertensive, one of the company's core low-cost preparations, not only remained stable, but increased slightly as well with an annual average price increasing by 6-10%. There is still a substantial increase in the price space, which will help contribute to its 10-15% annual revenue growth.

Third, National Reimbursement Drug List (NRDL) adjustment is just around the corner with focuses on local supplementary lists and children's medicines, and the company's pitvastatin and calsurf may be put on the NRDL. Pitavastatin, which has been included in the extended reimbursement drug lists of 11 provinces such as Beijing, Gansu and Guangdong, reached a sales volume of 26.56 million in 2015, rocketed by 124% YoY, and a sales revenue of over RMB100 million. In 1H 2016, the growth rate reached 74.1%. If the drug is included in NRDL, then its sales scale is expected to maintain rapid growth for the next two years, hopefully exceeding RMB500 million. Also, calsurf, as a children's medicine benefiting from market expansion and policy support, is expected to enter NRDL and the growth rate may be above 30%.

External Merger & Acquisition to Expand Business

CR Double-Crane is the only chemical drug + bio-drug platform affiliated to China Resources Pharmaceutical Group Limited, so it is highly probable that it will expand external business. After listed in HKEX, CR Pharmaceutical plans to allocate HKD3.35 billion to buy manufacturers of Chinese biological drug, traditional Chinese medicine and chemical medicine, and the target transaction scale will not be less than RMB50 million, which may increase medicine varieties and business performance for its affiliates like CR Double-Crane.

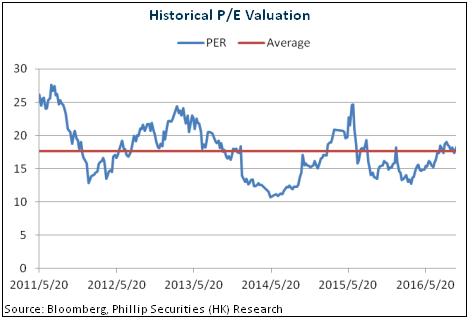

In short, the company will maintain a double-digit growth in revenue, and the profitability may see an improvement, together with the expected new profits brought by external M&A, we expect the company's performance to grow at an annual rate of 15-20%. We grant it 20x EPS in 2017 and the target price is RMB27.52, with the "Accumulate" initially. (Closing price at 21 Nov 2016)

Risks

Decrease in infusion businesses exceeds expectation;

Extensive acquisition fails to meet the expectation.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()