-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

SAIC Motor (600104.CH) - An Undisputed Industry Leader, with stable growth & opportunities

Friday, January 16, 2015  16265

16265

SAIC Motor(600104)

| Recommendation | Accumulate |

| Price on Recommendation Date | $24.670 |

| Target Price | $28.800 |

Weekly Special - 1171 YANKUANG ENERGY GROUP COMPANY LIMITED

An Undisputed Industry Leader

SAIC Motor is the largest automaker in China, with its major businesses covering the entire manufacturing of passenger vehicle and commercial vehicle, components&parts, after-market businesses such as automobile logistics, telematics, second-hand car and automobile finance. The company is an undisputed leader in Chinese automobile market. The total sales of SAIC in 2014 upped 10.07% yoy to 5.62 million units, which took up 23.9% of Chinese automobile market with the growth rate being higher than the average by 3.2 ppts. In 2014, in terms of sales volumes, Shanghai Volkswagen, Shanghai GM and SGMW occupied No. 2, No. 3 and No. 6 respectively in the 2014 Bestsellers list of China Passenger Vehicle market.

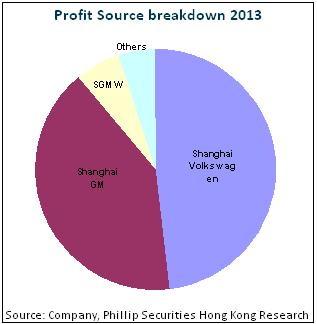

Shanghai Volkswagen and Shanghai GM: “Profit-Cows” with Excellent Profitability

SAIC's JVs Shanghai Volkswagen and Shanghai GM have developed in China for years, which respectively represent German and American vehicle, have good brand images and product reputations, and possess solid market status and strong competitiveness. The two assets give rich returns to SAIC and contribute most of company profit sources. In the first three quarters of 2014, the company reported a net profit of RMB20.4 billion, to which the jvs contributed 20.6 billion. In the following three years, the launch of new models of the two joint ventures will still gradually speed up. As the market leaders they will continue to benefit from the adjustment of competition structure and the exertion of scale effect. On the whole, product structure and profit margin of two joint ventures are expected to improve.

Self-owned brands and new energy vehicles are still in the market cultivation period

However, influenced by the larger environment that the competition among domestic self-owned brands is becoming increasingly fierce, as well as its weakening product lines, the sales of SAIC self-owned brands fluctuated in recent years. The higher initial investment, R&D and depreciation and the lower utilization rate made its self-owned brand vehicles continue to lose money. However, we still expected that MG-GS, the first mini SUV model of MG, which is to be launched in 2015, will take a share of the profits in the hot future domestic mini SUV market.

SAIC is walking in the forefront of the domestic manufacturers in terms of the new energy vehicles. Currently, it has made the batch production for the three new energy models of Roewe 750 hybrids, Roewe 550 plug-in hybrids and Roewe E50 pure electric cars. Its subordinate enterprise, SunWin Bus, also owns buses using hybrid power, pure electric power and fuel cell. Laying equal stress on multiple technological routes and continuous capital and technology investment provides the company with the first mover advantage and relatively low risk in the new energy field.

High dividend payout rate is likely to continue and SOE reform expand its imagination

The company has abundant cash flow. In the first three quarters of 2014, the net cash flow of operation activities is 20.374 billion yuan, 31.40% higher than the same period last year. And the cash in accounts is close to 90 billion yuan, with 73.5 billion yuan of unallocated profits. We predict that the relatively high cash dividend rate (about 50%) of the company is likely to continue. After the new management layer takes office, the SOE reform aiming at stimulating the follow-up development motivation is likely to go further, having a certain imagination space in resource allocation, diversified ownership reform and long-term incentive mechanism.

Investment Thesis

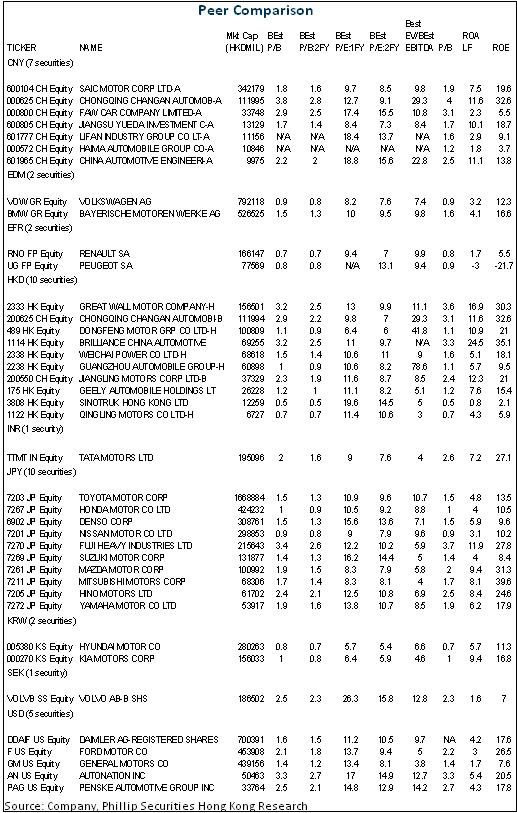

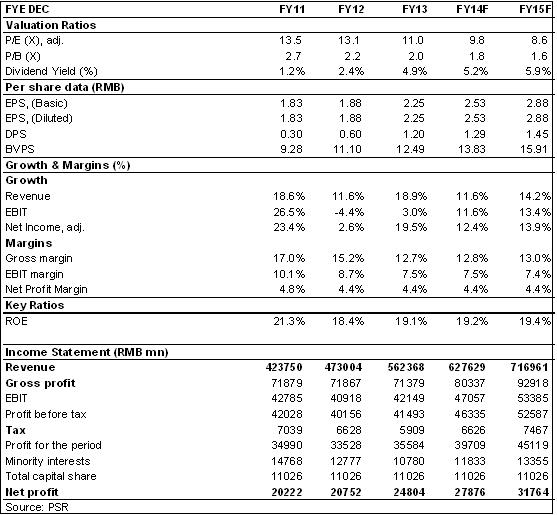

As analyzed hereinbefore, we think that SAIC can still obtain a relatively fast profit growth by virtue of scale effect under the condition that its overall sales grows stably. As analyzed above, we revised EPS expectation of the Company to RMB 2.53 and 2.88 of 2014/2015. And we accordingly gave the target price to 28.8, respectively 11.4/10x P/E and 2.1/1.8x P/B for 2014/2015. "Accumulate" rating.

Company Profile

SAIC Motor is the largest automaker in China, with its major businesses covering the entire manufacturing of passenger vehicle and commercial vehicle, research and development as well as production and sale of components and parts ( including engine gearbox, power transmission, chassis, interior and exterior decoration, electronic appliance, etc. ), meanwhile including automobile service trade businesses such as automobile logistics, telematics, second-hand car and after-market businesses such as automobile finance. At the end of 1997, the company had launched IPO in A Stock. By the end of 2014, the total capital stocks of company have reached 11 billion shares, of which Shanghai Automotive Industry Corp (Group) held 73%. SAIC's affiliated vehicle companies include Shanghai Volkswagen, Shanghai GM, SGMW, Morris Garages which mainly operates its self-owned passenger vehicle brand Roewe and MG, NAVECO, SAIC IVECO Hongyan and Shanghai Sunwin. In addition, HUAYU Auto (600741 CH) launched in A Stock is also the component manufacturer controlled by the company.

An Undisputed Industry Leader

The company is an undisputed leader in Chinese automobile market. In 2013, the company ranked No. 85 in world's top 500 enterprises for its consolidated sales revenue of 92 billion dollars. The total sales of SAIC in 2014 upped 10.07% yoy to 5.62 million units, which took up 23.9% of Chinese automobile market with the growth rate being higher than the average by 3.2 ppts.

The company respectively held 50% of equities of two largest domestic sedan joint ventures---Shanghai Volkswagen and Shanghai GM. In the whole year of 2014, these two joint ventures sold 3.4852 million units vehicle in total, accounting for about 18% of Chinese passenger vehicle market, among which the sales of passenger vehicle of Shanghai Volkswagen and Shanghai GM upped 13% yoy and 9.4% yoy respectively to 1.725 million units and 1.724 million units. SGMW with its 50% of equities held by the company is the largest domestic mini-bus manufacturer. In 2014, its sales upped 13% yoy to 1.806 million units, among which the shipment number of passenger vehicle was 933 thousand units, up 56.3% yoy.

In 2014, in terms of sales volumes, Shanghai Volkswagen, Shanghai GM and SGMW occupied No. 2, No. 3 and No. 6 respectively in the 2014 Bestsellers list of China Passenger Vehicle market. SAIC's products cover all market levels ranging from high-end premium car to economy sedan as well as market segments such as high-performance premium sedan, MPV, SUV, HEV and electric vehicle.

Shanghai Volkswagen and Shanghai GM: “Profit-Cows” with Excellent Profitability

Shanghai Volkswagen, founded in 1984, is in the first batch of Sino-foreign sedan joint ventures after China's reform and opening up in the 1980s. Currently, it has two brands which are Volkswagen and Skoda, with 17 vehicle model series. Established in 1997, Shanghai GM emerged in a trend of Pudong development since the 1990s. At present, it owns three brands which are Buick, Chevrolet and Cadillac, with 29 vehicle model series. Furthermore, two companies have developed in China for years, which respectively represent German and American vehicle, have good brand images and product reputations, and possess solid market status and strong competitiveness.

The two assets give rich returns to SAIC and contribute most of company profit sources. In the first three quarters of 2014, the company reported a net profit of RMB20.4 billion, to which the joint ventures contributed 20.6 billion.

In the following three years, the launch of new models of the two joint ventures will still gradually speed up. Shanghai Volkswagen will launch five new models in succession (Lamando, New Passat, New Touran, Santana Hatchback, Fabia). Shanghai GM will also launch new vehicle models such as Cadillac DTS, a changed generation of Buick Regal and Lacrosse, a new generation Malibu of Chevrolet. The mid-size SUV Buick Envision which has just been launched has a good sales prospect and will become another growth point in 2015. Additionally, as a new comer in Chinese premium car market, Cadillac is developing Chinese entry-level premium car market and is expected to obtain rapid development of premium car market in the future.

From the perspective of competition, although it has gone through a rapid development for more than a decade, currently, the sales of Chinese top ten passenger vehicle manufacturers take up 61% of the total sales. Compared with developed countries, the concentration ratio is not high. With the slowdown of overall Chinese automobile market, it is estimated that the industrial concentration ratio will gradually improve. As the market leaders they will continue to benefit from the adjustment of competition structure and the exertion of scale effect. On the whole, product structure and profit margin of two joint ventures are expected to improve.

SGMW: Benefiting from the Increasing Popularity of Domestic MPV Market

SGMW, established in 2002, has two brands, Baojun and Wuling, with 15 vehicle series covering the low-end market. Benefiting from the popularity of mini-car market, Wuling Sunshine and Wuling Rongguang sold 873,236 units new vehicle in total in 2014 with the market share of about 50% estimated, which won championship for nine years successively in mini-car sales. And benefiting from the continuous well-selling of MPV Wuling Hongguang and the rapid growth of new vehicle sales of Baojun 730 family car with seven seats, the sales of passenger vehicle still performed well. In December, the monthly sales of Wuling Hongguang were 75.9 thousand units, reaching a record high of monthly sales among all vehicle models so far. Moreover, the monthly sales of Baojun 730 also continuously exceeded 30 thousand units.

Self-owned brands and new energy vehicles are still in the market cultivation period

The self-owned brands car producer SAIC was founded in 2007. Currently, it has two major brands of Roewe and MG, with 10 series of models. Its core technology mainly comes from British Rover's 75 platform and 25 platform as well as the technology property of all the engines acquired by SAIC in 2005. Relying on the positioning of producing the cars for the younger and a sense of modern technology as well as the strong support from Shanghai government, the Roewe developed rapidly in 2009 and 2010. However, influenced by the larger environment that the competition among domestic self-owned brands is becoming increasingly fierce, as well as its weakening product lines, the sales of SAIC self-owned brands fluctuated in recent years. In 2014, a total of 0.18 million vehicles were sold yearly, with the yoy decline exceeding 20%. The higher initial investment, R&D and depreciation and the lower utilization rate made its self-owned brand vehicles continue to lose money. However, we still expected that MG-GS, the first mini SUV model of MG, which is to be launched in 2015, will take a share of the profits in the hot future domestic mini SUV market.

SAIC is walking in the forefront of the domestic manufacturers in terms of the new energy vehicles. Currently, it has made the batch production for the three new energy models of Roewe 750 hybrids, Roewe 550 plug-in hybrids and Roewe E50 pure electric cars, among which, Roewe 550 plug-in hybrids applied the battery and the electric drive system of self-owned research and development, with the comprehensive oil saving rate of more than 70%. Its subordinate enterprise, SunWin Bus, also owns buses using hybrid power, pure electric power and fuel cell. Laying equal stress on multiple technological routes and continuous capital and technology investment provides the company with the first mover advantage and relatively low risk in the new energy field.

High dividend payout rate is likely to continue and the state-owned enterprise reform may expand the imagination space

The company has abundant cash flow. In the first three quarters of 2014, the net cash flow of operation activities is 20.374 billion yuan, 31.40% higher than the same period last year. And the cash in accounts is close to 90 billion yuan, with 73.5 billion yuan of unallocated profits. We predict that the relatively high cash dividend rate (about 50%) of the company is likely to continue.

In the aspect of state-owned enterprise reform, as the giant state-owned enterprise of Shanghai, after the new management layer takes its new post, the state-owned enterprise reform aiming at stimulating the follow-up development motivation is likely to go further, having a certain imagination space in resource allocation, diversified ownership reform and long-term incentive mechanism.

Valuation

As analyzed hereinbefore, we think that SAIC can still obtain a relatively fast profit growth by virtue of scale effect under the condition that its overall sales grows stably. As analyzed above, we revised EPS expectation of the Company to RMB 2.53 and 2.88 of 2014/2015. And we accordingly gave the target price to 28.8, respectively 11.4/10x P/E and 2.1/1.8x P/B for 2014/2015. "Accumulate" rating.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()