-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

LK (600388.SH) - Purchased by Sunshine Group at a premium, ushering in a new stage of development

Wednesday, June 28, 2017  18418

18418

LK(600388)

| Recommendation | Buy |

| Price on Recommendation Date | $15.040 |

| Target Price | $18.400 |

Weekly Special - 2333 Great Wall Motor

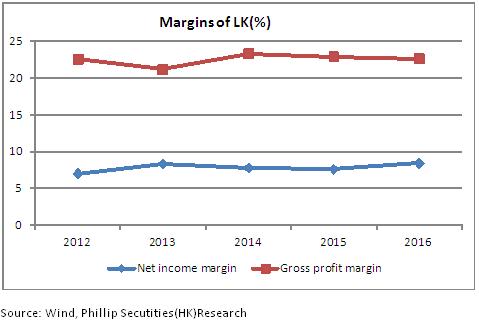

The cost was controlled well, and the gross profit was basically stable.

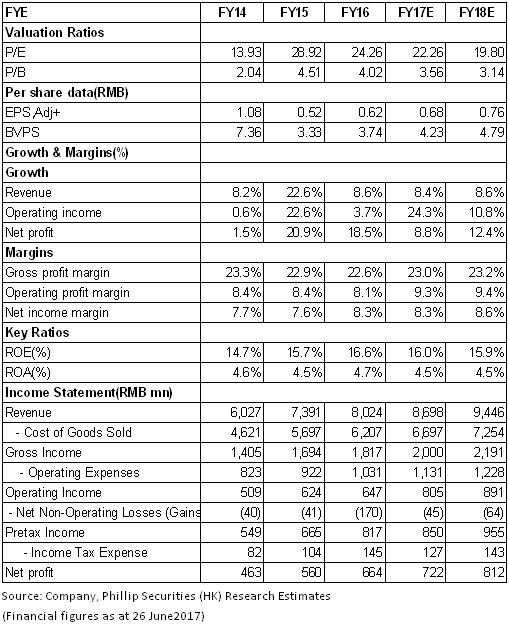

In 2016, the company's revenue jumped by 8.56% yoy to RMB8.024 billion; the net profit excluding non-recurring items attributable to the parent company increased by 18.52% yoy to RMB0.663 billion. Basic EPS was RMB0.62, increasing by 19.23% yoy. The profits were basically in line with its expectations. The results increased quarter by quarter. In Q4, results reached RMB3.09 billion, and the net profit attributable to the parent company was RMB0.234 billion. In 2017 Q1, the company's result positively increased. The revenues increased by 0.25% yoy to RMB1.143 billion; the net profit excluding non-recurring items attributable to the parent company grew by 3.58% yoy to RMB75 million.

Specifically, by expanding development space, the vacuum cleaner project, desulfurization and denitration project kept steady growth, which were the main sources of the result growth. The revenues were RMB4.266 billion (+6.2%) and RMB3.33 billion (+14.57%), respectively. The gross profit margins were 25.1% and 21.4%, respectively. The share acquisition of desulfurization catalyst business from joint venture parties was completed. And the revenue soared by 54.88% to RMB73 million.

In respect of cost, the increase was 8.94%, slightly higher than the increase of revenue. The gross profit margin decreased slightly by 0.27%, which was mainly affected by the decline of that of real estate and overseas EPC project. During the period, the expense was RMB1.031 billion; the expense ratio was 12.85%, slightly up by 0.38 percentage point over last year. The net profit reached 8.37%, mainly affected by the one-off non-operating revenue of RMB137 million.

The contracts in hand were abundant; the foundation of sustainable development was solid.

The amount of orders in 2016 was RMB10.2billion, including RMB5.5 billion of vacuum cleaning, RMB3.2 billion of desulfurization and denitration. As the end of the period, the amount of the orders in hand was RMB16.1 billion. The overall bid rate of the project was 44.9%. In 2017 Q1, the amount of orders was RMB2.7 billion. At the end of the period, the amount of orders in hand was RMB17.5 billion. Facing the situations of excess capacity of flue and gas treatment in power industry and fierce competitions among peer companies, the future business is confronted with many difficulties. However, the company's excellent technology and brand image, the abundant contracts in hand, the strong executive force and the active layout in non-electric projects lay solid foundations for the sustainable development in the future.

Sunshine Group purchased Longking at a premium, showing its great value.

In June 1, the company announced that Sunshine Group and its persons acting on concert purchased Eastright Investment at a price of RMB3.67 billion and indirectly held 17.17% of the company's stocks. Each share was nearly RMB20, nearly 60% higher than RMB12.77 before suspension. The premium mainly reflects the company's current business level, brand and technological research and development capabilities, profitability and the ability of valuation. Longking Co., Ltd has long been committed to the field of controlling air pollution. The purchase of Sunshine Group aims to working in environment protection industry and creates a comprehensive empire of environment protection. We believe that the purchase by Sunshine Group at a premium reflects its exploration and recognition of the company's value. With the experience of the Group's capital operation, the company will usher in a new development. Furthermore, Sunshine Group will increase its holdings of RMB0.5 billion to RMB1 billion of the company's stocks in the next year, showing its confidence to the long-term development of the company.

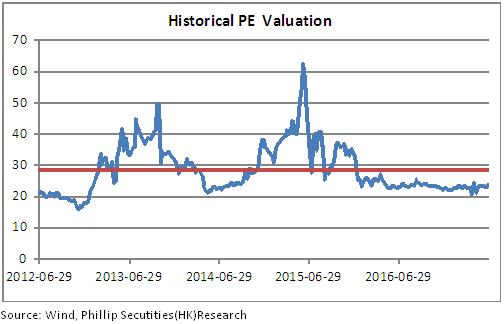

Valuation and Rating

At present, the project of flue and gas treatment in electricity industry is in the peak of implementation. On the contrary, there is still a broad market space in non-electricity industry. Based on technology, brand image and first layout, the company is expected to further increase the market share. We predict that the company's revenue in 2017-2018 will reach RMB8.7 billion and RMB9.4 billion, respectively. The net profit will be RMB0.72 billion and RMB0.81 billion, respectively. The EPS will be RMB0.68 billion and RMB0.76 billion,respectively. We will give the target price of RMB18.4 and the rating is Buy. (Closing price as at 26 June 2017)

Risk Warnings

Upward price of raw materials;

Risk of refunding;

Risk of macro-policy;

Fierce competition in the industry;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()