-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Huayu Auto (600741.CH)-Undervalued Industry Leader

Tuesday, August 11, 2015  6466

6466

Huayu Auto(600741)

| Price on Recommendation Date | $17.140 |

| Target Price | $21.300 |

Weekly Special - 002050 Sanhua

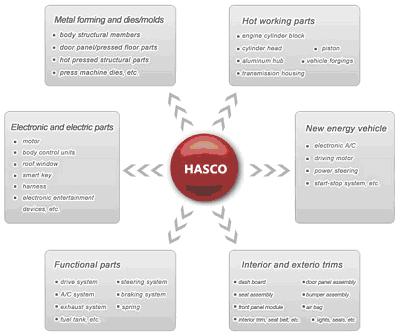

With its headquarters in Shanghai, HUAYU Automotive Systems (HASCO) mainly operates in R&D, manufacturing and selling of auto parts, which are the key areas of the auto parts and components business. Its six major business lines include metal forming and dies / molds, interior and exterior trimming parts, electronic and electric parts, functional parts, hot working parts and new energy vehicle parts. The Company was previously under the auto components business of SAIC. It is the key auto components platform of SAIC.

HASCO is the pioneer of China`s auto component industry. It is a listed integrated auto parts and components supplier, with the largest production capacity, the most comprehensive product offering, the broadest customer coverage and the strongest R&D capability in China. Many of its joint ventures companies, which are set up by SAIC with the world`s leading auto parts and components players, are the leaders in their respective sub-segments. As of the end of 2014, the subsidiaries and related companies of HASCO have established 261 R&D, manufacturing and service bases in China. 14 manufacturing bases have also been set up in various overseas countries, such as USA, Germany, Thailand, Russia, Australia, Czech and India. As its businesses sprawl across broad segments that cover both the Chinese and overseas market, it starts to enjoy the benefits of clustering effects.

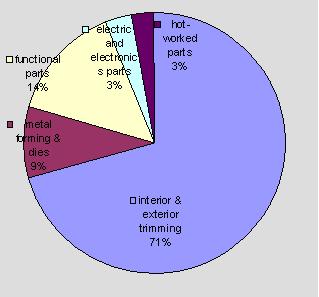

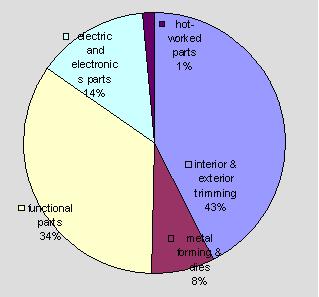

As for breakdown of profit by business lines, functional parts and interior & exterior trimming parts are the two largest profit contributors, accounting for 43% and 36% of total profits. Electronic and electric parts rank the third with 10% of profit contribution. Metal forming and dies / molds and hot working parts account for a total of 10% profit. As for the breakdown of profit contribution by invested companies, Yanfeng Visteon Automotive Trim Systems is the major profit centre, contributing to over 70% of HASCO`s sales revenue and 47% of net profit.

HASCO has set up a clear strategy of `Zero level, neutral, Global`. It has gradually identified and prioritized foci of its future development, namely: the company will continue grow its core businesses through a combination of outward expansion and organic growth, so that it can foster transformation and upgrade of these business lines to support sustainable growth. The completion of acquiring 50% stake in Yanfeng Visteon Automotive Trim Systems in 2013 signaled that the company has entered into a `Post-JV` strategic transformation. We believe that to attract customers, auto manufacturers will tend to apply more high-end and high-technology auto parts and components in their automobiles. This trend will certainly benefit top-tier auto parts manufacturers such as HASCO.

Hasco`s Business Segment

HASCO has 31 directly invested companies in total, including world renowned enterprises such as Yanfeng Visteon Automotive Trim Systems Co., Ltd., Shanghai Koito Automotive Lamp Co., Ltd., Shanghai Valeo Automotive Electrical Systems Co., Ltd., Shanghai Sanden Behr Automotive Air Condition Co., Ltd., Shanghai GKN Drive Shaft Co., Ltd., ZF Shanghai Steering Systems Co., Ltd. As its customers are more concentrated, its top 5 customers contributed to 62.5% of total sales in 2014. HASCO has 62 related companies which are awarded the status of `high-tech enterprises`.

The major customers of the company are top auto manufacturers in China. It has established stable and long-term strategic relationships with SAIC, FAW Group, DFPSA, Chang`an Automobile, GAC, BAIC Group, BMW Brilliance, Great Wall Motor, JAC Motors, etc. The company possesses an integrative competitiveness in quality, service, technology and price (QSTP) and hence attaining a higher profitability than the industry average.

HASCO has built up a rather comprehensive supply chain of auto parts and components. As of the end of 2014, the subsidiaries and related companies of HASCO have established 261 R&D, manufacturing and service bases in China. 14 manufacturing bases have also been set up in various overseas countries, such as USA, Germany, Thailand, Russia, Australia, Czech and India. As its businesses sprawl across broad segments that cover both the Chinese and overseas market, it starts to enjoy the benefits of clustering effects.

As for breakdown of profit by business lines, functional parts and interior & exterior trimming parts are the two largest profit contributors, accounting for 43% and 36% of total profits. Electronic and electric parts rank the third with 10% of profit contribution. Metal forming and dies / molds and hot working parts account for a total of 10% profit. As for the breakdown of profit contribution by invested companies, Yanfeng Visteon Automotive Trim Systems is the major profit centre, contributing to over 70% of HASCO`s sales revenue and 47% of net profit.

Revenue breakdown by Segments

Profit breakdown by Segments

As China`s overall auto sales growth steadily slows down, demand for quality auto products will gradually increase. Competition among auto manufacturers will become fiercer. To attract customers, auto manufacturers will tend to apply more high-end and high-technology auto parts and components in their automobiles. This trend will certainly benefit top-tier auto parts manufacturers such as HASCO. In an industry where impact of the economies of scale is significant, companies` profit can be improved through the increase in market share.

Besides, HASCO plans to strengthen the partnership and restructuring of the global interior trimming parts business of Johnson Controls. The ultimate plan is to set up the world`s largest interior trimming parts company, with HASCO holding a 70% stake to secure its leading global position in the business. While its overseas business just accounts for a small portion of the total business with 1.6% revenue contribution, we look forward to its future growth potential.

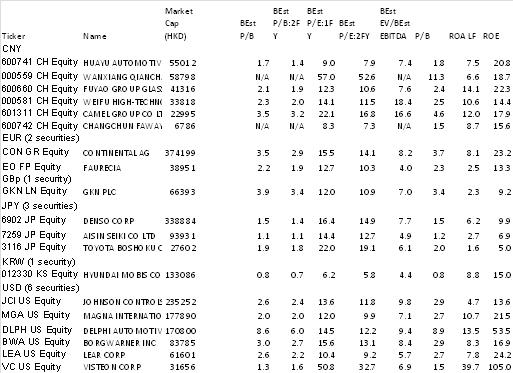

Peer Comparison

HASCO is the pioneer of China`s auto component industry. It is a listed integrated auto parts and components supplier, with the largest production capacity, the most comprehensive product offering, the broadest customer coverage and the strongest R&D capability in China. Many of its joint ventures companies, which are set up by SAIC with the world`s leading auto parts and components players, are the leaders in their respective sub-segments. As of the end of 2014, the subsidiaries and related companies of HASCO have established 261 R&D, manufacturing and service bases in China. 14 manufacturing bases have also been set up in various overseas countries, such as USA, Germany, Thailand, Russia, Australia, Czech and India. As its businesses sprawl across broad segments that cover both the Chinese and overseas market, it starts to enjoy the benefits of clustering effects.

As for breakdown of profit by business lines, functional parts and interior & exterior trimming parts are the two largest profit contributors, accounting for 43% and 36% of total profits. Electronic and electric parts rank the third with 10% of profit contribution. Metal forming and dies / molds and hot working parts account for a total of 10% profit. As for the breakdown of profit contribution by invested companies, Yanfeng Visteon Automotive Trim Systems is the major profit centre, contributing to over 70% of HASCO`s sales revenue and 47% of net profit.

HASCO has set up a clear strategy of `Zero level, neutral, Global`. It has gradually identified and prioritized foci of its future development, namely: the company will continue grow its core businesses through a combination of outward expansion and organic growth, so that it can foster transformation and upgrade of these business lines to support sustainable growth. The completion of acquiring 50% stake in Yanfeng Visteon Automotive Trim Systems in 2013 signaled that the company has entered into a `Post-JV` strategic transformation. We believe that to attract customers, auto manufacturers will tend to apply more high-end and high-technology auto parts and components in their automobiles. This trend will certainly benefit top-tier auto parts manufacturers such as HASCO.

Investment Thesis

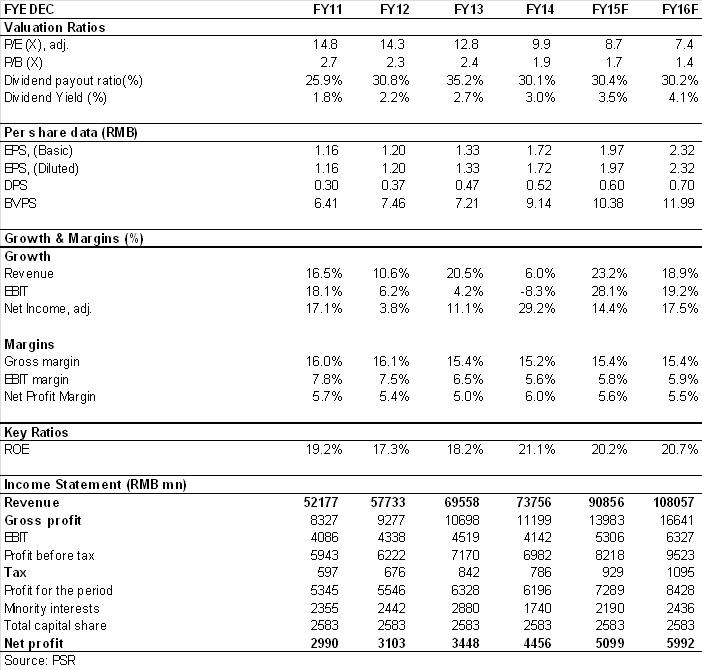

As analyzed above, we revised EPS expectation of the Company to RMB 1.97 and 2.32 of 2015/2016. And we accordingly gave the target price to 21.3, respectively 10.8/9.2x P/E for 2015/2016. `Buy` rating.(Financial figures as at 7 August 2015)Company Profile

With its headquarters in Shanghai, HUAYU Automotive Systems (HASCO) mainly operates in R&D, manufacturing and selling of auto parts, which are the key areas of the auto parts and components business. Its six major business lines include metal forming and dies / molds, interior and exterior trimming parts, electronic and electric parts, functional parts, hot working parts and new energy vehicle parts.Hasco`s Business Segment

HASCO has 31 directly invested companies in total, including world renowned enterprises such as Yanfeng Visteon Automotive Trim Systems Co., Ltd., Shanghai Koito Automotive Lamp Co., Ltd., Shanghai Valeo Automotive Electrical Systems Co., Ltd., Shanghai Sanden Behr Automotive Air Condition Co., Ltd., Shanghai GKN Drive Shaft Co., Ltd., ZF Shanghai Steering Systems Co., Ltd. As its customers are more concentrated, its top 5 customers contributed to 62.5% of total sales in 2014. HASCO has 62 related companies which are awarded the status of `high-tech enterprises`.

Three Core Competitive Advantages to Secure its Leading Position

HASCO is the pioneer of China`s auto component industry. It is a listed integrated auto parts and components supplier, with the largest production capacity, the most comprehensive product offering, the broadest customer coverage and the strongest R&D capability in China. Many of its joint ventures companies, which are set up by SAIC with the world`s leading auto parts and components players, are the leaders in their respective sub-segments.The major customers of the company are top auto manufacturers in China. It has established stable and long-term strategic relationships with SAIC, FAW Group, DFPSA, Chang`an Automobile, GAC, BAIC Group, BMW Brilliance, Great Wall Motor, JAC Motors, etc. The company possesses an integrative competitiveness in quality, service, technology and price (QSTP) and hence attaining a higher profitability than the industry average.

HASCO has built up a rather comprehensive supply chain of auto parts and components. As of the end of 2014, the subsidiaries and related companies of HASCO have established 261 R&D, manufacturing and service bases in China. 14 manufacturing bases have also been set up in various overseas countries, such as USA, Germany, Thailand, Russia, Australia, Czech and India. As its businesses sprawl across broad segments that cover both the Chinese and overseas market, it starts to enjoy the benefits of clustering effects.

As for breakdown of profit by business lines, functional parts and interior & exterior trimming parts are the two largest profit contributors, accounting for 43% and 36% of total profits. Electronic and electric parts rank the third with 10% of profit contribution. Metal forming and dies / molds and hot working parts account for a total of 10% profit. As for the breakdown of profit contribution by invested companies, Yanfeng Visteon Automotive Trim Systems is the major profit centre, contributing to over 70% of HASCO`s sales revenue and 47% of net profit.

Revenue breakdown by Segments

Profit breakdown by Segments

Steady Progress of `Post-JV era` Strategic Transformation

Through the competitive advantage of forming long-term partnership with global auto parts leaders, HASCO has set up a clear strategy of `Zero level, neutral, Global`. It has gradually identified and prioritized foci of its future development, namely: the company will continue grow its core businesses through a combination of outward expansion and organic growth, so that it can foster transformation and upgrade of these business lines to support sustainable growth. The completion of acquiring 50% stake in Yanfeng Visteon Automotive Trim Systems in 2013 signaled that the company has entered into a `Post-JV` strategic transformation.As China`s overall auto sales growth steadily slows down, demand for quality auto products will gradually increase. Competition among auto manufacturers will become fiercer. To attract customers, auto manufacturers will tend to apply more high-end and high-technology auto parts and components in their automobiles. This trend will certainly benefit top-tier auto parts manufacturers such as HASCO. In an industry where impact of the economies of scale is significant, companies` profit can be improved through the increase in market share.

Besides, HASCO plans to strengthen the partnership and restructuring of the global interior trimming parts business of Johnson Controls. The ultimate plan is to set up the world`s largest interior trimming parts company, with HASCO holding a 70% stake to secure its leading global position in the business. While its overseas business just accounts for a small portion of the total business with 1.6% revenue contribution, we look forward to its future growth potential.

Valuation

As analyzed above, we revised EPS expectation of the Company to RMB 1.97 and 2.32 of 2015/2016. And we accordingly gave the target price to 21.3, respectively 10.8/9.2x P/E for 2015/2016. `Buy` rating.Peer Comparison

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()