-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Kerry Properties (683.HK) - Gradual Shift to Property Development in China

Thursday, February 2, 2017  22497

22497

Kerry Properties(683)

| Recommendation | Buy |

| Price on Recommendation Date | $22.050 |

| Target Price | $26.400 |

Weekly Special - 002050 Sanhua

Investment Summary

- Several large projects in Hong Kong and China are expected to be completed in 2017, expecting to bring large revenue to the company

- Strong cooperation with Shangri-La in hotel business in its expansion in China

- Large and expanding property investment segment, which generates stable cash flow to the company

Company Overview

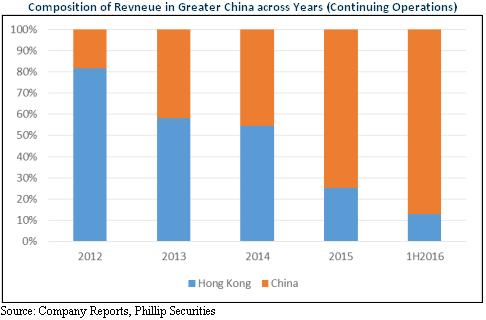

Kerry Properties is a property development and investment company and operates in both Hong Kong and China. Originally, Kerry Properties had a large logistics segment but ever since 2013 the segment has been spin-off and listed in Hong Kong Exchange as Kerry Logistics (636.HK). Therefore, Kerry Properties is now a company primarily concentrates on the property development and investment sector. Kerry Properties originally primarily operates in the property business in Hong Kong but since 2013, Kerry Properties has gradually shifted its main focus to property business in China, with its Chinese property business contributing 87% to the total revenue in 1H2016.

China Segment: Kerry Properties has about 6,856,000 square foot of investment properties, including hotels, in China, and reguarly achieves over 90% occupancy rate in major properties. Besides, the company also has property development in major cities such as Shenzhen, Shanghai and Hangzhou. In 1H2016, property development in China contributes HKD2.57Bn to the revenue, a YoY rise of 490%.

Hong Kong Segment: Kerry Properties has 2,785,000 square foot of investment properties and a majority of the GFA are for office and retail uses. Famous properties include Megabox. In terms of property development, the company targets at the high class residential property development in area such as Ho Man Tin and Kowloon Tong.

Increasing Exposure in China

Kerry Properties has a rapid increase in exposure in China since 2015. Both property development and investment property achieved significant growth, in terms of revenue. Other than the ordinary property development and investment business, Kerry Properties has a hotel segment operation in China, which contributes to about 15% of the total revenue. The hotel segment also had sizable growth and achieved a 13% increase in revenue in 1H2016.

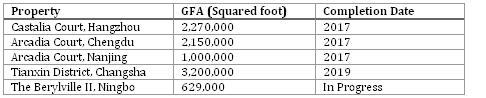

Property Development: The revenue from property development in China rose 490% in 1H2016 is due to the completion of several property construction projects, thereby allowing the recognition of revenue. In terms of property under development, the company has projects in many different cities in China, such as Shenzhen, Hangzhou and Nanjing, and has a large floor area being constructed. Selected properties under development include:

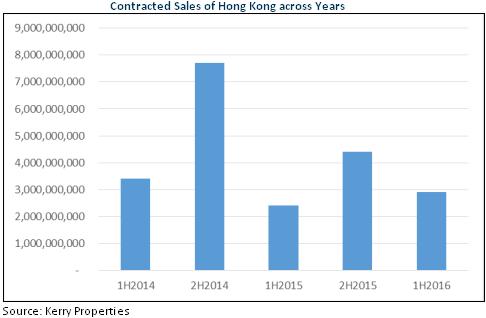

The above properties are primarily residential property development. At the same time, the company has many more integrated property complex, which consists of residential, commercial and retail components and they are in major cities such as Shenzhen and Hangzhou. Besides, the company's contracted sales has been on a steadily improving trend and the company has achieved the highest contracted sales in 1H2016 across recent years.

In 1H2016, the contracted sales in China was HKD7.2Bn, which is larger than the total recognised sales of HKD5.5Bn. Upon the completion of the property construction projects, we believe that the contracted sales will be gradually recognised and reflected in the income statement, assuring the stability of the company's operating results in the future.

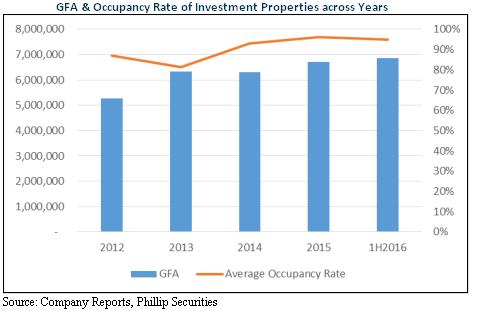

Property Investment: The portfolio of investment property in China is large and expanding. In 1H2016, the revenue generated from property investment grew 10% while the total GFA only grew 1.8%, from 6,738,000 square feet to 6,856,000 square feet, signaling an increase in average rent especially occupancy rate has stayed roughly constant. Selected investment properties are as follow:

The company has achieved, on average, over 90% occupancy in its major properties especially commercial and retail properties, which achieve over 95% occupancy rate in the last two years. Residential investment property relatively underperformed but still achieves on average 87% occupancy rate in both 2015 and 1H2016. With its investment properties being located in cities with high demand, such as Shanghai, Beijing and Shenzhen, we expect the high occupancy trend to continue and Kerry Properties can generate stable income from the existing properties.

Some of the investment properties under development are as follow:

We expect the property projects under development, such as the Shenzhen, project, to bring sizable rental income to the company especially Qianhai in Shenzhen is one of the most focused business district by the Chinese government. Other integrated complex projects such as those in Hangzhou and Shenyang are also expected to bring stable cash flow to the company as well as diversify away the risk as they include retail, commercial and residential spaces for leasing.

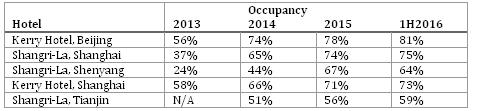

Hotel: Kerry Properties has strong cooperation with Shangri-La, the well-known hotel resort operators in the world and many of the hotels developed by Kerry Properties are managed and operated by Shangri-La. Major hotel properties include:

The company has a few integrated complex, which consists of hotels not only named as Kerry Hotel, but also hotels jointly developed and managed by Shangri-La and named after Shangri-La. The following is the summary of hotels currently under development:

Some of the hotels under development are managed by Shangri-La. We expect that Kerry Properties can leverage on the brand name of Shangri-La and generate stable cash flow from the current hotels and the future hotels.

High End Property Developer in Hong Kong

Kerry Properties primarily engages in the property development sector in Hong Kong and most of the properties developed by the company are located in the wealthy regions of Hong Kong. The property development segment however had an 85% drop in revenue because no construction projects were completed in 1H2016. Property investment achieved a 17% growth in revenue, which is mainly caused by the completion of renovation of a residential investment property in April 2015.

Property Investment: According to annual report 2015, Kerry Properties has 16 investment properties in Hong Kong, with the portfolio of properties spanning across residential, commercial and retail sectors. The total GFA of investment properties stay constant at around 2,785,000 square foot in 1H2016 but the revenue associated with the segment has increased, which is caused by an additional investment property put into use in April 2015. The following is the summary of large investment properties:

We expect property investment segment to generate stable cash flow and revenue to the company. However, we expect the room for growth is limited because of the constant GFA and the potential for growth is exhausted due to the high occupancy achieved in previous years.

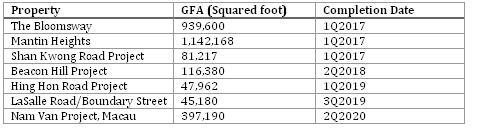

Property Development: The property development in Hong Kong recorded significant drop in revenue. This is mainly caused by the fact that no properties were completed in 2016. The company currently has 7 property development projects under development, with GFA of about 2,769,697 square foot. Most of the properties, about 2,279,365 square foot or 82% of the GFA, are expected to be completed before 2018.

With 3 properties scheduled to be completed in 2017, we expect the revenue from property development segment in Hong Kong to be large in 2017, especially the contracted sales of the large projects, The Bloomsway and Martin Heights, have already started its pre-sales as early as in 2H2015. Therefore, the revenue and cash flow in 2017 is expected to be sizable.

Future Outlook

China Market: The Chinese property market has been hot throughout 2016, leading to the Chinese government to adopt several cooling down policies and regulations to the property market.

- Policies include loan limitation, quantity limitation and increasing down payment ratio

- The policies have brought price adjustment and stabilisation in several large cities such as Shenzhen, Shanghai and Beijing

- According to statistics by Fang.com, the price for new apartment in Tier 1 cities has reduced its rate of growth

- In some Tier 2 cities, the rate of growth has started levelling off and stay stable at current level

We expect Kerry Properties to continue to perform well in the Chinese property market for the following reasons:

- The projects are geographically diversified across China and are usually integrated complex of hotels, offices, retail and residential properties

- Property investment represents a significant proportion of the company's revenue, reducing the company's exposure to the tightening regulation in the property development segment

- The company made large contracted sales, securing revenue ahead of the regulation tightening in October 2016.

With the large property development project reserve and investment properties in China, we expect China to continue to be the main driver of revenue growth and main source of income for the company. In fact, the investment properties in major cities especially the one in Qianhai, Shenzhen, which is currently under development, are full of potential and is the main focus of the Chinese government, allowing the company to generate sizable cash flow and revenue from these properties.

Hong Kong Market: The Hong Kong property market has been on a low transaction volume, in comparison with the high transaction volume achieved in the early years of the decade. The reasons for the low transaction volume could be summarized below:

- The adoption of the heavy stamp duties by the government, bringing down the transaction volume

- The expectation of a rate hike in Hong Kong in the foreseeable future, due to the relationship between HKD and USD

Property development segment is expected to be the main driver of revenue growth in Hong Kong because we believe growth of investment property segment is limited. Since high occupancy rate has been achieved but the GFA stays roughly stable, the growth potential is limited unless rent increases sharply. Comparing with China, the number of projects under development in Hong Kong is far fewer. Therefore, we expect Hong Kong segment to provide stable cash flow from its investment properties in the long term.

Financial Overview

In comparison with the property companies primarily engaging in the Chinese property sector, Kerry Properties has a relatively unlevered capital structure, with interest bearing debt contributing to only a small proportion in the capital structure. The summary of the gearing related ratio is as follow:

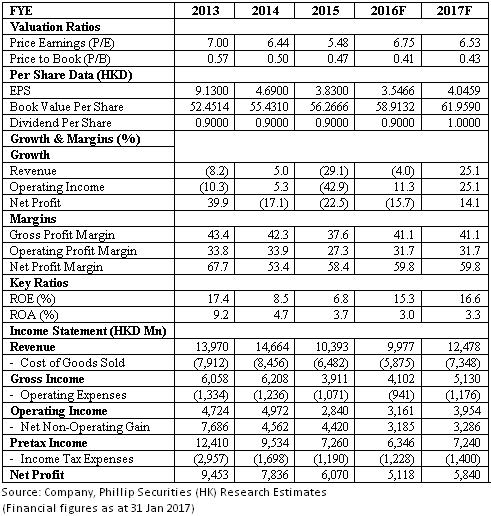

As shown from the above table, Kerry Properties's long term debt has been steadily decreasing and reach the recent ratio of about 20%. Interest coverage ratio has been deteriorating from 2013. However, the interest coverage ratio stays constant at about 14x after 2013, which is still considered to be healthy.

The profitability of Kerry Properties remain strong. In fact, the company operates in high demand cities such as Hangzhou and has a property investment business, which has high margin and provides stable source of income, hence a high overall profit margin.

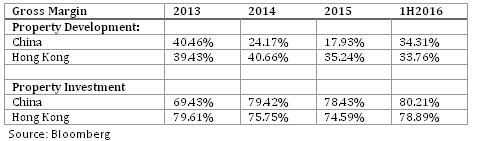

Further breaking down the gross margin, we have the following:

Property investment segment has a stable gross margin and the Hong Kong property investment yields a 79% gross margin in 1H2016. China segment performed well and rose from 69% in 2013 to 80% in 1H2016.

The gross margin of Hong Kong property development regularly stay above 30% and is due to the strategic positioning of the company in the high class residential property segment. China property development has quite a volatile gross margin and we believe it is due to the revenue arising from cities of different tiers, each having a vastly different gross margin, with Tier 1 cities having the greatest profit margin and Tier 3 cities having the lowest profit margin.

Valuation

The historical peer average P/E, P/B and P/S are 5.92x, 0.82x and 1.37x respectively. Kerry Properties's target price is therefore HKD26.40, with Buy rating assigned. (Closing price as at 31 Jan 2017)

Risk

Tightening policy in the property market

Delay in construction

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()