-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CHINA SHENGMU ORGANIC MILK (1432.HK) - Organic liquid milk the next focus

Thursday, August 28, 2014  11781

11781

CHINA SHENGMU ORGANIC MILK(1432)

| Recommendation | Accumulate |

| Price on Recommendation Date | $2.500 |

| Target Price | $2.790 |

Weekly Special - 1171 YANKUANG ENERGY GROUP COMPANY LIMITED

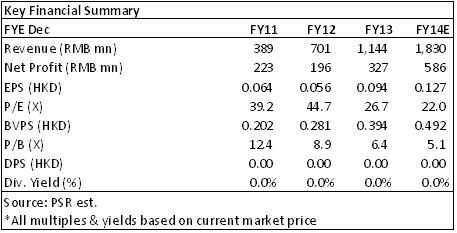

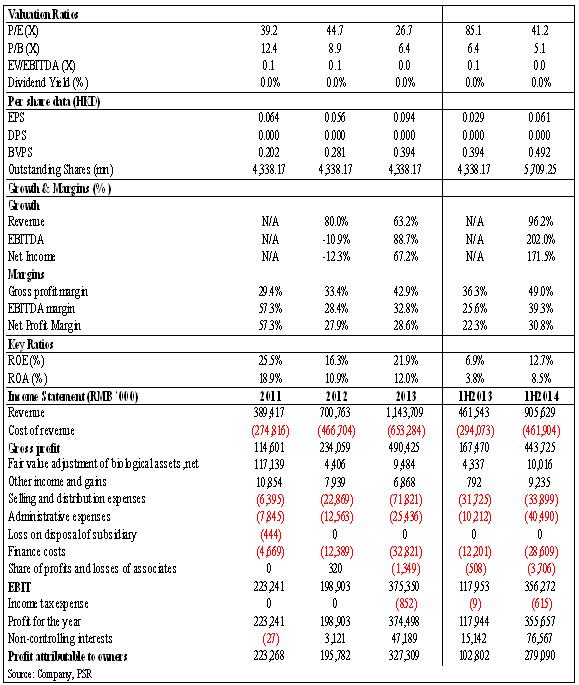

-Shengmu’s 1H14 revenue increased 96.2% yoy. Operating profit rose 202% yoy while profit attributable to owners surged 171% yoy. EPS doubled to RMB 4.9 cents.

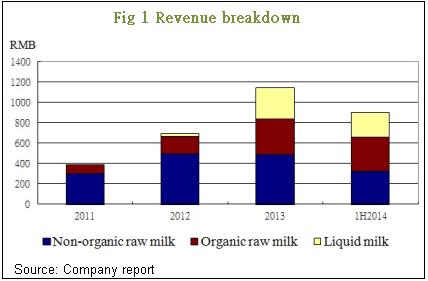

-Revenue from organic milk products, including raw milk and liquid milk obtained rapid growth of 141% and 132% yoy in revenue respectively.

-The company scheduled to shift to liquid milk production to obtain the highest gross profit margin. Management plans to double its liquid milk proportion to revenue to 60-70% in the next 3-5 years.

-We initiate a rating of “Accumulate” with target price HK$ 2.79, equivalent to 22x of 2014 forecasted EPS.

Financial Highlights

Shengmu announced its 2014 interim results that the revenue increased 96.2% yoy to RMB 906 mn, mainly due to the rapid growth of 141% and 132% yoy in organic raw milk and liquid milk revenue respectively. Gross profit surged 165% yoy to RMB 444 mn with gross profit margin up 12.7 percentage points to 49%. Operating income rose 202% yoy to RMB 356 mn while excluding the fair value adjustment income from biological assets, adjusted operating income soared 205% yoy. Profit attributable to owners for 1H surged 171% yoy to RMB 279 mn. Earnings per share amounted as RMB 0.049.

How we view this

The revenue in 1H has already reached around 79% of the total revenue in 2013. We expect the growth will continue in the 2H, since 1) management mentioned that the sales of liquid milk obtained rapid growth in both price and volume after its listing in HKEx which many distributors reported out of stock, 2) not just Shengmu, some milk producers also predicted the average milk price to go up in the 2H, and 3) the company is actively switching its product mix to liquid milk which has the highest GPM and planned to double its proportion to revenue to 60-70% in the 3-5 years.

Investment Action

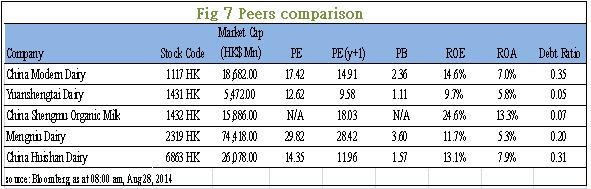

Although we found that the PE and PB of Shengmu are quite high when comparing with the upstream dairy companies, we tend to put it a bit towards the downstream manufacturer Mengniu due to the company’s future direction in liquid milk. Thus, we believe the valuation is still reasonable in this heavy investment stage. And we are quite confident with the company’s operation due to the strong background of the management. Thus, we initiate a rating of “Accumulate” with target price HK$ 2.79, equivalent to 22x of 2014 forecasted EPS.

Revenue on organic milk grew rapidly

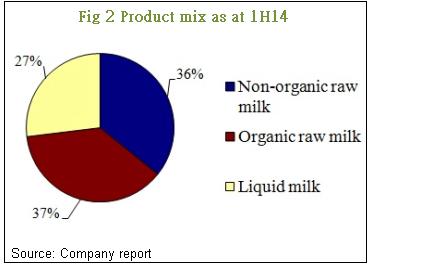

The 1H14 revenue increased 96.2% yoy to RMB 906 mn, among which the organic milk products, including raw milk and liquid milk obtained rapid growth of 141% and 132% yoy in revenue respectively. This is the first time the organic raw milk passed over the non-organic raw milk to be the largest revenue contributor. According to the company’s information, it obtained 54.2% market share and ranked as no.1 in the organic milk market in term of production volume. The management is confident at further expanding the business since the proportion of organic milk products to the whole dairy market is still low. They believe the ever-growing customers’ concerns on milk quality and healthy issue would drive up the future demand.

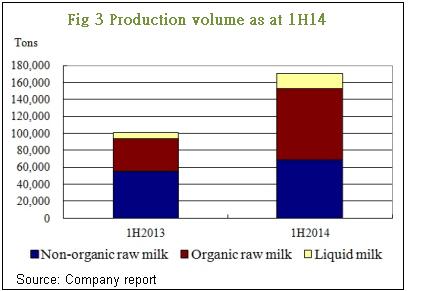

The production volume also shifted to organic milk products, which raw milk production soared 118% to 83,921 tons and liquid milk production surged 141% to 18,210 tons.

As at 1H14, there were a total of 25 farms in Inner Mongolia, of 12 non-organic farms located at Hohhot and 13 organic farms located at Ulan Buh Desert. The company plans to set up 6 new organic farms by the end of 2014 and an additional 18 organic and 3 non-organic farms in the next 3 years.

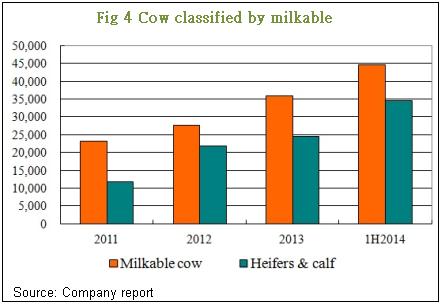

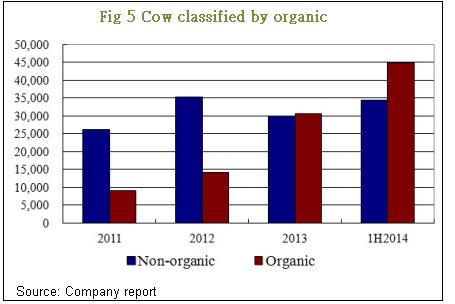

As at 1H14, there were 79,253 cows, among which 44,619 were milkable. The other 34,634 heifers & calf provide productivity in the future. With the same 79,253 cows, 44,779 are organic which shows a sharp increase of 117% of organic cows from 2012 to 2013 and another 46% growth in the 1H14.

Liquid milk the next focus

Shengmu’s main focus in the next 3-5 years is to transform itself from an upstream raw milk supplier into a milk product manufacturer, with its vertical operation of organic raw milk supply, which lowers the cost of production and confirms the raw milk quality. Management plans to double its liquid milk proportion to revenue to 60-70% during the period.

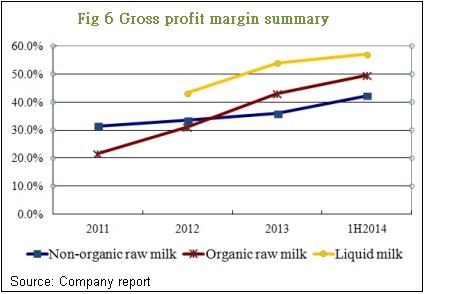

We see this as an appropriate direction of further expanding since the liquid milk obtains the highest gross profit margin among the three categories of product.

Currently the company has 4 different types of organic liquid milk, namely: organic whole milk, organic low-fat milk, organic milk for children and organic yogurt. The company is now distributing its liquid milk by different channels, such as supermarkets, department stores, convenient stores, corporate wholesale and VIP membership. Currently there are around 100,000 VIP members and its plans to have a total of 1 million loyal members in the future. It also schedules to develop the O2O network by Internet direct sales portal in the future.

Concern to company’s financial status

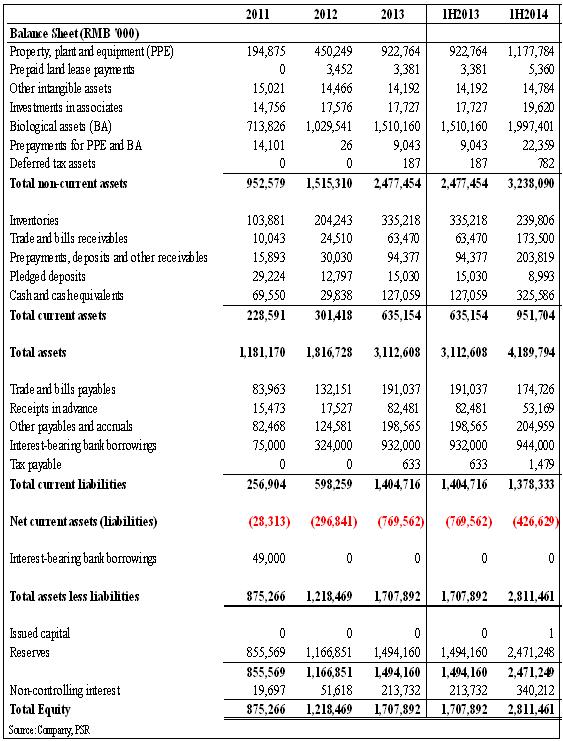

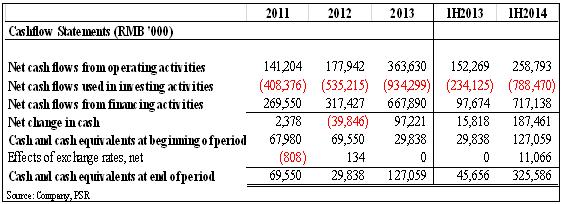

Shengmu is aggressively investing in the production facilities these year. As at 1H14, net current asset/ liability was still negative indicates heavy finance burden in the current liabilities, which interest-bearing bank loans amounted to RMB 944 mn while the cash balance was only RMB 326 mn. Currently the company is still able to get fund in financing its investment activities, we see the net change in cash flow maintains positive in 2013 and 1H14. And the cash from operation is ramping up which we forecast to have around RMB 500 mn net cash flow into the company in 2014.

Potential Risks

The company cannot maintain the quality of its organic milk products;

Selling price of Chinese organic milk not able to upgrade;

Confident on Chinese milk are low no matter in mainland or the global market.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()