-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

GREENTOWN CHINA (3900.HK) - Facing challenge but with hopeful future

Thursday, January 15, 2015  21550

21550

GREENTOWN CHINA(3900)

| Recommendation | Buy |

| Price on Recommendation Date | $7.340 |

| Target Price | $10.000 |

Weekly Special - 2333 Great Wall Motor

Sales hit target as planned

In December, the sales volume of Greentown(GT) China was RMB 13.8 billion Yuan with the total sales area of 630 thousand square meters. GT China sold 3618 suites with the average sales price of 22,031 Yuan/square meter. In 2014, the total sales area of Group was 3.91 million square meters and the contract sales volume was 79.4 billion Yuan. GT had accomplished the annual sales target of 127% set at the beginning of the year. The accumulated sales volume of four quarters was 39.5 billion Yuan which accounted for 49.7% of annual sales volume. Thus the strong sales of four quarters played a vital role in reaching the sales target.

Selling of Shanghai asset has uncertainty

Sunac bids 15.5 billion Yuan for Shanghai Sunac GT Holding, including the equity book value of 11.3 billion Yuan and outstanding debt of 4.2 billion Yuan, corresponding to 12.1 times 2015 P/E ratio and 2.2 times PB. And compared with NAV, it has a 18% discount. To be frank, this is an offer with the valuation being not low at all, which reflects that Sunac intends to obtain the leading position of Yangtze River Delta Region steadily by getting the company. On the other hand, although there is the support of Wharf Holdings and China Communications Construction Group, Song Weiping would not easily sell its assets of the best quality. Therefore, we estimate that it will be difficult for both parties to solve the issue of bidding for Shanghai Sunac GT Holding in a short term. The selling of assets has a rather high uncertainty.

Balance sheet will be rebuilt

The debt crisis of Kaisa has negative influences on real estate stock in Hong Kong and also leads to the fluctuation of bond price listed overseas. The total amount of the three bonds issued by Green City China (Two are of the dollar bonds and one is of RMB bond) is up to 10.8 billion HKD, with the due dates during the period of 2016-2019. Currently, the yield to maturity (YTM) is 8.6%-9.0%, and the current market prices are 97-99. The recent Kaisa event also caused the fluctuation of the three bonds of Green City. Recently, with the relief of the market panic mood, the bonds price also rose significantly. We think that the domestic real estate stocks will face three kinds of stress - the refinement of the industry prosperity, the real estate debt and political factors. The private real estate companies with the higher debt ratio should make consolidation of the balance sheet in advance.

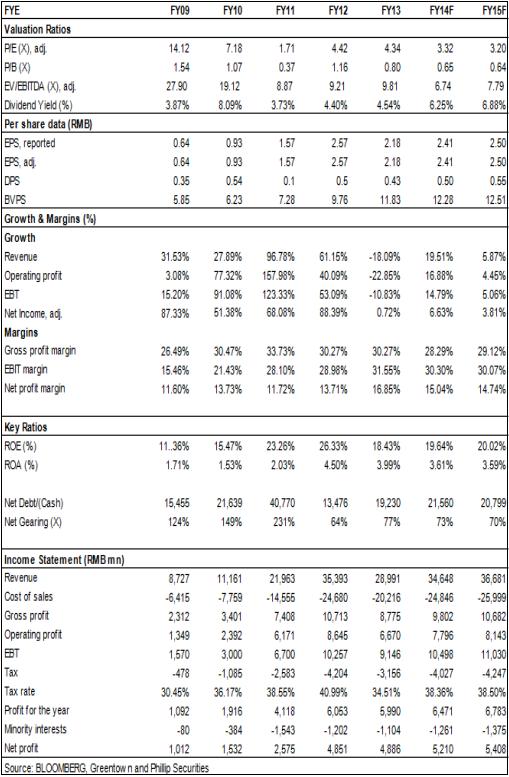

We expect that at the end of 2014, the net debt of GT China will exceed 30 billion, and the net debt ratio could be about 85%. The cashability of the property assets in the future and the company's refinancing ability are related to the important measures for GT to stabilize the balance sheet. As the two largest shareholders of GT China, Kowloon Club and CCCG Ltd. will make use of the strong capital strength and the financing ability to promote the reconstruction of Green City's balance sheet.

Valuation

No matter who is the winner, both Green City's equity dispute and the rivalry with Shanghai Sunac GT Holding had the negative influences on GT China, and also did harm to the valuation of the company. In the future, GT China will face many challenges, including the sales, financing and competition pattern. But what can be sure of is that GT China will remain the major role in Chinese real estate, and the joint power of Kowloon Club and CCCG Ltd. will drive GT China to complete the integration of strategy and product, and to form the new competitive advantage. The current price is attractive, and some catalysts including good news from selling and rebuilding will boost the share price upwards. We give GT China "Buy" rating, with the target price of 10 HKD in the next 12 months, which is equivalent to 3.2 times the forward P/E of 2015.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()