-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

CAERI (601965.CH) - China's Leading Auto R&D Evaluation Service Provider

Tuesday, June 2, 2015  10736

10736

CAERI(601965)

| Recommendation | Accumulate |

| Price on Recommendation Date | $15.100 |

| Target Price | $16.970 |

Weekly Special - 2333 Great Wall Motor

China's Leading Auto R&D Evaluation Service Provider

China Automotive Engineering Research Institute Co., Ltd (CAERI) is the only company listed in Stock A market which specializes in auto technology services and its controlling shareholder is China General Technology (Group) Holding Co., Ltd under the auspices of SASAC (Stated-owned Assets Supervision and Administration Commission). The broad range of services that CAERI provides fall into two categories: auto technology services and industrialized manufacturing business. Having strong capability in automotive R&D and testing, the Company is one of six third-party testing agencies licensed by the authority.

Automotive technology services are expected to experience rapid growth

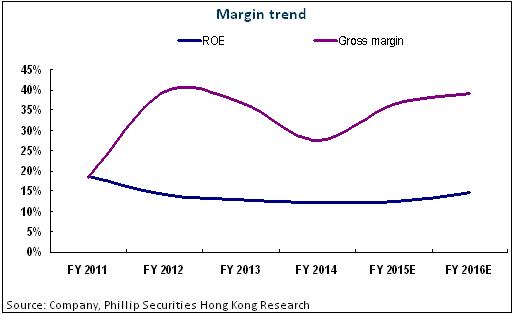

CAERI has outstanding profitability in automotive technology services. Although the business was adversely affected last year due to the rectification of oil-consuming measurement and other industry-specific factors, the Company's automotive technology services are regaining the momentum of rapid growth as the rectification was done, the domestic conversion of emission criteria was finished and the new base NVH/EMC project was launched. As the automotive technology services sits in the front part of the industry chain and is of a high-barrier sector, the access barrier in technology and policy ensures that the Company has strong pricing power. China's automotive market has entered a stage where growth is slowing but competition become more and more intense and this will undoubtedly stimulate the need for R&D. Meanwhile, the ongoing improvement and update in China's automotive industry-specific laws and regulations drives the demands for automotive evaluation. It is forecast that the high value-added services are likely to benefit from the fast growing automotive technology service sector in China.

Manufacturing business will benefit from commercialization of scientific achievements

The Company's industrialized manufacturing business includes Special Purpose Vehicles (SPVs), key components of railway transit and automotive fuel gas system. Among them, the key components of railway transit recorded a gross margin of over 50%, next only to that of the automotive technology services, and in 2014, this business landed new contracts amounting to RMB 225 million and is expected to have limited growth in 2015. Considering that the Company masters the key technologies, the commercialization of its scientific achievements makes the business look promising. In addition, Natural Gas Vehicles (NGVs) as a good example of clean energy application has huge room for further improvement as the domestic emission criteria keeps upgrading and the natural gas infrastructures are more widespread. Currently, Dinghui Automotive Fuel Gas, a subsidiary of CAERI, takes 85% of the refitted CNG vehicles market share together with two other competitors, and will benefit most from the industry growth. SPVs, however, doesn`t contribute much to the results because it has a very low profitability, more often than not one digit gross margin, and they are easily affected by the changes in macroeconomic situation.

Investment Thesis

Considering the Company's higher profitability in automotive technology services and its huge potential in the future, as well as the stock bottoms out, the operation of its new capacity is likely to bring about the turning point of the operation results. According to our forecast, its EPS in 2015 and 2016 will be RMB 0.48 and RMB 0.65 respectively, and our target price of RMB 16.97 yuan, respectively 35/26x of our expected EPS. We give it an "Accumulating" initiation rating. (Closing price as at 29 May 2015)

Company Profile- China's Leading Automotive R&D Evaluation Service Provider

China Automotive Engineering Research Institute Co., Ltd (CAERI), founded in 1965 and formerly known as Chongqing Heavy Duty Truck Research Institute, is one of Class One scientific research institutions. Its controlling shareholder is China General Technology (Group) Holding Co., Ltd under the auspices of SASAC (Stated-owned Assets Supervision and Administration Commission). CAERI is the only company listed in Stock A market which specializes in automotive technology services.

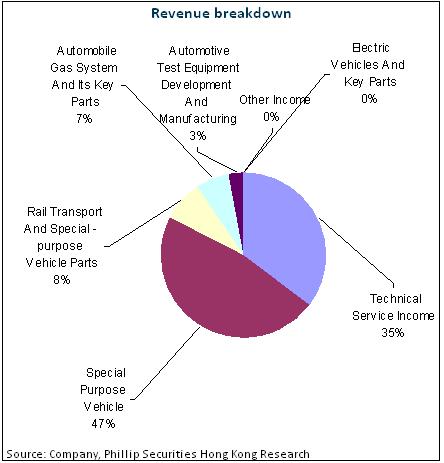

The broad range of services that CAERI provides fall into two categories: automotive technology services and industrialized manufacturing. The automotive technology services include automotive R&D and consulting, automotive testing and evaluation. The Company's industrialized manufacture business covers Special Purpose Vehicles (SPVs), key components of railway transit, automotive fuel gas system and its key components manufacturing.

Dozens of years` development has enabled the Company to have strong automotive R&D testing capacity, becoming an important base of Natural Gas Vehicles (NGVs) and key components of railway transit. The Company has three state-level technology R&D platforms: National Natural Gas Vehicles Engineering Technology Research Center, National Key Laboratory on Automotive Noise Vibration and Safety Technology and United Engineering Laboratory on Alternative Fuel Vehicles. In addition, the Company also has National Motor Vehicles Quality Inspection Center (Chongqing) and a post-doctoral research station, qualifying for “National High-tech Enterprise”, “Innovation-oriented Enterprise” and “International Cooperation Base”.

Automotive Technology Services are expected to gain rapid growth

For R&D and consulting services, the Company provides China's major automakers and components vendors with product development, technology consultancy, performance upgrading and other services, as well as vehicle-related new technology research and application entrusted by the relevant government authorities. In terms of automotive testing and evaluation, the Company mainly helps the automakers and components vendors with product performance testing, mandatory inspection and certification, and enjoys great strength in this aspect. Having strong capability in automotive R&D and inspection, the Company is one of six third-party testing agencies licensed by the authority.

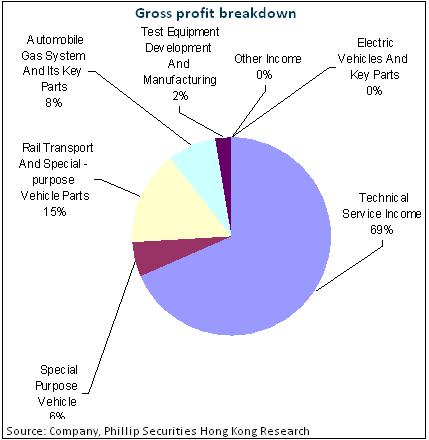

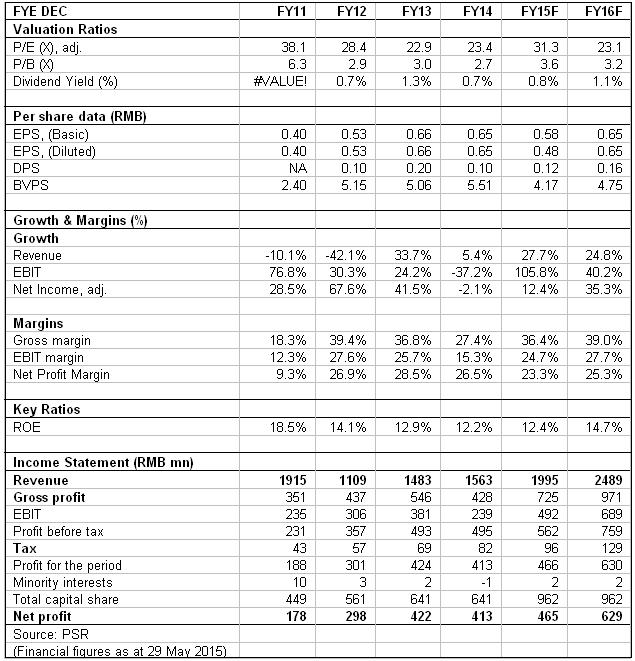

In 2014, CAERI registered revenues of RMB547 million from the technology services, representing 35% of the Company's total revenues, while the technology services contributed nearly 70% of the overall gross profit, with gross margin being up to 54% and showing strong profitability. Although the services were adversely affected last year due to the rectification of oil-consuming measurement and other industry-specific factors, the Company's automotive technology services are regaining the momentum of rapid growth as the rectification was done, the domestic conversion of emission criteria was finished and the new base NVH/EMC project was launched. For this business, Q1 2015 witnessed an increase of the gross profit by 11.4% yoy and 21.7% qoq.

We believe that, as the automotive technology services sit in the front part of the industry chain and is of a high-barrier sector, the access barriers in technology and policy ensure that the Company has strong pricing power. China's automotive market has entered a stage where growth is slowing but competition becomes more and more intense due to the rise of per capita rate of automotive ownership and the fall of automotive demands. To increase their product appeal to potential users, automakers must increase their R&D investment. Meanwhile, the ongoing improvement and update in automotive industry-specific laws and regulations in China drive the demands for automotive evaluation. It is forecast that the high value-added services are likely to benefit from the fast growing sector of the automotive technology services in China.

Components for railway transit look promising because of core technology

The Company manufactures components for railway transit, including monorail reducers, monorail braking devices, low floor train reducers, transmission case and so on. Among its customers of railway transit equipment manufacturers is China CNR Changchun Railway Car Co., Ltd. In particular, the Company made a technological breakthrough in the key monorail components which were qualified to replace the imported products and the gross margin from this business exceeded 50%, next only to that of the technology services in the Company. In 2014, the business contributed around 15% of the Company's gross profit despite the fall due to the changed schedule of order fulfillment. In the same year, this business landed new contracts amounting to RMB225 million and is expected to have limited growth in 2015. Considering that the Company masters the key technologies, the commercialization of its scientific achievements makes the business look promising.

Components for fuel gas system will benefit from alternative energy sources

The components for fuel gas system include electronic control system, pressure relief regulators, cylinder valves, nozzles and jet control system, with key customers from major automakers in China, such as Zhengzhou Yutong and King Long Motor. CAERI takes a leading position in Natural Gas Vehicles (NGVs) technology, having rich R&D experience and broad customer base. In 2014, the reported revenues of this business went up by 39% yoy, contributing 6.5% of the Company's total revenues and 8% of its total gross profit with gross margin at 34%. NGVs as a good example of clean energy application have huge room for further improvement as the domestic emission criteria keeps upgrading and the natural gas infrastructures are more widespread. Dinghui Automotive Fuel Gas, a subsidiary of CAERI, takes 85% of the refitted CNG vehicle market share together with two other competitors and will benefit most from the industry growth.

Special Purpose Vehicles face fierce competition

The Company's SPVs include vacuum trucks, agitator trucks, garbage trucks, dump trucks and so on, which are widely used in transportation, geological and petroleum exploration, agriculture, forestry, livestock husbandry and fishery, public security, fire control and other economic sectors. SPVs, however, doesn`t contribute much to the results because it has a very low profitability, more often than not one digit gross margin, and they are easily affected by the changes in macroeconomic situation.

Valuation

Considering the Company's higher profitability in automotive technology services and its huge potential in the future, as well as the stock bottoms out, the operation of its new capacity is likely to bring about the turning point of the operation results. According to our forecast, its EPS in 2015 and 2016 will be RMB 0.48 and RMB 0.65 respectively, and our target price of RMB 16.97 yuan, respectively 35/26x of our expected EPS. We give it an "Accumulating" initiation rating.

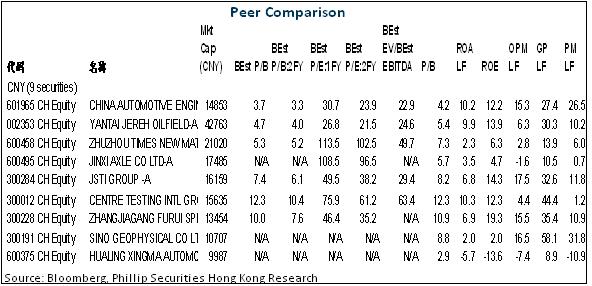

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()