-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Chongqing Rural Commercial Bank(3618.HK) - Profit performance met our expectation

Thursday, September 12, 2013  6803

6803

Chongqing Rural Commercial Bank(3618)

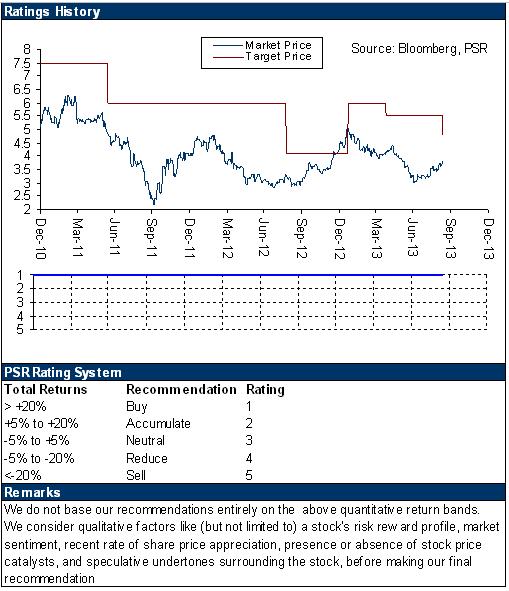

| Recommendation | Buy |

| Price on Recommendation Date | $3.800 |

| Target Price | $4.850 |

Weekly Special - 2333 Great Wall Motor

Company Introduction

CRCB has nearly 60 years of operational history that is one of the leading rural commercial banks in China. The bank experienced a series of financial restructuring since 2004. In June 2008, CRCB obtained the approval from CBRC, and has registered capital of RMB6 billion. In December 2010, CRCB was listed in H Shares.

Summary

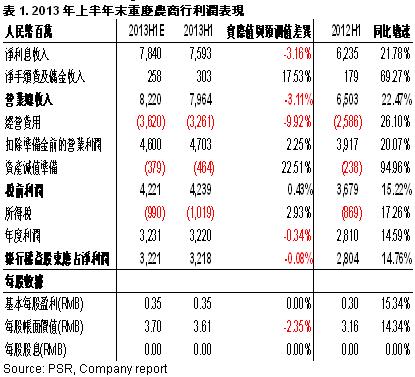

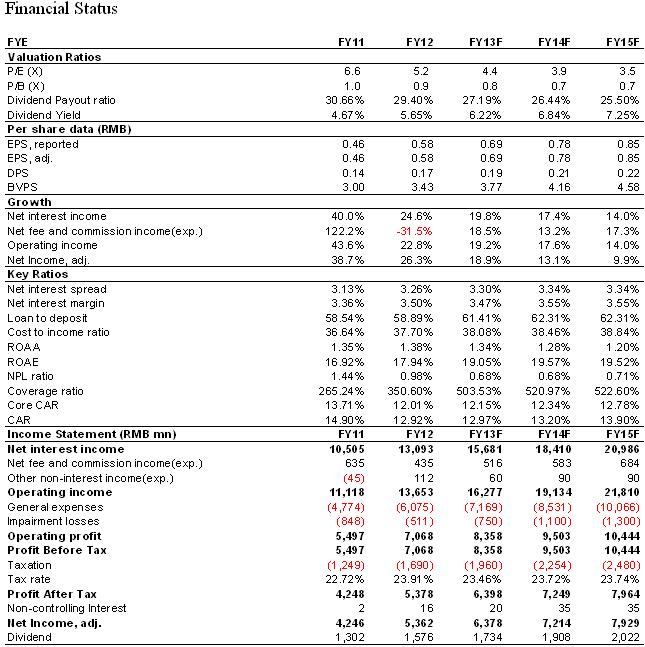

-According to 2013 interim report of CRCB(or the Group), as at the end of 2Q2013, net profits increased by 14.75% y-y to RMB3.217 billion with the slow-down of the growth rate, equivalent to the EPS of RMB0.35, in line with our expectation in Bloomberg;

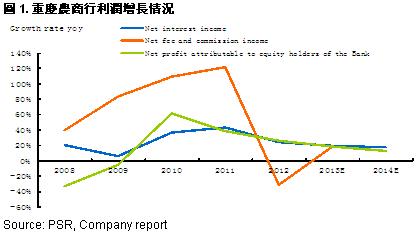

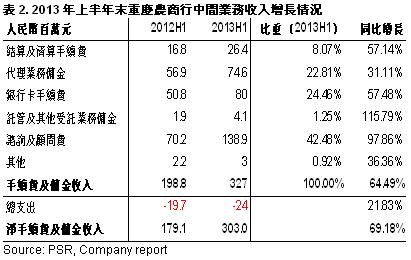

-The main reason of the stable growth of CRCB’s profits is the strong increase of the incomes from all businesses, especially for the intermediate business. By the end of 1H2013, the Group’s net fee and commission income increased sharply by 69.18% y-y to RMB303 million. The largest part of total incomes, net interest income, also increased by 21.78% y-y to RMB7.593 billion;

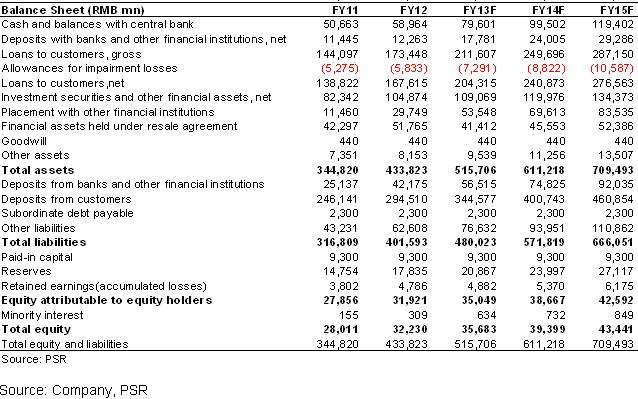

-The Group’s total assets maintained stable growth, raised 12.48% to RMB488 billion compared with the end of 2012, equivalent to the BVPS of RMB3.61, up 5.1%, the same as that of 1Q;

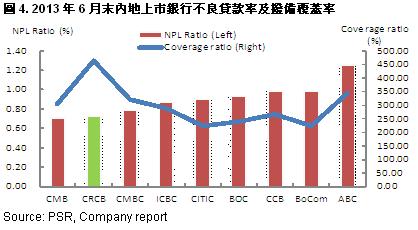

-Asset quality is still better than our expectation with the dual-decrease of the amount and ratio of NPLs, down RMB288 million and 0.25ppts to RMB1.407 billion and 0.73% respectively compared with the end of 2012, and the coverage ratio achieved to 456.93%, up significantly 112.80ppts during the same period. However, compared with 1Q, the decrease rate of the NPLs has narrowed, and we expect the amount will go up in future;

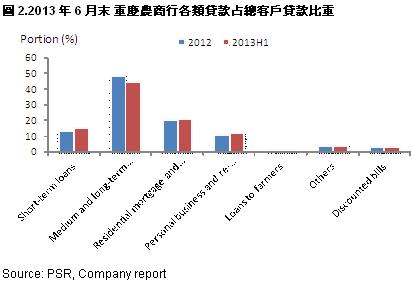

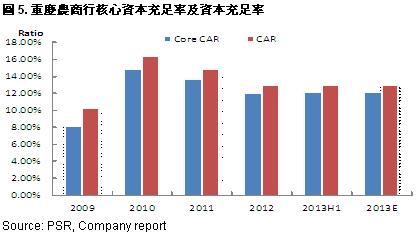

-Domestic banks started to use new rules to calculate the CAR in 2013, which caused the banks’ CAR to decrease obviously. By the end of 2Q2013, the Group’s Core Tier 1 ratio and CAR cut to 10.92% and 12.71% respectively, down 0.17ppts and 0.18ppts q-q. Even based on the previous calculation, the Core CAR and CAR increased by 0.07ppts and down 0.01ppts respectively, no big changes. Therefore the decrease of CAR led to the large increase of the bank’s capital pressure, which would affect the adjustment of capital expenditure projects, such as the amount of loans. In 1H2013, the Group’s net loans increased by 11% approximately, but obviously lower than the deposit growth as 15% during the same period;

-Overall the bank’s performance met our expectation, we still believe its profit growth would maintain on quite high level in 2013, but the profit growth would go down. We maintain the previous profit estimation that net profits would increase by 19% y-y approximately to RMB6.378 billion with the EPS of RMB0.69;

-Considering unstable factors in the markets currently, we cut the 12-M TP to HK$4.85, 28% higher than the latest closing price approximately, equivalent to 6.3xP/E and 1.2xP/B in 2014 respectively. Maintain Buy rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()