-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

GCL-Poly (3800.HK) - Valuation level will increase

Monday, May 5, 2014  3222

3222

GCL-Poly(3800)

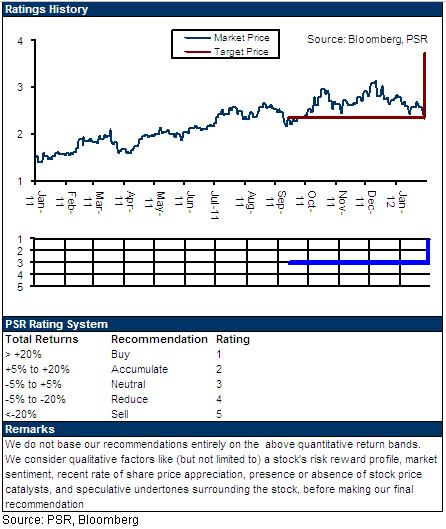

| Recommendation | Buy |

| Price on Recommendation Date | $2.370 |

| Target Price | $3.750 |

Weekly Special - 002050 Sanhua

Introduction of the company

As one of the largest global solar photovoltaic enterprises at present, GCL-Poly Energy Holdings Limited has become the largest photovoltaic material supplier in the world, and went public on the Hong Kong Stock Exchange in November of 2007.

Summary

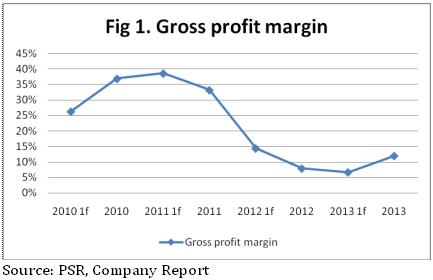

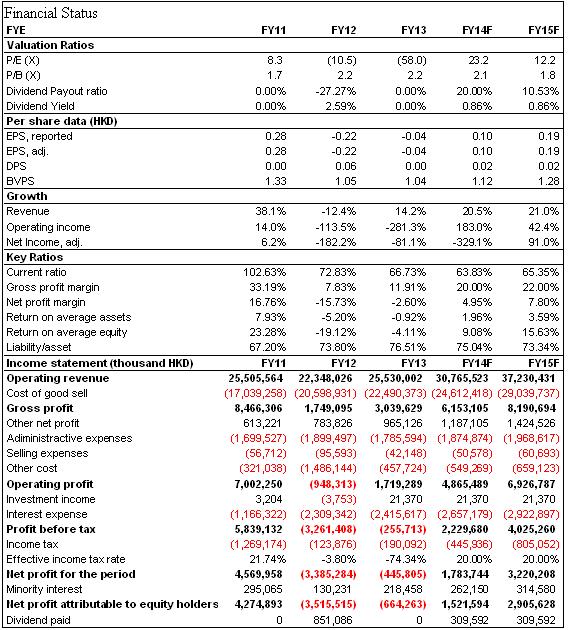

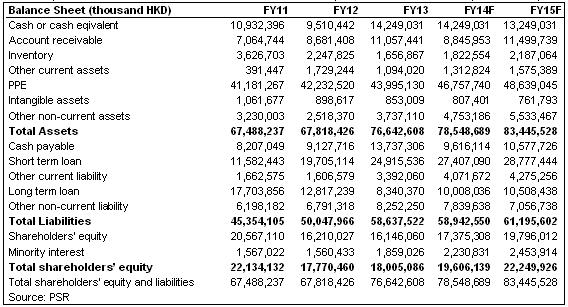

-The corporate performance in 2013 indicates that: the annual revenue is HKD25.53 billion, with an increase of 14.2%; the gross profit is HKD3.04 billion, with a huge increase of 73.8%; the loss attributed to shareholders is HKD0.664 billion, with a decrease of 81.1% compared with the HKD3.526 billion loss in the same period of 2012, and 4.29 cents loss per share.

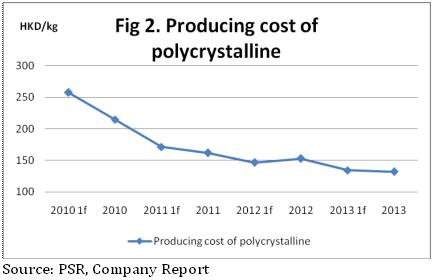

-The annual corporate production of polysilicon is 50,440 tons, with an increase of 36.1%; the amount of sales is 16,329 tons, with an increase of 29.7%. From the second half year of 2014, the corporation started to gradually put the silane fluidized bed technique whose capacity is 25,000 tons into production. Silane fluidized bed is the most advanced polysilicon production technique in the current world, by using which the cost of producing polysilicon can be further decreased. The expected annual sales of polysilicon this year will exceed 20,000 tons.

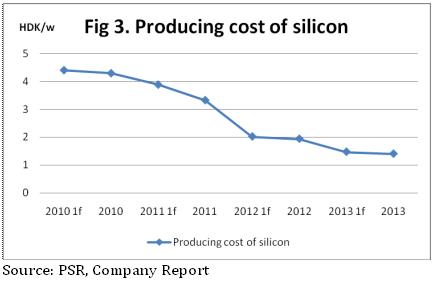

-The annual production amount of silicon wafers is 8,634 MW and the sales amount is 9,296 MW, which are increased by 53.6% and 66.2% respectively. The fact that the sales amount exceeded the production amount fully indicates hot sales of silicon wafer business. Therefore, the corporation will expand its capacity in 2014, from the current 10GW capacity to 15GW, to satisfy the sales condition of short supply. The expected sales amount of silicon wafers this year will exceed 11,000 MW.

-The corporation now owns 30 thermal power plants, wind farms and photovoltaic power plants in total. Equity capacity has reached 1,150 MW and provides profits of HKD6.71 billion, with an increase of 15.5%. The corporation achieved annual photovoltaic grid-connected amount of 270 MW in 2013, and has achieved 303 MW cumulatively up till now. The corporation will spend HKD1.4 billion to purchase 68% shares of Tyson Group, taking Tyson Group as its future distributed platform for PV business.

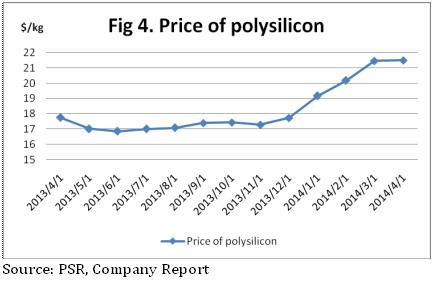

-After the revival of PV industry and frequent increase of polysilicon price, a lot of small enterprises which stopped production have recovered production, large-scale enterprises have expressed that they will increase the capacity in the future. The future PV industry will probably face the problem of excessive capacity again, and some polysilicon and solar products which just picked up may face the risk of price reduction again.

-Shanghai and Hong Kong Finance will enable mainland investors to have more convenient opportunities and invest in Hong Kong stocks. Domestic large-scale PV enterprises have been basically all listed in US or HK Stocks. The current industry position and stock price have made GCL-Poly worth to invest. It is believed that at that time a lot of mainland investors will choose GCL-Poly as the investment target for PV industry, and the valuation level of future corporation will probably increase consequently.

-After experiencing the trough of PV industry in last two years, the corporation global market share of polysilicon has increased to 24% from 15%; the silicon wafer market share has increased to 26% from 16%. The corporation started to make profits in the second half year of 2013. The application of new techniques in upperstream and the business development of electricity stations in downstream have made the cooperation prospect even better. After the implementation of Shanghai and Hong Kong Finance, the corporate valuation level will increase. Combining with the PV industry P/E ratio in A and H share market, we gave the corporate target price HKD3.75 within 12 months, which is 38/20 times of prospective P/E ratio in 2014/2015 respectively and it is "BUY" recommendation.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()