-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Salubris (002294.CH) - Growth Expected to Be Accelerated in 2017

Friday, February 10, 2017  26042

26042

Salubris

| Recommendation | BUY |

| Price on Recommendation Date | $29.040 |

| Target Price | $36.700 |

Weekly Special - 002050 Sanhua

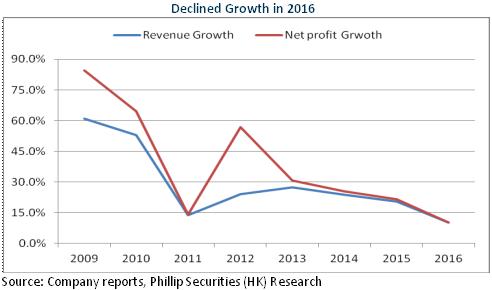

Growth Slowed Down in 2016

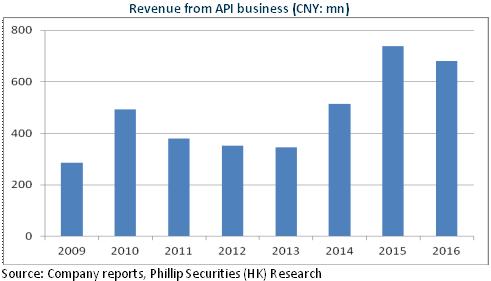

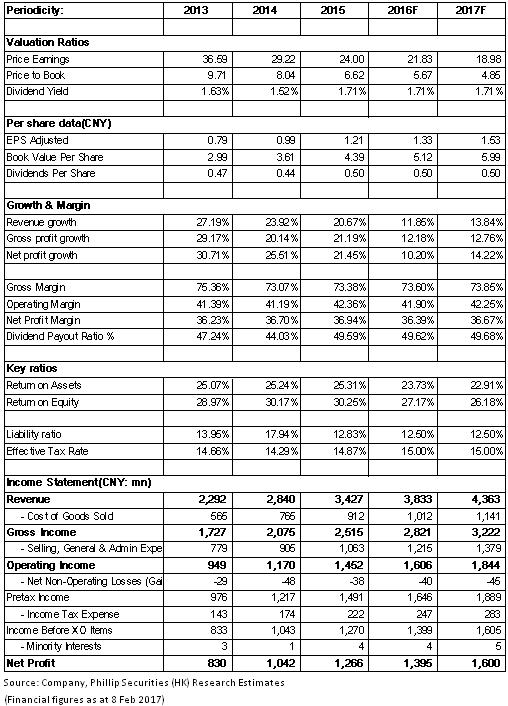

In 2016, Salubris recorded RMB3.83 billion in revenue, up 10.2% yoy; the net profit attributable to the parent company stood at RMB1.39 billion, up 10.2% yoy, with an EPS of RMB1.33. Overall speaking, the company experienced steady growth in 2016, but the growth rate slowed down, touching the lowest level since Salubris` IPO. As the main factor, the capacity was affected to a certain extent because the API business had been in the process of adjustment to production planning under the pressure from environmental protection. We expect that the API revenue in 2016 is less than RMB700 million, down to some extent compared to the previous year.

However, the company's preparations business is still expected to achieve rapid growth, with the sales volume of competitive products Clopidogrel (Taijia) rising by around 15% to approximately RMB2.6 billion, and the revenue from second-line products, such as Bivalirudin, achieving rapid y-o-y growth at RMB120 million to RMB150 million.

Growth Expected to Be Accelerated in 2017

First, the company is one of the few local enterprises which has successfully operated high-end generic varieties, and its core variety, Taijia, has obtained the EU certification and becomes a typical example of high-quality homegrown generic drugs. Due to too many potential competitors, the market generally was not optimistic about the prospects of Taijia. But after the introduction of the consistency evaluation policy on generic drugs, medical policies have valued "improvement of quality standards, emphasis on cost performance", which will benefit high-quality generics in approval process, bidding and purchasing and other processes. Therefore, we expect Taijia's oligopoly to maintain. Furthermore, Interim Measures for Drug Trade of Medical Institutions in Guangdong Province took effect in September 2016, which means Taijia may participate in the tender through the non-base drug list and return to the Guangdong market in 2017. Therefore, we anticipate that Taijia will report more rapid growth.

Second, the main second-line products are likely to enter the new Medical Insurance Drug Reimbursement List and sell quickly, which will mitigate the company's risk resulting from over-dependence on a single variety. Bivalirudin has become the preferred anti-coagulant drugs for PCI operations in the new version of guidelines, and its clinical status has exceeded heparin. Allisartan isoproxil, which belongs to New Drug Class 1.1, can be hydrolyzed into antihypertensive active substances in the gastrointestinal tract and absorbed without going through liver metabolism, thus imposing only small burden on liver and safer to the elderly. If Allisartan isoproxil makes the reimbursement list, its future revenue is likely to exceed RMB500 million.

In addition, the company accepted the assignment of 69.52% equity of Alain Medical for RMB129 million, for the improvement of its layout in cerebrovascular sector and peripheral vessel sector. The main products of Alain Medical are cerebral artery drug-eluting stent (in clinical follow-up stage) and lower limb arterial drug-eluting stent (in preclinical research stage), which possess optimistic market potential and is expected to become one of the growth points.

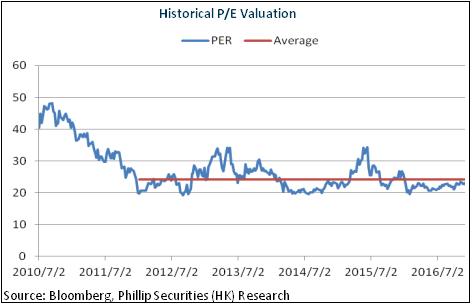

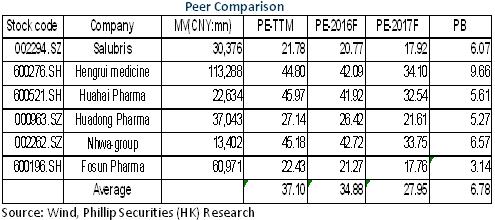

Valuation at Record Low

Generally, the company's growth hit the bottom in 2016, but will speed up in 2017 when the preparations business boosts. Meanwhile, the API business anticipates stable development. And the valuation of the company was only around 20x, at record low and the bottom of the industry counterparts. In light of the result improvement, we give an estimation of 24x EPS in 2017 with a target price of RMB36.70, with the "Buy" rating initially. (Closing price as at 8 Feb 2017)

Risks

Persistent risk of single product;

Expansion of second-line market below expectations;

R&D progress of new products below expectations.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

E-Check

Login

![]()

![]()

![]()

![]()