-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Construction Bank (939.HK) - The issuance of preferred stock reduced the capital pressure

Wednesday, December 17, 2014  17124

17124

China Construction Bank(939)

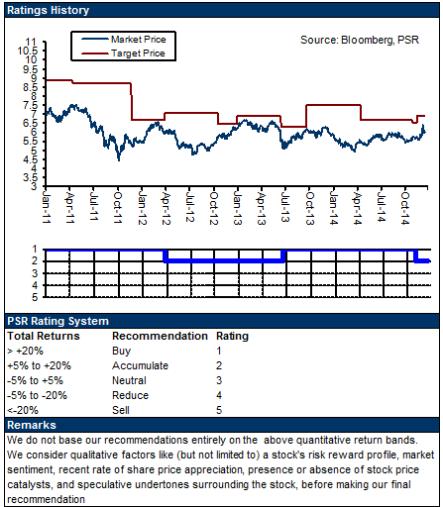

| Recommendation | Accumulate |

| Price on Recommendation Date | $5.980 |

| Target Price | $6.900 |

Weekly Special - 002050 Sanhua

Capital pressure declined

According to the latest announcement of China Construction Bank (CCB or the Group) last weekend, it will issue the preferred stock of 600 million shares privately, and the book value per share is RMB100, with the total amount of RMB60 billion, in order to increase its tier-1 capital.

The dividend of the preferred stock is paid annually, and according to the terms, if the core tier-1 CAR decreased to 5.125% (or below), CCB has the rights to convert the preferred stock into A Shares common stock without the agreement of the shareholders of the preferred stock.

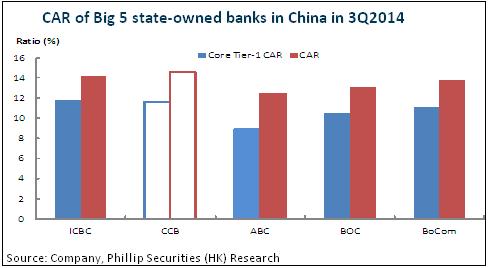

In the previous report, we mentioned that the bank’s capital pressure was smaller than other large-sized banks. By the end of this Sep, CCB’s CAR and Core Tier-1 CAR recorded to 14.53% and 11.65% respectively, up 0.90ppts and 1.19ppts respectively compared with the end of 2013. After the issuance of the preferred stock, excluding the relative expenses, CCB’s CAR and Core Tier-1 CAR would achieve to 15.12% and 11.65% respectively, representing the further decrease of the capital pressure.

Stable improvement of the performance

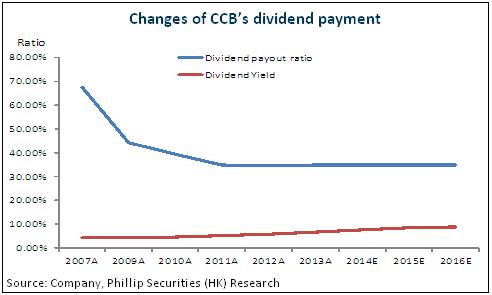

In all, the preferred stock will increase the bank’s capital obviously, the performance met our expectation in the first three quarters, and the market environment will improve obviously in 4Q, and the investors hold more optimistic view on the expectation especially after the launch of the HK-SH Stock Connect, therefore we still hold cautiously optimistic view on the bank’s future performance, but estimate the profit growth would go down continually and net profit should increase by 8% y-y in average in the next two years. We increase CCB’s 12-month target price to HK$6.90, 15% higher than the latest closing price, equivalent to P/E5.0x and P/B1.0x in 2015 respectively, and the valuation is quite attractive. Maintain Accumulate rating

Investment Thesis

The issuance of the preferred stock will increase CCB’s capital obviously this time, and based on the historical dividend payout record, the impact is quite small for the bank’s common stockholders. Considering the Group’s table performance, and the high CAR, we believe there is a further optimization of the bank’s capital structure, and the profit growth will maintain at the stable level.

CAR will increase

The CAR of CCB increased obviously in 2014 due to the internal capital accumulation from profit outpacing that of risk-weighted assets and the issuance of qualifying capital instruments. By the end of Sep, CAR and Core Tier-1 CAR recorded to 14.53% and 11.65%, up 0.90ppts and 1.19ppts respectively compared with the end of 2013, and CCB’s CAR was still on the top of the peers. According to the plan of the preferred stock, excluding the relative expenses, and based on the 3Q results, CCB’s CAR and Core Tier-1 CAR would achieve to 15.12% and 11.65% respectively, representing the further decrease of the capital pressure.

Small impact of profits

Common stockholders may have a loss of RMB3.6 billion based on the total amount of the preferred stock as RMB60 billion with the dividend yield of 6% because the preferred stockholders can gain the dividend primarily. However, considering CCB’s stable historical dividend payout record, we believe the impact of the preferred stock is quite small. Additionally, if all preferred stocks were converted into A Shares common stocks, based on the total amount of RMB60 billion and the convertible price of RMB5.20/share, the shares will be no more than 11.538 billion (=600/5.2), and as at the end of this Sep, CCB’s total common stock was 250,011 million, therefore original shareholders’ voting rights would be diluted no more than 4.41%.

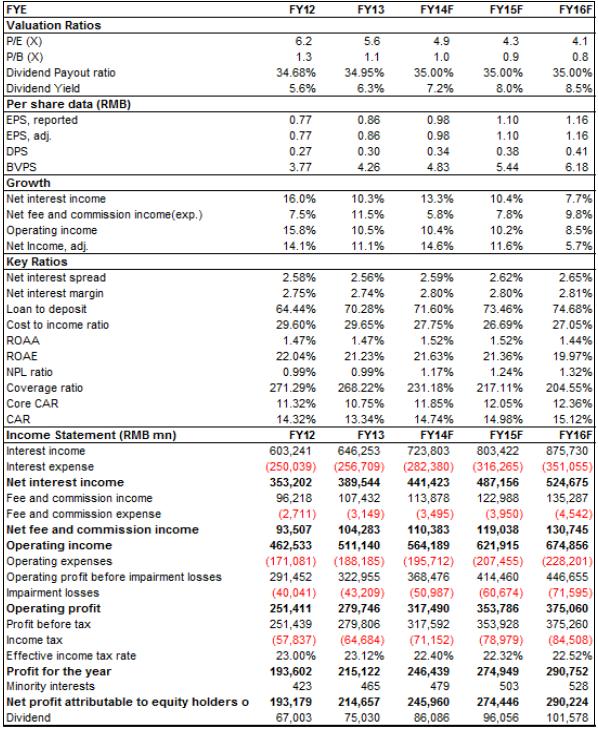

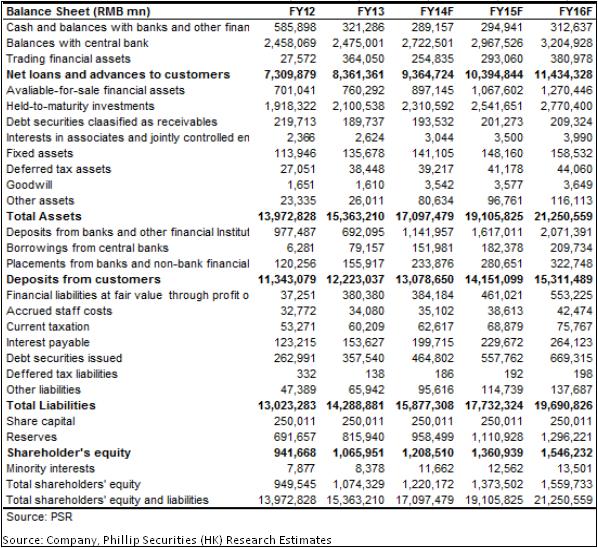

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()