-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of November 2013

Wednesday, December 4, 2013  5656

5656

Report Review of November 2013

Weekly Special - 2333 Great Wall Motor

Industry:

Local property and Others (Dennis), Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing),

Local Property (Dennis)

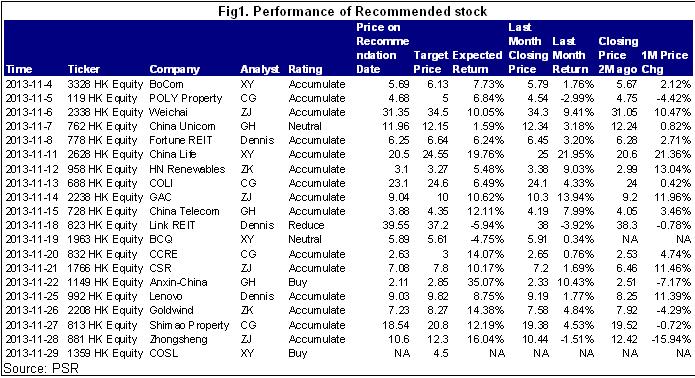

In November, we updated research report on Fortune REIT (778.HK) and Link REIT (823.HK).

Fortune REIT (778.HK): The acquisition of Kingswood Ginza property was approved in EGM on 16 Sept, 13 and completed on 9 Oct, 13. We like Fortune REIT's move to add growth driver and consequently create value for shareholders.U.S. Treasury yield surged from 1.63% to nearly 3% during the 4 months period starting from May, 13. In the same period, Fortune REIT's share price slumped 14.2% to HK$6.26. We observed that the 10-year U.S. treasury yield has calmed down to ~2.6% after Federal reserve announced the same bond purchase scale until more evidence to signal U.S. economy recovery. But it didn`t give a positive impact to Fortune REIT's share price. For October, Fortune REIT's share price declined 2% while MSCI US REIT index climbed 2.7% and Link REIT (823.HK) gained 2.8%. We believe Fortune REIT is undervalued. Our TP is HKD6.64, representing FY14 dividend yield of 6.0% (vs. historical average of 5.72%). We gave an “Accumulate” rating and the major downside risk is the faster-than-expected interest rate hike.

Link REIT (823.HK): 1HFY14 results beat expectation due to margin improvement. The net property income margin improved to 72.1%, up 1.5 ppt YoY/ 0.8 ppt HoH, mainly due to better cost control (utilities expenses dropped 4.4% YoY through energy management measures, repair and maintenance costs declined 3.9% YoY). We revised up DPU estimates for FY14 and FY15 by 2.4% and 1.1% on higher revenue growth and net property income margin. Our new DDM based target price was HK$37.20. Our target price implies forecast dividend yield of 4.4%, close to 5-year average of 4.44%, which we think more reasonable for investors amid the interest rate hike expectation. We gave a “Reduce” rating.

Mainland Financial (Xingyu Chen)

HSI showed the strong growth in November after the adjustment in October and it tried to touch the key point 24000 at the last trading day of this month. During the period, the large weighted sectors such as banking, and insurance appeared the better performance. Most of Chinese banks` prices increased slightly compared with the beginning of this month to varying degrees, this is mainly because the detailed policies have released in Shanghai FTZ after the Third Plenary Session, especially for some good news for financial sectors, which stimulated the market to make the good prospects for the future performance of banks and insurers. Additionally, there were two domestic banks listed in H Shares this month, plus one of the largest AMCs, China Cinda, promoted investment enthusiasm of the investors in domestic financial sectors.

As at the end of 29 November, 11 domestic listed banks increased by 3.4% approximately in average within one month, among which CMB's share price has the best performance with the growth of 7.3% in Nov, and considering two new listed banks, BOCQ recorded the worst one, decreased by 1.3% compared with its closing price at the first trading day. Overall, we still hold a cautiously optimistic view for the banks` future performance development, and maintain Buy rating to the sector.

Mainland Telecom (Fanguohe)

Overall speaking, the telecom sector has basically taken akin tendency to HSI since November. The early fall can be attributed to the failing expectation of 4G license issue in October. What's more, it was also suppressed by the weak market and the first fall of China Mobile's performance in 3Q13. Entering into the second half, the sector has risen with the market because of expected easing monetary environment by new Federal Reserve Chairman candidate and the reform expectation by the Third Plenary Session of 18th CPC Central Committee.

In our view, investors can become optimistic at the telecom sector after prior pullback. First, the capital expenditure of the three operators will accelerate in 4Q13, China Mobile and China Telecom have taken collective bidding and purchasing for 4G, which will help relative companies achieve better performance than the first half in 2013. Second, the award of 4G licenses will still be a positive catalyst for the sector.

According to Central Government, China National Security Council will be established after the Third Plenary Session of 18th CPC Central Committee, which will highlight the importance of national security and public security and verify the great attention paid by high-level leaders. We believe that the market of security and protection will be further supported by policies, and those security and protection enterprises with advanced technologies will benefit from this. So we recommend Anxin-China Holdings (1149.hk) and expect its performance can remain a compound growth rate of at least 30% in the next two years.

Mainland Property & Oil/Gas service (Chengeng)

In November, 2013 I wrote four research reports on Poly, COLI, CCRE and Shimao Property, which got success by unique operation model. We recommend “Shimao Property”. In 2014, the total sales scale of Shimao Property will be about 160bn RMB while the sales volume is expected to reach 60% of it. Thus we predict that it is really possible for the sales volume of 2014 to exceed 100bn RMB. The company has remained the compound growth rate of nearly 50% since 2012 to 2014, which is one of the highest among the mainland property stocks. We think that Shimao Property is in the best condition in terms of scale, increase and structure and it is currently a high-quality company within the industry. Therefore, we remain the valuation “Accumulate” for Shimao Property with 12m TP at 20.8 HKD, 5.6 times of expected price earning ratio in 2014.

Automobile & Air (ZhangJing)

The overall automotive sector in November performed well, among which, Dongfeng, GAC, Weichai and Sinotruk outperformed, others with the market trend. Airline stocks most of the time in sync with the market, but surged from late this month, outperforming the general trend. Particularly in our key recommendation in October of Cathay and Dongfeng showed strongest momentum.

In November, we updated 4 research reports including Weichai (2338.HK), GAC (2238.HK), CSR (1766.HK) and Zhongsheng (881.HK), in chronological order. We recommend CSR and GAC firstly. The former will benefit from the restart of the railway equipment sector and the latter is expected to accelerate the introduction of new models.

New energy & Environmental Goods

We published two reports in this month and recommended Huaneng Renewables (958.HK) and Xinjiang Goldwind (2208.HK). By main business, they can be classified as wind power operator and wind power equity producer respectively. The stocks of wind power industry have a rise in price in this month. The main reason is that there is more confidence about wind power industry getting warmer gradually in the market after the 3rd quarter performance reports were published. The wind power operators locate in the downstream of industry and expand the utilization quantity sharply; this causes the orders of equity producer increase.

The price of Huaneng Renewables increases about 10 percent and the valuation level reaches a relative high point simultaneously. We suggest hold in cautious if no favorable policy will be published in the future. Xinjiang Goldwind stays in the process of shock adjustment and the price is relative stable in this month, we forecast upside potential exist in this stock as the revenues of wind power equity producers are realized later compared with that of wind power operators.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()