-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Hysan Development (0014.HK) - Scenario analysis on cap rates change

Friday, September 27, 2013  9637

9637

Hysan Development(14)

| Recommendation | Accumulate |

| Price on Recommendation Date | $34.950 |

| Target Price | $39.000 |

Weekly Special - 3750 CATL

Company Profile

Hysan Development is principally engaged in property investment, management and development, which are mostly located in HK Causeway Bay. Investment properties include Hysan Place, Lee Theatre Plaza, Leighton Centre, Sunning Plaza, Lee Gardens, etc. In addition, the Group also holds high-end residential properties, Bamboo Grove in Mid-levels for rental purpose.

Investment rationale

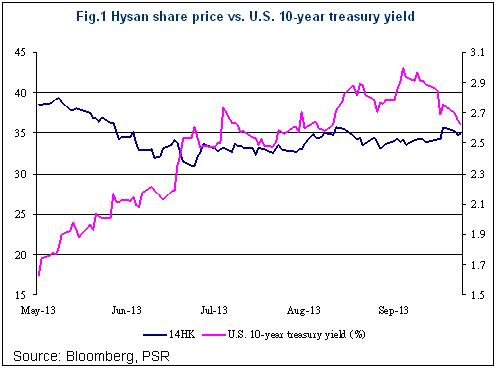

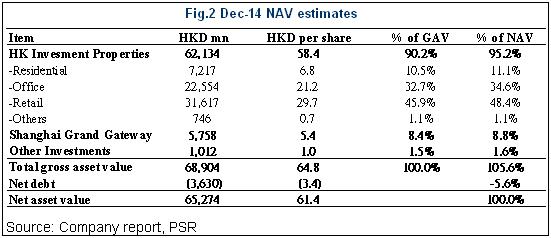

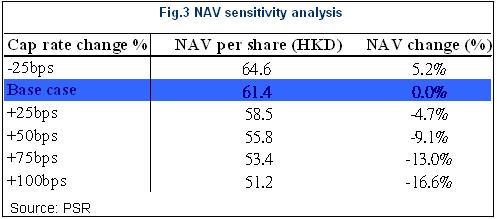

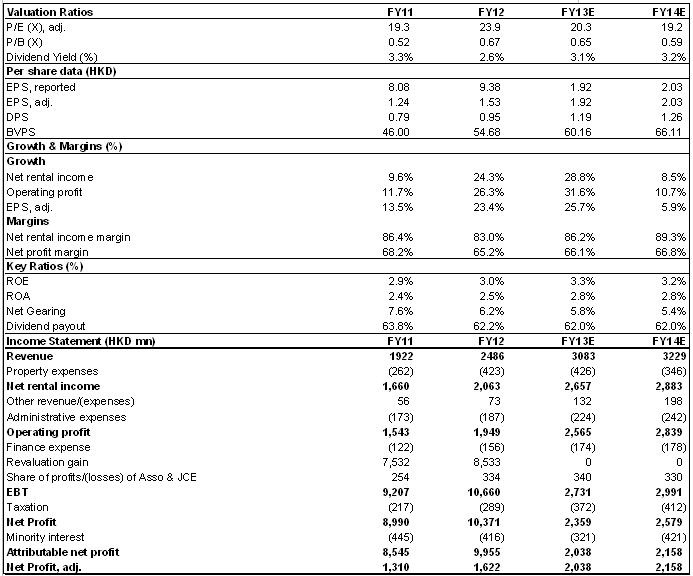

Scenario analysis on cap rates change – Hysan`s NAV is sensitive to cap rates change due to its pure landlord nature: We can see from fig. 1, Hysan`s share price slumped 19.7% to the lowest point on 25 June since 1 May (before our coverage) with the U.S. 10-year treasury yield surge, which climbed from 1.63% on 1 May to the highest point of nearly 3% on 5 Sep. The interest rate hike obviously triggered investor concern of cap rates expansion on the rental properties. We were aware of the concern of negative impact from higher cap rates assumption on HK property sector, especially on the landlords, we did a scenario analysis on cap rates change for Hysan. We found that our NAV estimate would drop 4.7%/9.1% for 25/50 bps added to cap rates and in the extreme case of 100 bps cap rates expansion, our NAV estimate would decline 16.6%. Not surprising that Hysan`s NAV is quite sensitive to the cap rates assumption, mainly due to its pure landlord nature (HK investment properties account for 95.2% of NAV, from our estimates). However, we would like to highlight that we have already given a conservative cap rates assumption, which is >5% for retail and ~4.8% for office portfolio. Moreover, U.S. 10-year treasury yield dropped to 2.64% yesterday after the outcome of the FOMC meeting that Fed will maintain the same pace of bond purchases. We believe it relieves investor concern of interest rate hike and give support to Hysan`s valuation.

Upside potential for Hysan`s valuation: Hysan showed strong growth in 1H13 net rental income, which was HKD1.35 bn, up 41.1% yoy due to decent rental reversion and contribution from Hysan Place. Our net rental income growth estimates for FY13 and FY14 are 28.8% and 8.5% respectively. The upside potential for our valuation will be better-than-expected rental growth, which drive Hysan`s NAV. It would happen if the rental reversion rate beat expectation while Hysan has ~15% by occupied GRA of retail space and ~27% of office space is up for renewal in FY14. Also, if Fed policy makers give a clearer plan of their monetary policy like reducing bond purchase schedule, investor concern of interest rate hike may be relieved and may drive the market sentiment on property sector and lift Hysan`s valuation (narrower NAV discount).

Downside potential for Hysan`s valuation: Hysan`s investment property portfolio is mainly located in Causeway Bay, a prime retail district in HK, so Hysan`s performance is highly reliable on tourist spending, especially from the mainlanders. 55.7% and 35% of Hysan`s net rental income came from retail and office sectors respectively in 1H13. Downside potential will be lower mainlander tourist spending and weaker HK economy, which gives negative impact on occupancy rate of office portfolio.

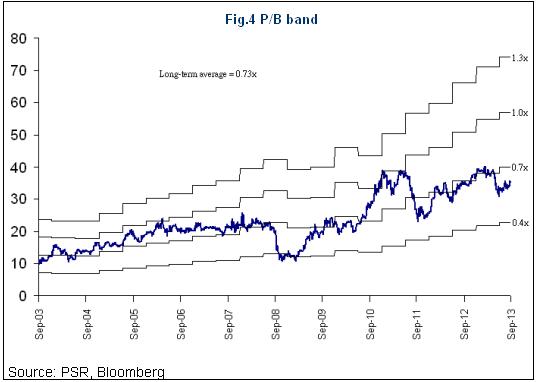

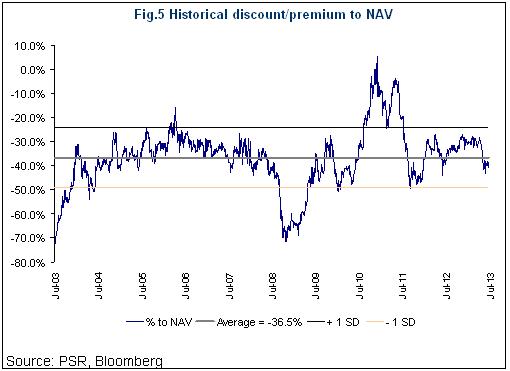

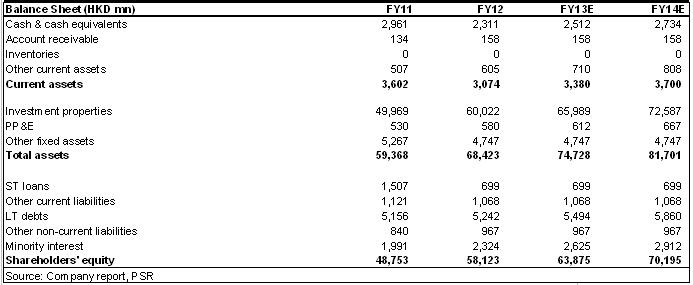

Valuation: We roll our NAV estimate to FY14, which is HK$61.4 per share, 5.7% lower than our previous FY13 estimate, due to a higher risk-free rate assumption. Hysan is now trading at P/B of 0.61 (vs. historical average of 0.73) or our 43.1% discount to our FY14 NAV estimate (vs. historical average of 36.5% discount). Hysan performed well in 1H13, Net rental income surged 41.1% yoy due to contribution of Hysan Place and robust organic growth, rental reversion of retail/office sectors reached 50%/40% in the period, occupancy rates were 99% and 93% for retail and office portfolio respectively. We don`t see a high downside risk on the rental income and occupancy rates of Hysan`s investment property portfolio, so current valuation is inexpensive in our view. We retain a same NAV discount target of 36.5% and get a TP of HK$39.00. We give an “Accumulate” rating to Hysan with upside potential of 11.6%.

Major risks

Earlier interest rate hike

Decline in HK retail sales or mainlanders` spending

Lower rental reversion

Lower occupancy rate

Financial Status

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()