-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ZTE Corporation (0763.HK) - 4G Business Contribution will Increase Significantly

Wednesday, April 23, 2014  2801

2801

ZTE Corporation(763)

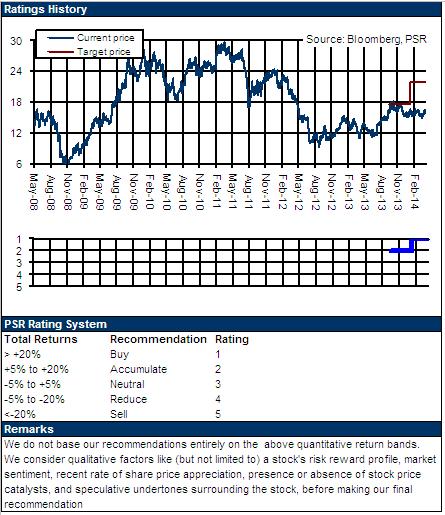

| Recommendation | Buy |

| Price on Recommendation Date | $16.580 |

| Target Price | $20.250 |

Weekly Special - 3993 CMOC Group Limited

Company Overview

ZTE is the world-leading provider of telecom solutions, providing technical and product solutions for telecom operators and intranet users in 160 countries and regions. Its main products include carriers` network, terminals, telecommunication software systems and service, etc.

Investment Overview

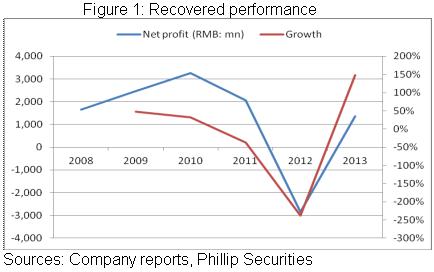

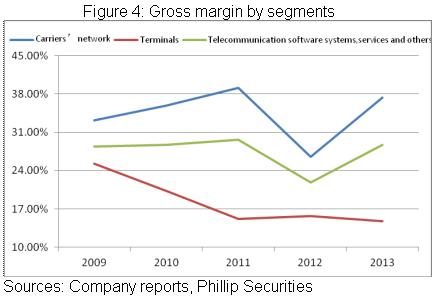

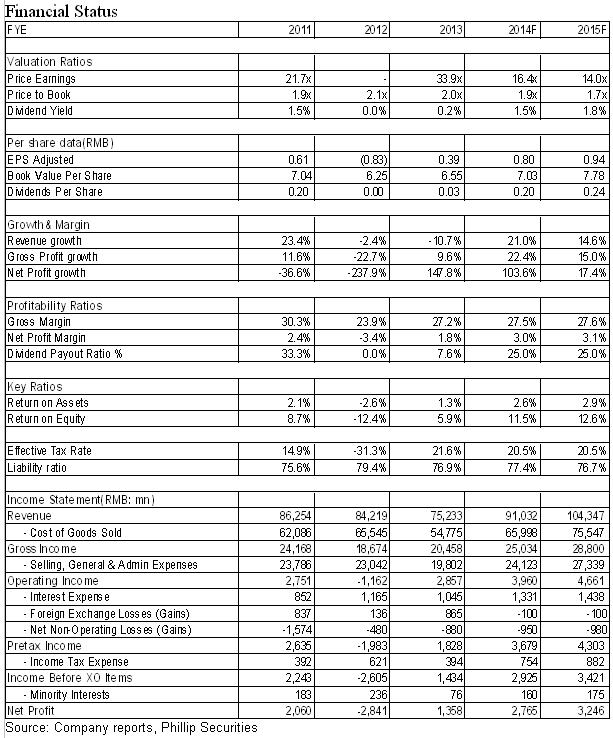

Due to the periodic trough of investments in domestic communication equipment and quarterly decreased overseas telecommunication operators` investments caused by the global economic downturn, ZTE has experienced decline in performance of two years. However, the financial report of 2013 published recently indicates that though the revenue drops 10.6% yoy to 75.2 billion RMB, the net profit rises 148% and reaches 1.36 billion RMB, converting into earnings per share of 0.39 RMB, which means that the company's performance shows signs of recovery. This mainly profits from 5 percentage points increase of gross profit margin which is 27.2% now. And among that, the gross profit margin of carriers` network business substantially rises over 10 percentage points to 37.4%.

The company's performance in 1Q14 continued to recover. Its revenue reach 19.053 billion RMB with a growth of 5.51%, and net profit attributable to shareholders reach 622 million RMB, with the growth of 203.51%. This mainly benefits from the confirmation of incomes of 4G primary devices with high earning capability, the development of overseas business and the decrease of financial costs due to the depreciation of the RMB. In addition, the company also forecasts that the performance in the first half year of 2014 will increase by 158% to 223% to 0.8 to 1 billion RMB.

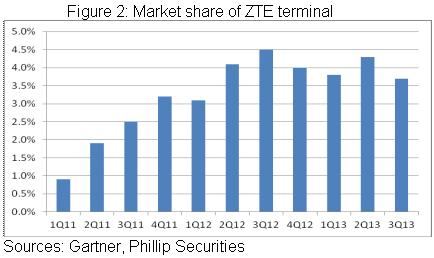

After the preliminary construction of 4G network is completed and covers large and medium-sized cities in Mainland China, smart cellphones may experience changing phones trend. In the first quarter, 4G cellphones only accounted for 4.1% among all cellphones of domestic brands, which was far lower than that of international brands, namely 20.6%. However, domestic 4G cellphones will be released in succession starting from the second quarter. And domestic 4G smart cellphones of one thousand RMB will have great impact on international brands relying on their high cost-effective performance. Therefore, the prospect of smart cellphone industry in the mainland is still optimistic. With the technological advantages of ZTE, the realization of the company's terminal goal, namely increasing the shipment of smart cellphones from 40 million in 2013 to 60 million and realizing the growth of income of smart cellphones for 20% on year-on-year basis, is a large probability event after the product line and distribution channels finish recombination.

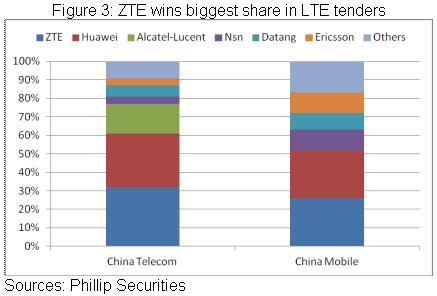

As the core supplier of primary devices, ZTE is expected to obviously benefit from the arrival of 4G investment period. The capital expenditure of China Mobile in 2014 is 225 billion RMB with a year-on-year growth of 22%. China Unicom and China Telecom also are probable to have additional investment in wireless business after obtaining the 4G business licenses of FDD-LTE. It is also worth mentioning that the carriers` network business is highly profitable, and the increase of its contribution in 2014 also means that the gross profit margin of the company is probable to keep rising in succession.

After the "Prism" event, departments of domestic governments and enterprises gradually show the trend of de-Cisco, which is a good opportunity of development for ZTE, Huawei, Ruijie and other domestic manufacturers with the addition of the government's construction planning of safe and intelligent cities. After ZTE increases the resource investment, it is expected that this business is probable to become the third growth pole following primary device and terminal in the middle period, and its revenue proportion is probable to rise to twenty or thirty percent from the current ten percent.

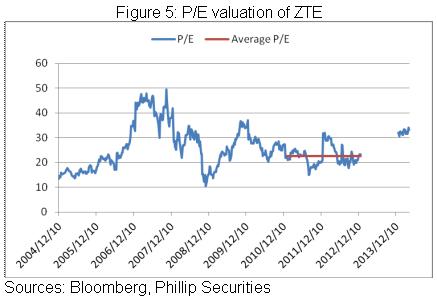

Viewing from the historical valuation, the company's valuation once reached 37 times during the peak period of 3G capital expenditures in 2009, and the average PE ratio also has reached 22 to 23 times in the downturn period since 2011. Even we assume that the PE ratio valuation is 20 times that of EPS in 2014, the target price can reach 20.25 HKD , which is "Buy" rating.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()