-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of June 2014

Wednesday, July 2, 2014  7697

7697

Report Review of June 2014

Weekly Special - 002050 Sanhua

Industry:

Software (Kay Ng), Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe), Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing), New energy & Environmental Goods (Zhang Kun)

Software (Kay Ng)

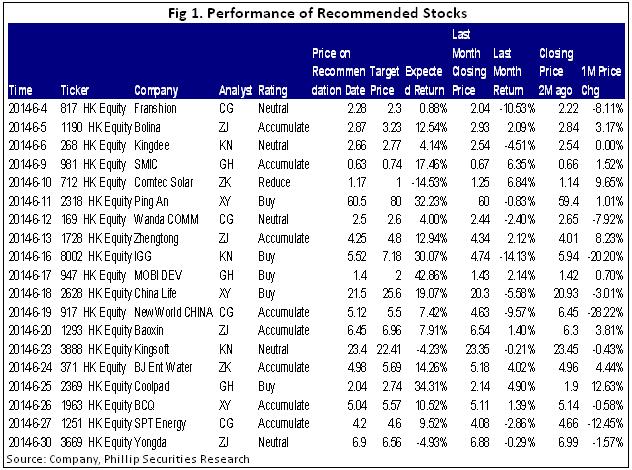

The price movement on mobile gaming and software stocks in June had similar patterns as May.

Mobile gaming stocks continued to sink. There is rumor that Ministry of Culture will take measures to monitor the mobile gaming market, in order to prevent illegal Internet activities, or excessive pornography and violent content in the mobile apps. Although Boyaa had repurchased its shares from market last week, the half-year closing price was still as same as the 2014 opening, though it was already the best performing stock among the mobile gaming sector. Forgame had reached its record low last week and the acquisition of Magic Feature Inc was still in a doubt, while IGG had continued to slide on the downward channel. Suffered from weak IPO condition, the newly listed chess game operators Ourgame dropped nearly 12% on its first listing day. It is expected the mobile gaming sector is still in consolidation in the short term, while share prices are expected to rebound based on good performance in the second quarter.

The overall performance of software sector was slightly better than the mobile gaming. The Chinese government was concerning to establish the Internet security examination scheme for online information security. There was news on the trial localization of information security, which would focus on the using of domestic server and router. Among all, Sinosoft performed the best with 6.4% increase in June, while other software stocks such as Kingsoft and NetDragon recorded around low single digit price growth. However, a newly listed software stock Chanjet Info that focused on small and micro enterprises ERP software had recorded an 8% drop in price in its first listing day. Share price had dropped cumulatively about 15% for the till the end of June. However, last week the China International Software & Information Service Fair last week had just released the China Enterprise Information and Software Requirements Report", which expected the investment in information security by enterprises would increase by more than 30%, and corporate and government procurement of software would increase 7.8 %. Therefore, we still expect the software sector can be benefited more from national policies and market demand, thus have more stable performance in the long run.

Mainland Financial (Xingyu Chen)

The market continued to maintain stable in June, HSI adjusted slightly around 23,200. Most of Chinese banks’ prices increased this month. The operating performance of banks also maintained stable growth, with the positive market prospect, which is one of main reasons of large growth of banks’ share prices in June. The regulators announced a series of policies to support the banks’ development, such as the issuance of the preferred stock, BOC and ABC have announced their plans, and we believe ICBC and CCB will make the plans as well in future. Additionally, the PBOC announced the list of banks approved to decrease the directional deposit reserve rate by 0.5ppts, which can make the banks release more capital in the market, and increase the market liquidity. We expect the released capital would achieve to RMB100 billion. Meanwhile, the main target of decreasing the deposit reserve rate this time is to support the real economy, especially for agriculture, rural areas and farmers, and SMMEs, and decrease financial costs for these industries or enterprises.

According to the share price, the small and medium-sized commercial banks recorded the better performance, among which Harbin Bank achieved the best performance with the share price growth of 17.5% this month, and CMB and CMBC recorded the relative better performance among the peers, with the price growth of 7% and 7.5% respectively compared with the end of last month. Overall, we still maintain Accumulate rating to the banking sector.

Mainland Telecom (Fanguohe)

China Mobile has won 4G TD-LTE license since the end of 2013. On June 27, 2014, the MIIT authorized China Telecom and China Unicom to take the trial of FDD / TD hybrid network in 16 cities respectively. In May, the 4G user net increase has doubled in mainland. In our view, 4G charge has decreased since June, plus with more available 4G terminals and lower sales prices, the 4G market in mainland has been into the fast lane.

After experiencing the call-back, the telecom sector has seen the recovery trend. We believe the 4G network construction will still be in a rapid development period, and the 4G handsets shipment may begin a robust outbreak, so we recommend ZTE, Mobi Development, Tongda Group and Coolpad Group. For the worry that the operators may cut terminal subsidies, we expect that, this has limited impact, because the adjustment of subsidy policy is structure based, that is to say, they are planning to increase the subsidies for 4G mobile phones while gradually eliminate the subsidies for 2G/3G mobile phones. Furthermore, subsidies in the past were mostly shared by high-end cellphones like Apple. Judging from these two aspects, we think the subsidies cut may benefit mainland terminal manufacturers like Coolpad Group.

Mainland Property & Oil/Gas service (Chengeng)

In June, 2014 I wrote three research reports on Samsonite, CSCI and Shimao Property, which got success by unique operation model. We recommend “CSCI”. We believe that, driven by the amount of adequate uncompleted contracts and robust new orders, the profit growth of CSCI in 2014 is expected to speed up. We expect that the profit growth of the company will respectively reach 50% in 2014 and 36% in 2015, and the compound average growth rate from 2011 to 2015 will reach 38%. With the deepened understanding by the market over the accelerated performance of CSCI and its features that distinguish it from common domestic-funded real estate stocks, the company's stock price is expected to recover after this round of adjustment. We give a “Buy” evaluation to CSCI, that the 12-month target price is 15.80 Hong Kong dollars, which equals to 17 times of price earnings ratio in 2014 and 15 times of price earnings ratio in 2015..

Automobile & Air (ZhangJing)

This month we released 4 reports: updated Zhengtong(1728.HK), Baoxin(1293.HK), and Yongda(3669.HK), and a field research report of Bolina (1190.HK), all of which show relatively better return with the HIS index. As far as the valuation ratio is concerned, we prefer Zhengtong with the more attractive expected P/E ratio.

The high-end strategy focusing on luxury cars adopted by the company has a positive influence on its high-return after-sale business, besides, the extension business focusing on the second-hand cars, automobile insurance and automobile finance still lies in the initial stage of development currently, with broad space in the future. The company forms a favourable layout in the aspects of automobile insurance, automobile network and mobile terminal, laying a foundation for the development of high-margin business in the future. Our 12-month target price of HK $ 4.8 is based on 8.5/6.8x P/E 2014/2015E EPS, Accumulate rating.

New energy & Environmental Goods (Zhang Kun)

Ministry of Environmental Protection presented “Standard for pollution control on the municipal solid waste incineration” in this month. It provided more restrict need to solid waste treatment and local government will choose the waste treatment facility with higher standard. In this area, all facilities of “China Everbright International (257.HK)” use the European 2000 standard, which is more restrict than national standard, so the company will more competitive in the future.

We update two reports in this month, they were “Comtec (712.HK)” and “BJ ENT Water (371.HK)”, BJ ENT Water has sharp increase in operation development and the international strategy is in progress, we are bullish on its future performance.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()