-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Geely (175.HK) - Electrification Upgrading Is Accelerating

Monday, April 25, 2022  1906

1906

Geely(175)

| Recommendation | BUY |

| Price on Recommendation Date | $11.800 |

| Target Price | $14.900 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

Sales Volume Underperforms the Industry Average for Multiple Reasons

According to the released sales data, Geely reported a sales volume of 146.4/78.5/101.2 thousand units in Jan/Feb/Mar, -6.36%/+1.63%/+1.14% yoy. In the first quarter of this year, the cumulative sales volume was 326024 units, down 2.26% yoy. Geely completed 19.8% of the annual target of 1,650 thousand units.

According to the information released by the CPCA, the sales volume of China's passenger cars fell by 4.4% yoy in January, and increased by 27% yoy in February, down by 1.6% yoy in March. The overall growth of the Geely's sales volume was below the industry average. We think that the main reasons are listed as follows: 1) The dilemma of chip shortage (such as body electronic stability system (ESP) chips) has not been got rid of. 2) The Chinese Spring Festival holiday in 2022 was earlier than the previous year. 3) With a small proportion of new energy models, the Company has not fully enjoyed the booming prosperity of new energy vehicles.

The Sales Volume Increase Mainly Depends on New Energy Products

On a closer look at brands, Geely brand's sales volume in Jan/Feb/Mar dropped by 6.1% /3.0%/flat yoy, respectively. In particular, the high-end models of China Star series (Xingrui, Xingyue, and Xingyue L) recorded a sales volume of 25/14/21.6 thousand units, respectively in Jan/Feb/Mar, accounting for 17.1%/17.8%/21.35% of the total sales, respectively. The proportion saw a further increase. The premiumization of Geely brand was steadily advancing.

In Jan/Feb/Mar, LYNK&CO brand reported a sales volume of 18/11/13.6 thousand units, respectively, down 28.1%/11.0%/17.2% yoy, respectively. We think that `LYNK&CO`, as the Company's high-end sub-brand, has a high level of intelligent configuration, which has led to a more serious shortage of required chips, and the lack of new energy models, are the main reasons for the poor performance.

`Geometry`, Geely's pure electric sub-brand, displayed remarkable performance. Its sales volume in Jan/Feb/Mar was 10.2/7.7/8.1 thousand units, respectively, up 391%/863%/334%, respectively. `Zeekr`, Geely's premium pure electric brand, delivered 3,530/2,916/1,795 units in Jan/Feb/Mar. Since its launch, 13.8 thousand units have been delivered accumulatively. `Ruilan`, the battery swap-enabled brand of Geely, sold 1,618/2,008 units in Feb/Mar, with a cumulative sales volume of 5,309 units this year.

On a closer look at markets, export markets maintained outstanding performance. In 22Q1, the export sales volume climbed to 27,417 units, up 15% yoy.On the whole, the Company's sales volume increase was mainly driven by the sales volume of new energy products. The proportion of the sales volume of new energy vehicles continued to expand, rising to 18.5% at one point in February, compared with 12.2% and 14.4% in January and March, respectively.

Affected by the increases Investment in Transformation and Upgrading strategy, 2021's Results Are and Decrease by over 10%

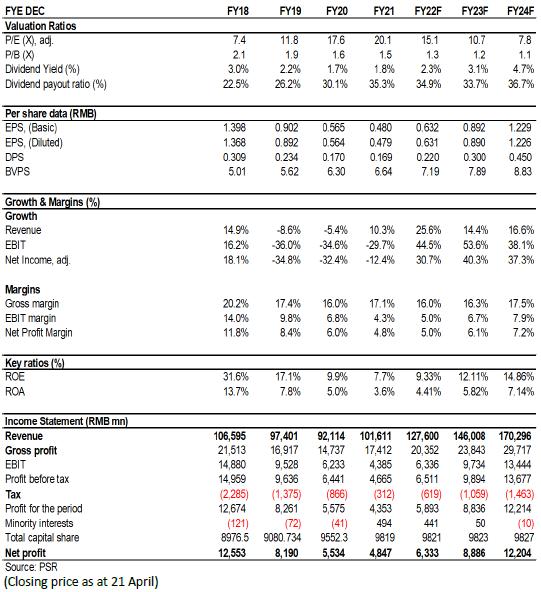

According to the latest released financial report, under the premise that the total sales volume increased by 1% yoy to 1,328 thousand units in 2021, the Company reported a gross revenue of RMB101.61 billion, up 10% yoy. Specifically, the automobile sales revenue increased by 5% yoy to RMB87.7 billion, which reflected the further optimization of the sales mix. Excluding LYNK&CO/Zeekr, the average sales price increased by 9% yoy to RMB87.7 thousand. The proportion of models with a guidance price between RMB100 - RMB150 thousand increased to 44% from 25% in the previous year. The proportion of above RMB150 thousand increased from 11% to 22%. In addition, the Company recorded a total of RMB4.53 billion in revenue from technical support services and intellectual property licensing, we believe whose contribution to the results is expected to continue in the future.

However, the revenue growth was offset due to the sharp increase in raw material costs, and the significant increase in expenses resulting from the increased R&D investment (up 120% yoy) and the recognition of large-value employee share incentive scheme (RMB1.2 billion). Therefore, the net profit attributed fell 12.4% yoy to RMB4.85 billion, lower than expected. While excluding the expenses paid by shares and RMB370 million of loss attributable to stockholders resulting from Zeekr, the net profit would increase by 16% yoy to RMB6.43 billion.

The annual gross margin grew by 1.1 ppts yoy to 17.1%. The ratios of S&A expense saw a yoy increase of 0.7 ppts and 1.7 ppts, respectively. The R&D expense ratio increased significantly by 2.6 ppts due to the increased R&D investment in the new brand Zeekr and the transformation and upgrading strategy in the Geely 4.0 era (including new powertrain, and electrification and intelligence of automobiles).

The capital expenditure in 2021 was RMB6.1 billion. The budget for 2022 is RMB9.2 billion. In order to maintain medium- and long-term competitiveness and attract talent, the Company is expected to maintain large R&D expenditure and share incentive.

Electrification Upgrading Is Accelerating

In October 2021, Geely released its hybrid power technology: Leishen Power. Leishen Hi-X, the Leishen intelligence engine, highly integrates one power generation motor, one drive motor, two motor controllers and 3-speed hybrid transmission, with the advantages of low fuel consumption, strong power, and long endurance. It reduces fuel consumption by 40%, and has a NEDC rating as low as 3.6L/100km, which is 0.4-0.6L lower than the Japanese HEV. In the future, it can match different models graded at A0-C, and adapt to full hybrid systems such as HEV, PHEV, and REEV. Relying on its CMA, BMA, SPA and SEA architecture platforms, Geely plans to launch more than 25 new smart new energy models in the next five years, including ten models of Geely brand, five models of Geometry, five models of LYNK&CO, and five models of new battery swap-enabled travel brand. New models equipped with Leishen Power launched in 2022 include LYNK&CO 01 HEV/PHEV, 03 HEV, 09 PHEV, 05 PHEV, Emgrand L HEV, and Xingyue L HEV/PHEV. We think that the launch of Leishen Power is significant for Geely, which not only makes up for the shortcomings in smart HEV, but also takes the first step of the "Smart Geely 2025" strategy, facilitating the realization of the objective of "Smart Travel Technology Enterprise".

Investment Thesis

Since 21Q4, the Company's share price has tumbled by 60%, mainly reflecting market concerns about the profit erosion of downstream manufacturing by rising raw material prices or subsidy declines. From Feb 2022, it has been dragged down by the potential impact of political conflicts. We think that Geely is relatively less affected by rising costs due to the model structure and excellent cost control. In 2021, the Company exported only 2% of vehicles to Russia, with limited risk exposure. Factors such as the chip shortage caused by the pandemic are expected to gradually improve or eliminate from 2022, and the long-term competitiveness and growth momentum remain unchanged.

We revised our financial forecast and target price to HK$14.9, equivalent to 19.1/13.5/9.8x P/E ratio in2022/2023/2024, and we give the rating of BUY. (Closing price as at 21 April)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()