-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

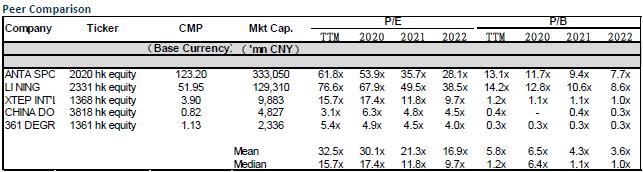

ANTA SPORTS (2020.HK) - Spin off sub-brands and focus on core business of the JV

Monday, January 4, 2021  8332

8332

ANTA SPORTS(2020)

| Recommendation | ACCUMULATE |

| Price on Recommendation Date | $123.200 |

| Target Price | $144.940 |

Weekly Special - 358 JIANGXI COPPER

Investment Summary

The joint venture company divested its sub-brands

The company announced on December 22 that the joint venture company Amer Sports Holding (Cayman) Limited (AS Holding) sold its brand Precor to Peloton Interactive, Inc. (PTON.US) for a total cash consideration of US$420 million (Approximately HKD 3.27 billion), corresponding to the P/E of FY18/19 is 40.0x/6.7x respectively. Precor's main business is the design, production and sales of fitness equipment.

The transaction is expected to be completed in 2021, after completion, Precor will be 100% owned by Peloton. As of October 31, 2020, the net asset value and intellectual property book value of Precor's business was approximately US$312 million. It is expected that after the completion of the transaction, it will generate approximately US$20 million in profits for the joint venture group. Based on a 52.70% shareholding ratio, the transaction is expected to contribute approximately RMB 69 million in net profit to Anta in 2021.

Sub-brands are not closely related to the company's core business

We believe that this disposal of sub-brands will help the joint venture to focus on its core business in the future. When acquiring Amer, Anta plans to focus on the development of footwear and apparel brands, while Precor's main business is less connected to Amer's core business. The divestiture of non-core assets also enables Amer to focus its resources on the three core brands (Arc`teryx, Solomon and Wilson) in the future. The proceeds from this transaction will help improve Amer's cash flow, build directly-operated stores for the three core brands, and develop footwear and apparel product lines. On the other hand, the average EBIT margin of the Precor brand for the past years is about 3%, which is lower than the loan interest rate of the joint venture and the overall EBIT margin of Amer Sports. The profitability of the joint venture is expected to increase after the disposal.

Double 11 shows the company's digital operation capabilities

During the Double 11 Shopping Festival, Anta Group's e-commerce GMV reached RMB 2.84 billion, a year-on-year increase of 53%. Among them, the GMV of its online flagship store on Tmall recorded a year-on-year increase of 93.36%. The company's e-commerce turnover this year also exceeded RMB 10 billion at 11November. The company's digital transformation is accelerated under the epidemic. During Double 11, the company's multi-brands reached 160 million consumers, of which new customers accounted for more than 83%, reflecting the ability of digitalizing new customer groups to operate.

Valuation and investment advice

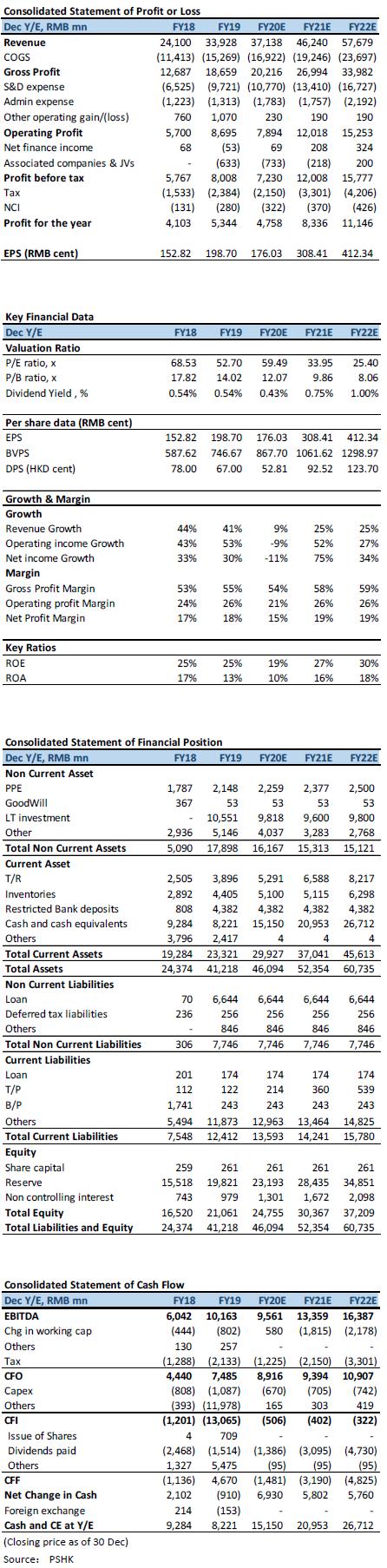

We believe that this transaction can effectively improve the cash flow level of the JV and accelerate its development of the three core brands. However, the basic factors in Anta's main business have little impact. Taking into account the one-time disposal gains of the Precor brand by AS Holding, for profit and loss, we adjusted the company's 2021 profit forecast and maintained the 2020 profit forecast unchanged. It is expected that the company's net profit attributable to the parent in 2020/21/22 will be RMB 47.6/83.4/11.15 billion (previously RMB 47.6/82.5/11.15 billion), and the corresponding EPS will be RMB 1.76/3.08/4.12 respectively.

Since December 7th, Anta Sports has been included as a constituent stock of the Hang Seng Index, becoming the only Chinese sports goods company in the Hang Seng Index, reflecting the recognition of the company by the capital market and attracting capital inflows from passive funds. The company's long-term investment value has not changed, focusing on the growth brought about by the company's main brand channel upgrade and the cultivation of new brands. Recently, the valuation of sportswear sector in Hong Kong stocks has been restored. The market is optimistic about the recovery of the industry after the epidemic. In addition, the policy risk of the industry is relatively low. Considering the company's short-term growth momentum and the large potential development space, we revise up the company's 2021 target P/E to 40.0x, corresponding to a target price of HK$144.94, which corresponds to 69.32x/40.0x/29.61x for 2020/2021/2022, and the Accumulate rating is maintain.

Risk

1) The impact of COVID-19 continues

2) Growth of newly acquired brands is not as expected

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()