-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Anta Sport(2020.HK) - Acceleration plan in next 12 months, Lead Anta to Win

Thursday, July 29, 2021  6901

6901

Anta Sport(2020)

| Recommendation | Accumulate |

| Price on Recommendation Date | $156.500 |

| Target Price | $178.240 |

Weekly Special - 002050 Sanhua

Investment Summary

Anta Sport announced the company's operating data for Q2 and the 1H on July 8. The company's retail sales value growth in the second quarter was outstanding. Anta's main brand 2Q21 retail sales value increased by 35%-40% Yoy; FILA brand 2Q21 retail sales value Yoy Growth of 30%-35%; 2Q21 retail sales value of other brands increased by 70%-75% Yoy. In the first half of the year, Anta and FILA's retail performance exceeded the company's original expected growth. In addition, the company also announced the `Lead to Win` acceleration plan in the coming 24 months, providing a clear development direction.

In 2Q21, Anta's main brand retail sales value increased by 35%-40% Yoy, and also recorded a growth of more than 35% compared to the same period in 2019. 1Q21 online retail sales value increased by 40% Yoy, compared with the same period in 2019 Compared with the recorded growth of more than 100%. Retail sales (in terms of retail value) recorded a Yoy growth of 35%-40% in 1H, which was higher than the company's originally growth target of 20%. The overall discount has returned to a normal level; the current inventory-to-sales ratio is about 5x, maintaining a healthy level; the offline sales rate in the second quarter increased by 10 ppts compared with 2019. The company's DTC transformation has been smooth, and the efficiency of DTC stores in 1H21 has been improved. Benefiting from the company's online and offline strategy of placing inventory, the Anta brand store efficiency recovered in 1H21 exceeded 300,000, which is higher than the store efficiency of wholesale stores and the same period in 2019.

FILA brand 2Q21 retail sales (in terms of retail value) still recorded a Yoy growth of 30%-35% despite the high base last year, and recorded a growth of more than 50% compared with the same period in 2019; medium-sized goods/children/fashion brands /Online Yoy growth was 20%+/40%+/80%+/40%+. In the first half of the year, the overall retail sales (in terms of retail value) of the FILA brand increased by 50%-55% Yoy, which was higher than the company's original expectation of 30%. In 2Q21, the discount level is about 20% off (including Outlet). If the outlet is not included, the discount level is 14% off, which is an improvement over Q1; the inventory sales ratio is currently 6x, which is an improvement over 2020. The overall performance of offline stores has improved compared with 2020 and 2019.

Other brands` 1H21 retail sales value increased by 90%-95% Yoy, and increased by more than 100% compared to the same period in 2019. The 1H21 retail sales (in terms of retail value) of Descente/Kolon increased by 100%+/40%+ Yoy, respectively, and recorded an increase of 200%+/50%+ respectively compared with the same period in 2019. Descente estimates that the number of stores at the end of the year will be about 200, and the retail sales value this year is expected to exceed 2 billion.

Impressive five-year development goal, and the main brand transformation in many ways

The company released the Five-Year Development Strategy and the rapid growth `Lead to Win` in the next 24 months. The strategic goal is divided into two parts, Leader in Scale and High Quality Growth. In the next 5 years, the main brand retail sales value aims to maintain 18-20% CAGR growth, and the market share will increase by 3~5 ppts; in addition, we will strengthen the layout of the first to third-tier cities, and the target will account for more than 50% of sales

in the next 5 years, and the number of shopping malls will increase. The online retail sales value will maintain a CAGR growth of 30% in the next 5 years, and its proportion will increase to 40%.

The company Lead to Win is divided into two major directions, eight aspects. The two main directions are rooted in & known for performance sport and brand transformation & growth; in terms of rooted in & known for performance sport, the company proposes three aspects: 1) Continue to sponsor outfits for the national team; 2) Leverage global advanced sports R&D capability; 3) Breakthroughs in core sport categories - running, basketball and women's series. In terms of brand transformation & growth, the company proposes five aspects: 4) Focus on the Summer and Winter Olympics; 5) Win and lead the Generation Z; 6) Speed up DTC transformation and digital transformation; 7) Maintain Anta Kids` position as a market leader 8) Promote sustainable development and sports charities.

1. Continue to sponsor outfits for the national team:

At present, the company has sponsored competition equipment for 28 national teams in total, and will continue in the future, leading the brand's professional innovation and research and development capabilities

2. Leverage global advanced sports R&D capability:

The company plans to invest more than CNY 4 billion in the next five years to improve the global R&D system, build five major design R&D centers and human resources teams in China, the United States, Japan, Korea, and Italy; deepen cooperation with topuniversities and scientific research institutions; integrate global material chemical suppliers and manufacturers; Continuous precession sports research and development innovation

3. Breakthroughs in core sport categories:

The company will continue to focus on running, basketball core sport products and women's series

Running category: Create `nitrogen technology` platform and running brand matrix, increase the product price band to CNY 1,399-1,599, and increase the annual sales of running shoes from 20 million pairs to 40 million pairs in the next five years.

Basketball category: Build basketball brand image that represents the young generation, continue to support international top basketball superstars, and invest in young high-potential stars. Raise the price of the product to more than CNY 1,500, and thesales volume in the next five years will increase from 6 million pairs to 12 million pairs per year.

Women's Series: The target is to reach CNY 20 billion in retail sales value by 2025.

4. Focus on Summer and Winter Olympics:

Focusing on the "Double Olympics" of the 2020 Tokyo Olympics and the 2022 Beijing Winter Olympics, taking advantage of the opportunity to promote the brand image, the Anta Champion Store will be launched to tell the Olympic story of the Chinesenational team in the image store. Champion stores are mainly located in CBD in first- and second-tier cities, and 50-80 stores are expected to be opened in 2022.

5. Win and lead the Generation Z:

Open up new sports tracks in response to the preferences of Generation Z; cooperate with top sports stars such as Wang Yibo and Eileen Gu (谷愛凌) to enhance the image of the Anta brand among young people; cultivate a young designer platform;cooperate with KOLs from all walks of life to strengthen the social platform Interact with Gen Z.

6. Speed up DTC transformation and digital transformation:

DTC transformation

In the next 24 months, it is expected to increase the proportion of DTC in the overall retail sales value to 70%. By strengthening quick return and online operations, product efficiency will be improved, and store efficiency will increase by 40%; the proportionof mainstream channels will be strengthened to increase the first to third-tier cities market share and number of shopping mall stores.

Digital transformation

Company plans to invest more than CNY 400 million in the next 24 months to strengthen digital capacity building. By 2025, the number of effective members will be doubled from the current 50 million to 120 million, with a member contribution rate of 70%and a member repurchase rate of 40%. In the next 24 months, the 5-month sales rate of commodities will increase to 75%.

7. Maintain Anta Kids` position as a market leader:

Consolidate the leading position in the children's sports market, strengthen the R&D of children's exclusive sports technology, optimize the channel structure to maintain high growth in store efficiency, and target online business to account for more than40% by 2025. Increase Anta's market share in the children's sports market. The company currently ranks first in China's children's sports market share, and its market share is 1.3x that of the second place.

8. Promote sustainable development and sports charities:

In the next three years, company plan to invest CNY 600 million in sports charity to support rural revitalization; continue to promote ESG construction and sustainable product research and development, and strengthen corporate social responsibility.

Valuation model adjustment

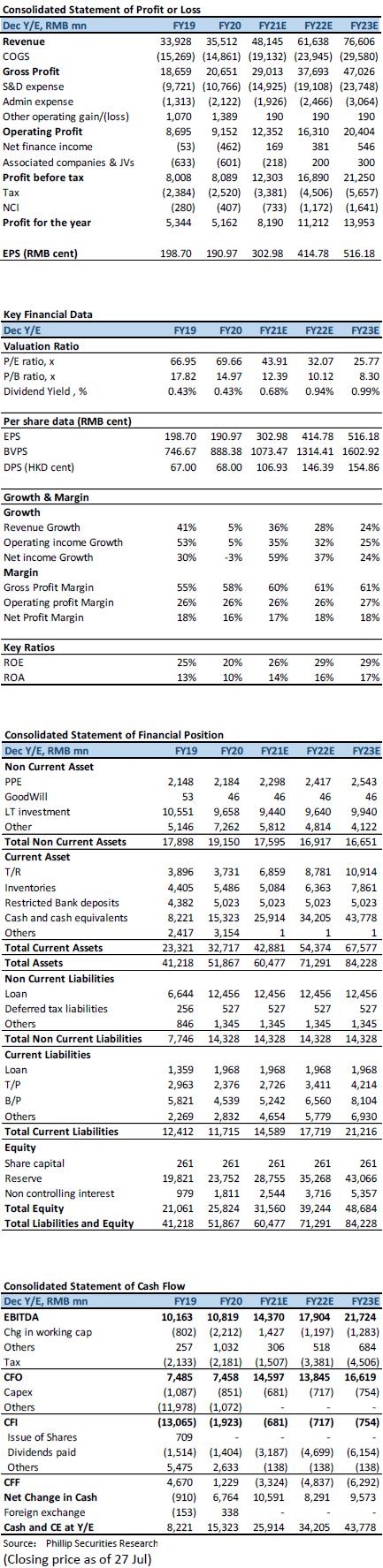

We have adjusted the valuation model and raised the company's FY21/FY22/FY23 revenue to CNY 481.4/616.4/76.61 billion (previously: CNY 462.4/565.3/68.09 billion); as the company expects DTC to be in the main brand The proportion increased. We raised the company's FY21/FY22/FY23 GPM to 60.3%/61.2%/61.4% (previously: 59.3%/59.5%/60.0%); raised the company's FY21/FY22/FY23 net profit to CNY 8.19/11.21 /13.95 billion (previously: CNY 7.77/10.20/12.53 billion).

Valuation and investment thesis

The company's retail sales value growth target set for the next five-year strategy is more aggressive and higher than other peers` expectations. However, the company also puts forward a clear development plan for coming 24 months. We are confident in the company's future development of the main brand. It is estimated that the company's EPS in 2021/2022/2023 will be CNY 3.03/4.15/5.16. The company's future growth expectations have increased, and the company's target price-earnings ratio has been raised to 50x FY21 (previously: 45x FY21). The company's target price has been adjusted to HK$178.24 (previously: HK$152.24) corresponding to 50.00/36.53/29.35 times expected earnings in 2021/2022/2023 Rate, maintain a accumulate rating.

(Current price as of July 27)

Risk

1) The growth of newly acquired brands falls short of expectations

2) Rebranding has not been recognized by consumers

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()