-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

TK Group (2283.HK) - Steady Growth Mode with Diversified Customer Network

Tuesday, January 10, 2017  11189

11189

TK Group(2283)

| Recommendation | Buy |

| Price on Recommendation Date | $2.180 |

| Target Price | $2.800 |

Weekly Special - 2333 Great Wall Motor

We had a conference call with Executive Director, Chief Financial Officer & Assistant to Chairman Franky Cheung to conduct research on TK Group.

Company Overview

TK Group was established in Hong Kong in 1983. Business expanded to an industrial park of over 100,000 sq.meters (incl. Guangming Shenzhen, Buji Shenzhen, Suzhou and Germany) with a family of over 3,000 staff from a 70 sq. meters factory with 7 staff at the beginning. It was successfully listed on the main board of Hong Kong Stock Exchange on 20 Dec 2013.

The board of directors recently announced that according to the market research report of Ipsos Hong Kong Limited, TK Group exported approximately RMB470 million of plastic injection molds in 2015, representing 4.5% of PRC total export value of plastic injection molds in the amount of approximately US$1.69 billion, making it the largest PRC manufacturer of plastic injection molds with level above MT3 (in terms of export value) in 2015. The board of directors also announced that the Company received the ``2016 Hong Kong Awards for Industries: Upgrading and Transformation Award`` from the Hong Kong Young Industrialists Council recently.

The development of TK Group benefits from China`s policy support, including “Made in China 2025” and “Industry 4.0”. The Company began to use the smart flexible production lines with Industry 4.0 concept in early 2015. It began to use automation technique to produce different products in the same line, which enhanced the production efficiency and therefore effectively controlled labor costs.

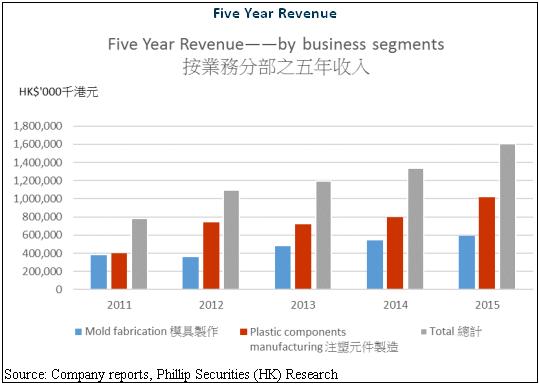

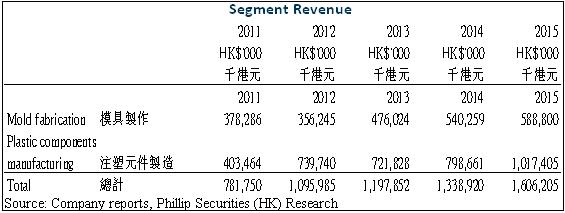

There are two main business segments——Mold fabrication business and plastic components manufacturing business. In 1H2016, the turnover of the mold fabrication business division amounted to approximately HK$290.2 million, representing an increase of approximately 18.8% YoY and accounting for 40.2% of total revenue (from external customers). And the gross profit margin is 26.2%. And the turnover of the plastic components manufacturing business division amounted to approximately HK$431.1 million, representing a decrease of 11.9% YoY, and accounting for approximately 59.8% of the Group`s total revenue. Thanks to the Group`s efforts in automation and product mix adjustment, the segment`s gross profit margin increased from 23.4% to 26.6% YoY.

Revenue grew gradually from 2011 to 2015 at a CAGR of 19.7%.

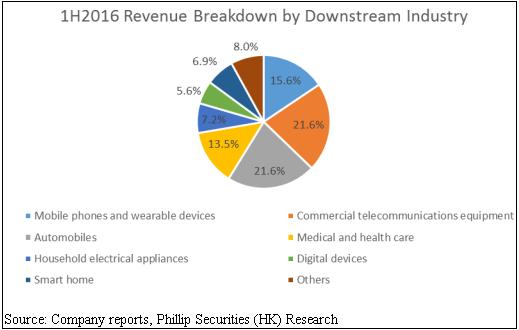

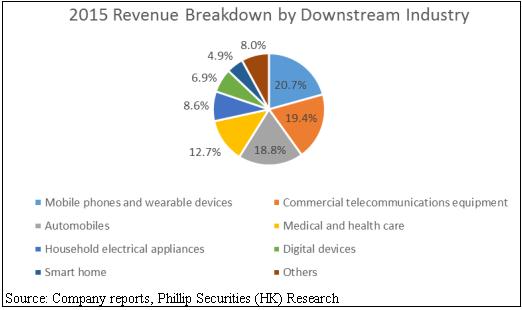

The clients of TK Group are from different sectors and are diversified enough to spread the risk of one specific industry suffering the economic slowdown. In 1H2016, the global and China market faced economic slowdown, demands for high-end electronics declined. Revenue from mobile phones and wearable devices division decreased by over 30% YoY. However, thanks to the rapid growth of automobiles molds and smart home markets, the total revenue only declined slightly. Automobile segment grew by 32.1% YoY, driven by the new automobile mold business in Germany. And smart home segment grew by 220.6% YoY, driven by new orders from a leading smart home brand customers and its rapid growth. Total revenue in 1H2016 was HK$721.3 million, representing a decrease of 1.7% YoY.

The Group recorded a profit attributable to owners of the Company for 1H2016 of HK$78.9 million (1H2015: HK$71.2 million), representing a YoY increase of 10.8%. The net profit margin for the period was 10.9% (1H2015: 9.7%).

Here`s the charts for 1H2016 and 2015 revenue breakdown by downstream industry:

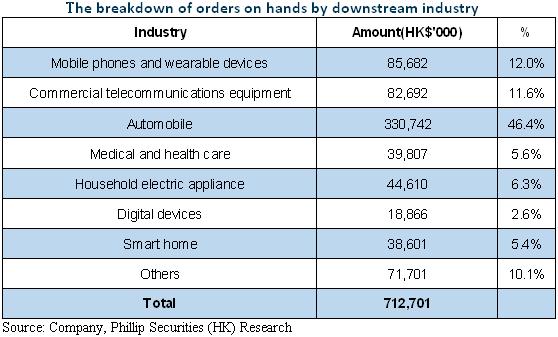

The Group has sufficient orders on hand. As at 30 June 2016, the Group`s orders on hand was HK$712.7 million, representing an increase of 7.8% YoY. The following table shows the breakdown of orders on hands by downstream industry. On 30 Nov 2016, the Group`s orders on hand increased to around HK$750 million.

Company Products and Diversified Customer Network

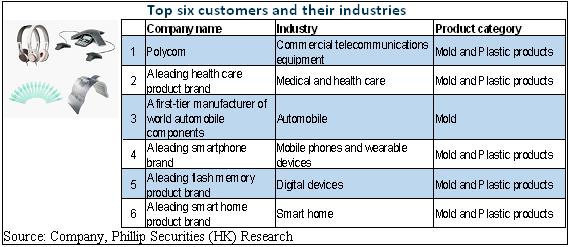

The following table shows 1H2016 top six customers and their industries. The top six customers contributed 51.7% of TK`s revenue in 1H2016. The cooperation with top six customers has a long history. Management mentioned that the cooperation with the largest customer Polycom has a history of 25 years. And the customer relationship is relatively strengthened.

Production Base and Capacity

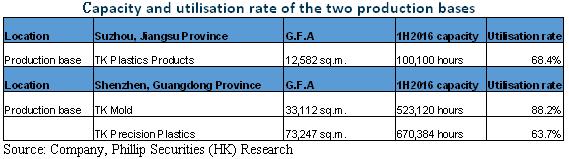

TK Group has two production bases in China——Suzhou, Jiangsu Province and Shenzhen, Guangdong Province. The following table shows 1H2016 capacity and utilisation rate of the two production bases.

Future Segment Growth Expectation

TK Group might benefit from the development of mobile phones and wearable devices, automobiles molds, medical and health care, smart home and virtual reality(VR) segments in the future.

Mobile phones and wearable devices: The Group`s mobile phones and wearable devices division experienced a decline of over 30% YoY in 1H2016. We expect a segment growth recovery in 2H2016 and the segment may perform better in 2017.

Automobiles molds: The Group developed its automobiles molds business in Germany through the newly acquired German Subsidiary. Now it`s mass production stage. And the Group focuses on customer confidence building in Germany. Future performance of the segment may be driven by the business in Germany.

Medical and health care: We expect a faster segment revenue growth in 2017.

Smart home: Market research institution “Markets And Markets” issued a report anticipating the global smart home market may be worth US$122 billion in 2022 at a CAGR of 14%. The smart home segment growth is also expected to accelerate in the future.

Virtual reality(VR): Another market research institution SuperData anticipates the market value for VR to reach $28 billion by 2020. Oculus under Facebook has begun the cooperation with TK Group. The businesses include precision molds and plastic injection. The VR segment growth is expected to accelerate in 2018 accompanied with VR market`s potential growth.

Prospects for Development

The Group keeps faith with its well-established philosophy of diversified customers and its development strategy of focusing on high-precision molds in these years. The precision mold design has core technology and is better than competitors` technology. It will drive the growth of plastic components manufacturing business. The dividend payout ratio is expected to rise to 50%. And the company positions itself as a high-tech company with high dividend payout ratio. As for gross profit margin, mold fabrication has long production cycle. Because of the lag effect, economy efficiency from capacity expansion will reflect in the financials later and the gross profit margin may rise in FY16. Part of FY17 CAPEX will be used for the development of automation. Automation may cause labor cost to drop and decline in number of employees.

TK Mold (Shenzhen) Limited and TK Precision Plastics (SZ) Limited, subsidiaries of the Group, were recognized as “New and High Technology Enterprise” and thus enjoy a preferential CIT rate of 15% from 1 January 2014 to 31 December 2016 and 1 January 2015 to 31 December 2017, respectively. Tax rate is reviewed every three years, and management expects they will continue enjoying a preferential tax rate.

TK group`s financial situation is good, and they are considering buying into upstream and downstream companies and will have synergistic effect.

The Impact of RMB Depreciation on the Company

The mold fabrication business benefited more from RMB depreciation because steel as raw materials was paid using RMB. For the plastic components manufacturing business, raw materials were bought from outside China, so the segment benefited less. Because mold fabrication has long production cycle and sales is affected by the lag effect, the recent RMB depreciation may reflect in the financials of FY17. And most of the company cost is paid by RMB, while most of the revenue is USD and EURO. Such structure benefits from RMB depreciation. At the end of June 2016 company`s cash is mainly HKD and USD, however, in 1H2015 it`s mainly RMB. From 2H2015 company forecasted the RMB might depreciate and bring potential risk and therefore changed RMB deposit into foreign currency.

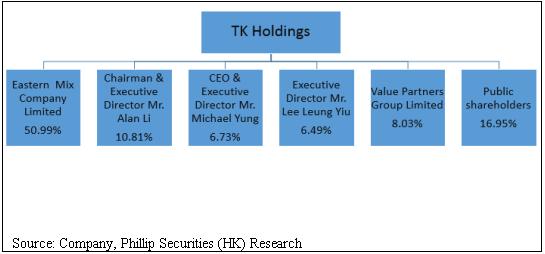

Shareholding Structure

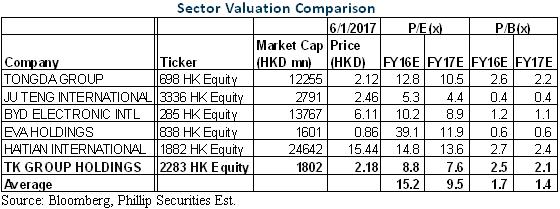

Peers Comparison

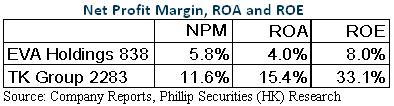

Among them, EVA Holdings(838 HK) is the most similar company. The following table shows the respective Net Profit Margin, ROA and ROE of the two companies in 2015:

We can see that TK Group has stronger profitability. EVA Holdings announced the net profit in 1H2016 was HK$ 22.998 million with an 80.5% decrease YoY. However, TK Group announced the net profit in 1H2016 was HK$78.9 million with a 10.8% increase YoY.

Valuation

Buy rating is given with TP of HK$2.80. TK Group is the largest PRC manufacturer of plastic injection molds with level above MT3 (in terms of export value) in 2015. After the conference call with management, we forecast net profit growth of 9.8/16.1% in FY16/17, driven by 3.0/12.0% revenue growth. Our TP of HK$2.80 represents 9.8 FY17E P/E, which is higher than the industry average. It also represents 0.55x PEG on an expected 17.8% EPS CAGR during FY16-18, which is lower than industry average. We believe TK Group deserves a higher multiple than 9.5 given its historical steady growth, diversified product structure which can spread the risk caused by slowdown in global economic growth, high dividend payout ratio and scarcity premium. (Closing price as at 6 Jan 2017)

Risk

The liquidity risk in the trading process;

The company doesn`t maintain long-term purchase contracts with their customers, decrease or termination in the purchase orders by the customers may affect the company`s financial results;

Fluctuations in the price of raw materials.

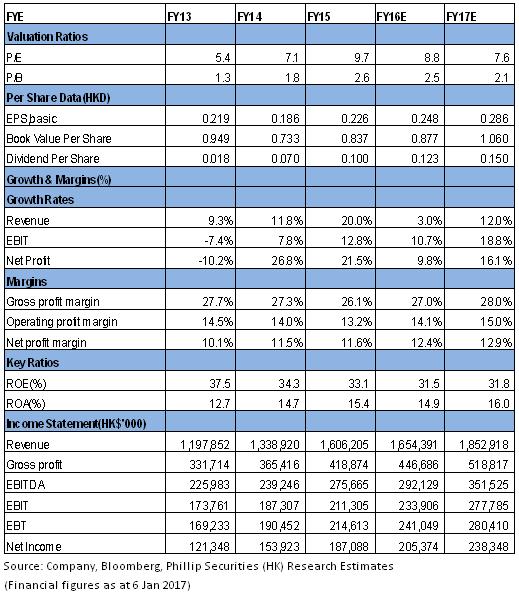

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()