-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

VTech Holdings Limited (303.HK) - Gigaset Boosting Telecommunications, Solid Margin Expansion

Monday, March 31, 2025  1605

1605

VTech Holdings Limited(303)

| Recommendation | Accumulate |

| Price on Recommendation Date | $57.700 |

| Target Price | $64.400 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

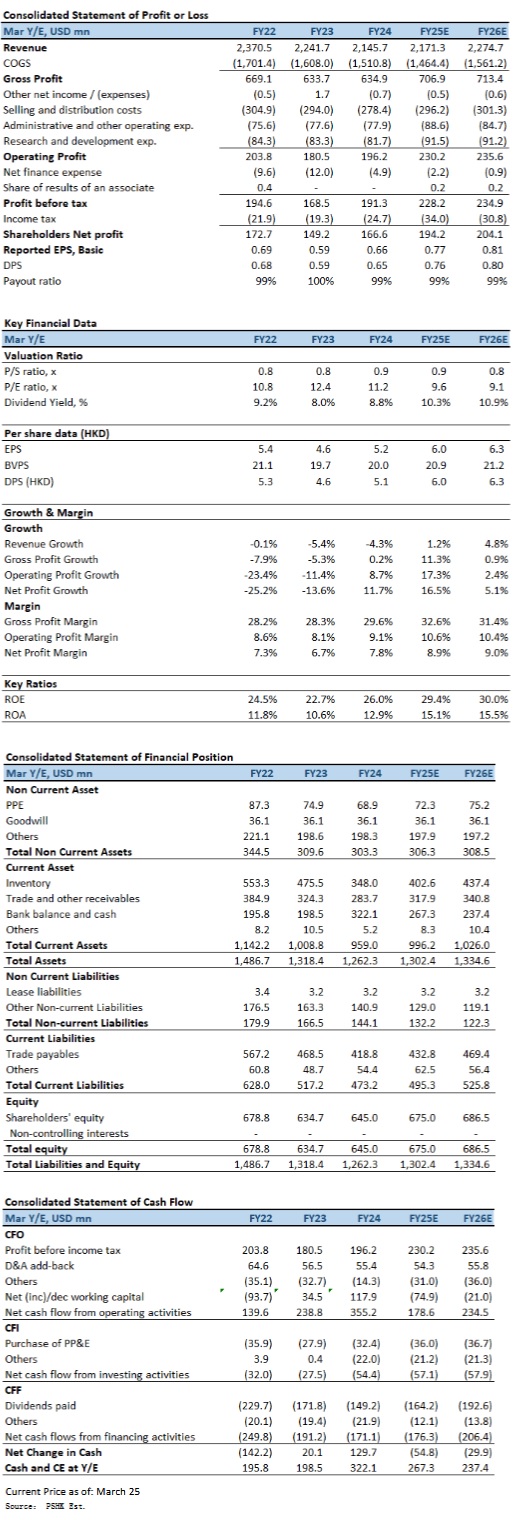

VTech Holdings Limited (00303.HK) reported revenue of USD 1.09 billion for the first half of the 2025 fiscal year (six months ended September 2024), a year-on-year decline of 4.5%. Despite an improvement in gross margin to 31.5% (compared to 28.5% in the previous year), net profit attributable to shareholders dropped by 6.6% to USD 87.4 million due to lower revenue and higher operating expenses associated with the Gigaset acquisition. Basic earnings per share (EPS) decreased by 6.5% to USD 0.346. The interim dividend was maintained at USD 0.17 per share, reflecting management's confidence in the company's stable cash flow.

Revenue Decline but Solid Margin Expansion

Total revenue for the first half of the fiscal year was USD 1.09 billion, down 4.5% year-on-year. The decline was primarily driven by weaker demand in the North American, European, and Asia-Pacific markets, where revenues decreased by 7.4%, 1.4%, and 7.1%, respectively. North America's revenue fell to USD 453.1 million, Europe's revenue reached USD 462.1 million, and Asia-Pacific revenue stood at USD 159.4 million. In contrast, revenue from other regions, including Latin America, the Middle East, and Africa, surged by 33.6% to USD 15.1 million, though these regions remain a small portion of overall sales.

Gross margin increased from 28.5% to 31.5%, mainly benefiting from lower material costs, improved product mix, and contributions from the Gigaset acquisition. Despite the margin expansion, the ongoing integration of Gigaset led to higher operating expenses, resulting in a 5.5% decline in operating profit to USD 104.2 million, with an operating margin of 9.6%, down from 9.7% in the previous year. Net profit attributable to shareholders decreased by 6.6% to USD 87.4 million

U.S. Recovery, Weak European Demand

Revenue from electronic learning products (ELPs) totaled USD 404.0 million, recording a 1.9% year-on-year increase, making it the most stable segment in the company's portfolio. In the U.S., ELP sales rose by 7.4% to USD 224.0 million, benefiting from a market rebound and the implementation of new sales and marketing strategies. Both the VTech and LeapFrog brands recorded sales growth, maintaining their leadership in the infant and preschool electronic learning category. However, European revenue for ELPs declined by 6.3% to USD 137.0 million, as sluggish economic growth, high interest rates, and inflation eroded consumer disposable income, leading to cautious ordering from retailers. The Asia-Pacific market grew by 1.1% to USD 35.4 million, supported by sales recovery in Australia and mainland China. The Australian market benefited from effective marketing campaigns and new product launches, while China's growth was driven by increased sales in both online and offline channels.

Revenue from telecommunications products reached USD 193.9 million, representing an 18.3% year-on-year increase, primarily driven by the Gigaset acquisition. In Europe, telecom revenue surged by 93.4% to USD 84.5 million, with strong contributions from Gigaset's commercial and residential phone businesses. While the overall market remains in decline, the inclusion of Gigaset's sales significantly boosted the segment's performance. In contrast, North America's tele-communications revenue declined by 11.3% to USD 92.2 million, affected by weakening market demand. Although the home phone segment performed better than the broader market, it remains in a long-term downward trend. The commercial phone business also suffered a decline due to reduced orders from a key customer. Asia-Pacific telecommunications revenue fell by 16.4% to USD 9.7 million, mainly due to declining sales of residential phones and other telecom products in Australia and Japan. While SIP phone sales showed some growth, it was insufficient to offset declines in other product categories.

Revenue from Contract Manufacturing Services (CMS) fell by 15.3% year-on-year to USD 492.0 million, making it the most significant drag on overall earnings. North American CMS revenue declined by 22.6% to USD 137.1 million, as weak end-market demand and excess inventory at key customers led to a reduction in orders across multiple product categories. European CMS revenue also fell by 13.7% to USD 241.0 million, primarily due to lower sales of professional audio equipment, headsets, and smart energy storage systems. Asia-Pacific CMS revenue declined by 8.5% to USD 114.3 million, impacted by weaker sales of professional audio equipment, medical and healthcare products, and communication devices.

The integration of Gigaset is progressing well, with management expecting full completion by the end of 2024. The acquisition has already contributed to improved gross margins. In the electronic learning products segment, the recovery in the U.S. market is a positive sign. The newly implemented sales and marketing initiatives have shown encouraging results, and management aims to continue driving growth in standalone and licensed preschool products. However, global macroeconomic uncertainties remain a key risk. High interest rates, geopolitical tensions, and weak consumer demand could continue to weigh on sales. The CMS business, in particular, may take longer to recover due to end-market softness, though management is actively expanding global manufacturing capacity in Malaysia and Mexico to enhance long-term competitiveness.

Investment Thesis and Valuation

VTech's profitability has improved, but revenue growth remains a challenge. The integration of Gigaset is progressing well and is expected to provide long-term growth momentum. However, weak demand in CMS and macroeconomic uncertainties pose near-term risks, we forecast the company's earnings per share (EPS) for FY2025 and FY2026 to be 0.77 and 0.81 USD, respectively. Our target price is set at HK$64.40, corresponding to a 10.7x forward P/E ratio for FY2025, which is in line with the company's five-year historical average valuation. Our investment rating is “Accumulate”.

Risk factors

1) Global Economic Slowdown; 2) Slow Recovery in CMS Business; 3) European Market Integration Risks; and 4) Geopolitical and Supply Chain Risks.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()