-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

FSE Lifestyle Services (331.HK) - Core net profit recorded a considerable growth, with total outstanding contract sum of HK$10.7B

Friday, December 23, 2022  6855

6855

FSE Lifestyle Services(331)

| Recommendation | Buy |

| Price on Recommendation Date | $5.280 |

| Target Price | $6.730 |

Weekly Special - 2333 Great Wall Motor

FSE Lifestyle Services (“FSE”) are a lifestyle services conglomerate with 3 major business segments: property & facility management services, city essential services and E&M services. FSE's services are being delivered through 8 major groups of companies which include Urban Group, Kiu Lok Group, Waihong Services Group, FSE Environmental Technologies Group, Hong Kong Island Landscape Company Limited, General Security Group, Nova Insurance Group and FSE Engineering Group. FSE offer comprehensive “one-stop shop” professional services to its clients who are engaged in a wide diversity of projects, including property developments, public infrastructures, education and transportation facilities, as well as entertainment and travel industries in Hong Kong, Macau and the Mainland China. FSE clientele includes the HKSAR Government, multinational corporations, owners and investors of properties, theme parks, universities, hotels and hospitals covering both private and public facilities.

Core np recorded a considerable growth, with total outstanding contract sum of 10.7B

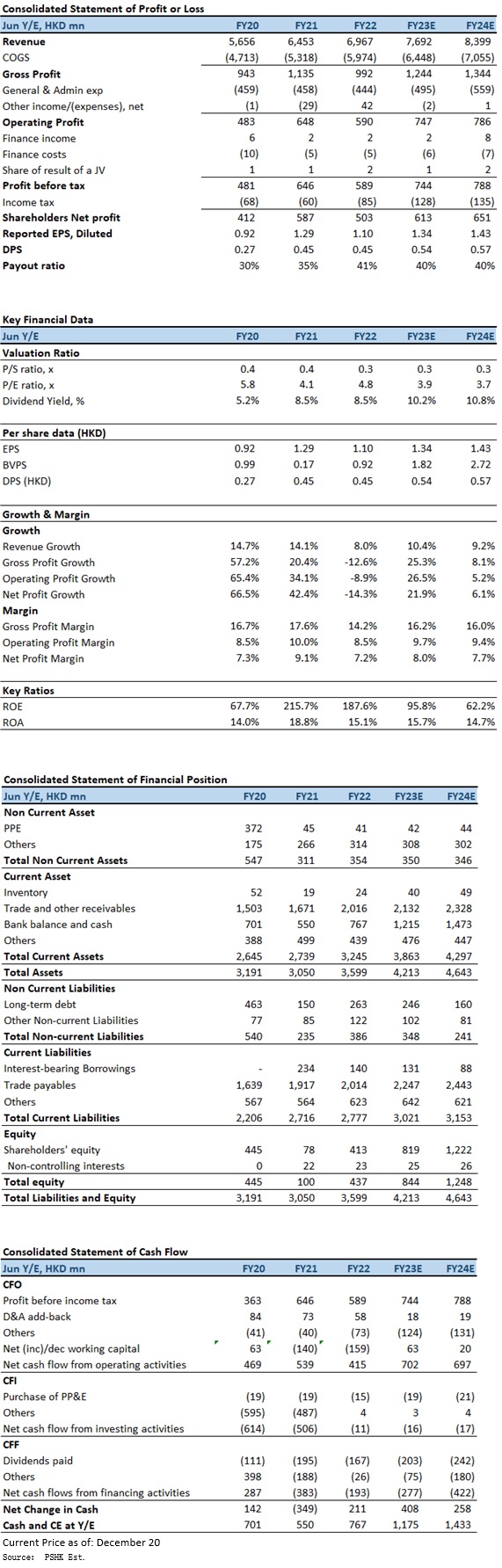

In FY2022 (for the year ended 30 June 2022), FSE's recorded revenue amounting to HK$6,966.9mn, representing an increase of HK$514.2mn or 8.0%, as compared with HK$6,452.7mn in FY2021. Profit attributable to shareholders was HK$502.9mn, representing a decrease of HK$84.0mn or 14.3% as compared with HK$586.9mn in FY2021, mainly resulted from a decrease in government grants. If excluding the effects of government grants, adjusted net profit for the FY2022 of 35.2% to HK$414.7mn (i.e. after excluding government grants of HK$88.2mn from profit attributable to shareholders of the Company of HK$502.9mn for the Year) as compared to adjusted net profit of HK$306.8mn for FY2021. Basic EPS was HK$1.10, a decrease of 14.7% YoY. The total dividends for 2022 was HK45.0 cents (2021: HK45.0 cents) per share, the dividend payout ratio is 41.0% (calculated based on the adjusted profit), while the dividend payout ratio was 48.7%, calculated based on the adjusted profit for the year ended 30 June 2021.

The gross profit decreased by HK$142.6mn or 12.6% to HK$992.5mn from HK$1,135.1mn in FY2021, with an overall gross profit margin decreased to 14.2% from 17.6%, mainly reflecting a decrease in COVID-19 related government grants. If excluding the effects of these grants, adjusted gross profit margin increased to 13.6% from 12.8% last year, mainly caused by an improvement in the gross profit margin of the E&M services segment.

By business segment, city essential services segment revenue grew by 8.5% or HK$254.0mn to HK$3,252.6mn from HK$2,998.6mn (restated), contributed 46.7% (FY2021: 46.5% (restated)) of the total revenue. The growth is mainly reflected a number of new general cleaning service contracts, which encompassed a wide range of buildings and facilities, including university campus, shopping malls, hospital, government buildings and residential and commercial properties, and additional ad-hoc intensive disinfection cleaning contracts; higher revenue from its environmental solutions business, especially in respect of its provision of ELV device installation services, largely contributed by 11 SKIES project in Chak Lap Kok; higher revenue from its technical support and maintenance services in Hong Kong contributed from the refurbishment works for a hotel in TST and the maintenance works for 2 residential properties in Shatin and Sai Wan Ho and an increase in new insurance contracts for construction projects awarded. Segment recorded a decrease in its gross profit of HK$193.3mn or 30.8% to HK$434.4mn from HK$627.7mn (restated) , with its gross profit margin decreased to 13.4% from 20.9% (restated), reflected a decrease in COVID-19 related government grants; a reduction in gross profit contribution from its security guarding & event services resulted from a lower demand in event services affected by the fifth wave of COVID-19 and a lower gross profit contribution from its technical support and maintenance services following the completion of Venetian contracts in Macau last year. Segment profit was 201.5mn, decrease 45.3% YoY.

Property & facility management services segment revenue grew by 5.8% or HK$38.1 million to HK$696.3mn from HK$658.2mn, contributed 10.0% (FY2021: 10.2%) of the total revenue. Such growth was mainly driven by newly awarded property management contracts for car parks of shopping malls, additional works for staff quarters of a university and increased commission income from property sales and leasing partly offset by a reduction in revenue from pandemic-induced additional works for government buildings. This segment recorded a decrease in its gross profit of HK$23.5mn to HK$219.4mn from HK$242.9mn, with its gross profit margin decreased to 31.5% (FY2021: 36.9%), reflected a decrease in COVID-19 related government grants. Segment profit was 136.3mn, increased by 1.6% YoY.

E&M services segment revenue increased by 7.9% or HK$222.1mn to HK$3,018.0mn from HK$2,795.9mn (restated), contributed 43.3% (2021: 43.3% (restated)) of the total revenue. Such growth reflected an increase in revenue contribution from Mainland China, Macau and Hong Kong by HK$122.9mn, HK$85.8mn and HK$13.4mn respectively. The gross profit of the E&M services segment increased by HK$74.2mn to HK$338.7mn from HK$264.5mn (restated) with its gross profit margin increased to 11.2% (FY2021: 9.5% (restated)), principally reflected a higher gross profit margin contributed by its Inland Revenue Tower project in Kai Tak. Segment profit was 173.4mn, increased by 60.1% YoY.

As of 30 June 2022, the property & facility management services segment has a total gross value of contract sum of HK$2,074mn with total outstanding contract sum of HK$1,162mn; the city essential services segment has a total gross value of contract sum of HK$7,643mn with a total outstanding contract sum of HK$4,415mn; the E&M services segment has a total gross value of contract sum of HK$9,009mn with a total outstanding contract sum of HK$5,085mn. The total gross value of contract sum of the above-mentioned is HK$18,730mn, and the total outstanding contracts sum of HK$10,660mn. With the sufficient reserve of outstanding contracts project, future revenue growth would be guaranteed.

Investment Thesis

After completing multiple acquisitions in the past, including property and facility management services, the overall business scale of FSE has been significantly expanded. Further to the strong synergies generated among business units within the group, it has also maximized cost-effectiveness and operational efficiency at all times. With the increasing expectation of the corporate clients and property investors, there is a growing demand of enhanced services and one-stop solutions in professional property and facility management services. FSE's compound annual growth rate (CAGR) of revenue and profit from FY2017 to FY2022 reached 14% and 24%, respectively. Upon the government policy on increasing the supplies of residential units by the coming 10 years, the increasing supply of both private and public housing units, hence, creates a growing demand and necessities of professional property management services in the territory, which is expected to bring huge market opportunities to FSE. We expect FY2023E-FY2024E EPS to be HK$1.34 and HK$1.43 respectively, with PT of HK$6.73, implies a FY2023E P/E of 5.01x (~5-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()