-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Logan Property (3380.HK) - Direct Beneficiary of the Greater Bay Area National Policy

Wednesday, April 19, 2017  18591

18591

Logan Property(3380)

| Recommendation | Accumulate |

| Price on Recommendation Date | $4.640 |

| Target Price | $5.500 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

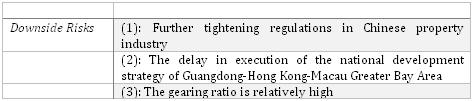

- Direct beneficiary of the national development strategy of Guangdong-Hong Kong-Macau Greater Bay Area

- Majority of the land and project reserve, in terms of either GFA or saleable resources, are located in Shenzhen

- Well-positioned projects, especially those in Shenzhen, which are located above or close to Metro stations, allowing the company to charge high and solid prices

Business Overview

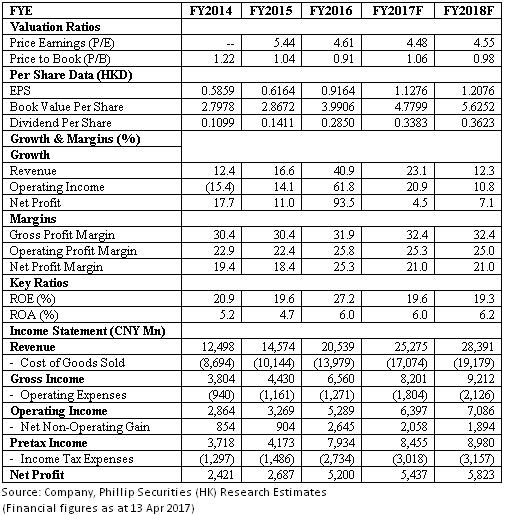

Outstanding FY2016 result: Benefiting from the rapid rise in property price in Shenzhen in recent years, Logan Property achieved an outstanding result in FY2016. Revenue rose 40.9% to CNY20,538.8Mn and net profit rose 69.4% to CNY4,487.7Mn. Gross profit margin improved from 30.4% in FY2015 to 31.9% in FY2016. Contracted sales increased 40% in FY2016 to CNY28,716Mn while contracted sales area decreased 4.9% in FY2016, implying that the overall increase is caused by the 44.9% increase in average contracted selling price to CNY11,870 per square foot. Because of the outstanding result and strong growth achieved in FY2016, Logan Property has declared CNY0.22 dividend and CNY0.03 special dividend per share.

Direct beneficiary of Guangdong-Hong Kong-Macau Greater Bay Area national development strategy: Logan Property has a first mover advantage in the Guangdong-Hong Kong-Macau Greater Bay Area. In the early years, Logan Property has established its strategic positioning in the region by engaging in development projects and building up land reserve in Shenzhen, Huizhou, Foshan, Zhongshan, Zuhai, Guangzhou and Dongguan. All of these cities form an integral part of the national policy submitted by the Chinese Premier Li Keqiang in Study on the Action Plan for the City Cluster in the Guangdong-Hong Kong-Macau Greater Bay Area`.

Logan Property has projects or land reserve in most of these cities and is the reason Logan Property will directly benefit from the Greater Bay Area national policy.

Logan Property is expected to benefit from the national policy by the fact that they have a large land reserve and large amount of property development projects in the region with a competitive cost, thereby allowing Logan Property to stay ahead of other property developers and enjoy a first mover advantage because of Logan Property's years of experience in the region and a built up land reserve enough for development for the next 5 to 6 years.

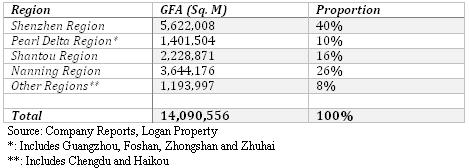

Large land reserve with a competitive cost: Logan Property has a large land reserve located around the Guangdong-Hong Kong-Macau Greater Bay Area but has a competitive cost because Logan Property has established its strategic positioning in the region in early years before the property market in the region went wild. As at 31/12/2016, Logan Property's land bank had a total GFA of 14.09Mn square metres, with an average cost of CNY3,384 per square metres. A substantial amount of land, in terms of GFA, is located in Shenzhen and about half of the land, in terms of GFA, falls into the region covered by the national policy `Guangdong-Hong Kong-Macau Greater Bay Area`.

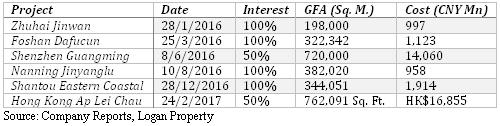

Apart from using the land acquired a few years ago, Logan Property has been actively acquiring several land and projects in China throughout FY2016 and a Hong Kong project at the beginning of FY2017.

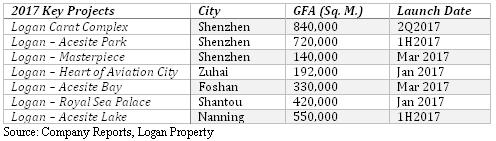

Well-positioned property development projects: Logan Property has set an annual sales target of CNY34.5Bn, a growth of 20% in comparison with FY2016. In particular, the majority of the saleable resources come from Shenzhen, indicating that Logan Property could enjoy a higher profit margin if the sales in FY2017 consist of a large proportion of sales from Shenzhen. The majority of the key property projects to be released in FY2017 are located in Shenzhen and thus are expected to bring sizable revenue to Logan Property.

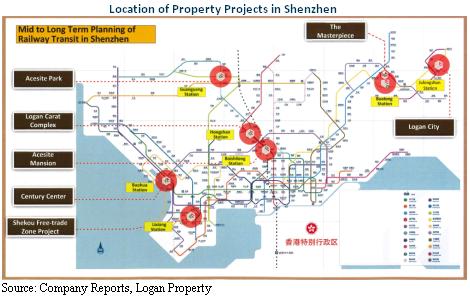

The property development projects of Logan Property, especially those in Shenzhen, are well-positioned in the city by locating close to the Metro stations. Locating close to or right above the Metro station will allow Logan Property to charge a solid selling price on these properties.

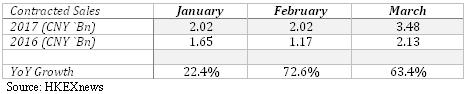

Strong sales is expected to continue: Logan Property has made sizable contracted sales in the first three months of FY2017 and that was a rapid increase in comparison with the contracted sales result of the same period in FY2016.

The company also has a large receipt in advance, indicating that the company will have a sizable revenue waiting to be recognised in the near future.

With the strong contracted sales in the first quarter of FY2017 and the large reserve of receipt in advance as at 31/12/2016, Logan Property is expected to have a strong solid revenue base for FY2017. Sizable growth in revenue in comparison with that of FY2016 is also expected especially the revenue of FY2016 was only CNY20,539Mn, whereas the receipt in advance as at 31/12/2016 was already CNY16,049Mn. The sales of property is also expected to continue to be strong in the future, not only because the property projects are located close to or above the Metro station, but also because it has a high quality land reserve, which has strong economic development around the region as well as is included in the Greater Bay Area national development strategy of the Chinese government. Therefore, Logan Property is expected to have long term sustainable growth in the future, in terms of both its sales and profitability.

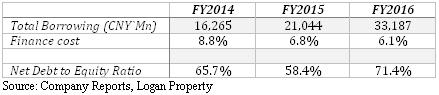

Finance cost decreased despite total borrowing increased: The finance cost of Logan Property decreased despite the total borrowing increased from CNY21,044Mn in FY2015 to CNY33,187Mn in FY2016, an increase of 57.7%. The net debt to equity ratio increased from 58.4% in FY2015 to 71.4% in FY2016 but the weighted average borrowing cost has decreased from 6.8% to 6.1%.

Total borrowing has increased rapidly in FY2016 but finance cost has decreased, indicating that the investors are optimistic towards Logan Property's future. Moreover, as at 31/12/2016, the cash on hand of Logan Property, including restricted cash, amounted to CNY14,797Mn, which is a very strong liquidity position. Besides, the company has several large projects to be launched in FY2017, which will enable the company to cash out in the near future. Therefore, despite the high net debt to equity ratio, we expect the ratio will drop once the large projects to be launched in FY2017, such as Logan Carat Complex in Shenzhen and Logan Acesite Park in Shenzhen, which provide a total GFA of 1,560,000 square metres and are expected to bring sizable revenue to the company due to the hot property market in Shenzhen, are completed and converted into cash.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$5.50: Logan Property has achieved a very strong result in FY2016. The strategic positioning of the company in Shenzhen, Foshan and Huizhou has allowed it to directly benefit from the national development strategy of Guangdong-Hong Kong-Macau Greater Bay Region, which will allow the company to achieve long term sustainable growth in the future. We are also optimistic towards the future property development projects of the company because of the excellent location chosen for its property development projects especially those located in Shenzhen, which the projects are located directly above or close to the Metro station. The complete transport infrastructure will allow Logan Property to charge premium prices on the properties. Therefore, we raise Logan Property's target price to HK$5.50, corresponding to a P/E and P/B of 4.48x and 1.06x, with an `Accumulate` rating assigned. (Closing price as at 13 Apr 2017)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()