-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

KPC Pharmaceuticals (600422.CH) - Marketing reforms boosted up rapidly grown results

Tuesday, November 3, 2015  9016

9016

KPC Pharmaceuticals(600422)

| Recommendation | BUY |

| Price on Recommendation Date | $33.670 |

| Target Price | $42.630 |

Weekly Special - 2333 Great Wall Motor

KPC Pharmaceuticals announced that the Company recorded growth of net profit of 40-60% in the previous three quarters, with the net profit of RMB203 million in the same period last year and the earning per share was RMB0.596. The main reason of growth of profit is the implementation of a series of measures including fine-tuned marketing reform, which boosted up the sales growth of various highlighted products. We believe that the Company's marketing reform could bring a new round of growth to the core products of the Company.

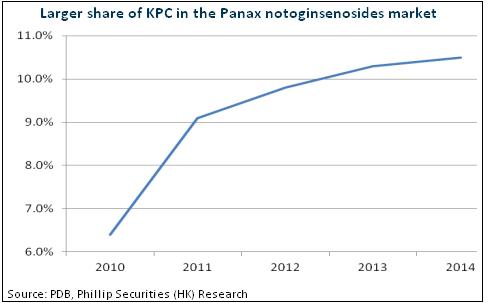

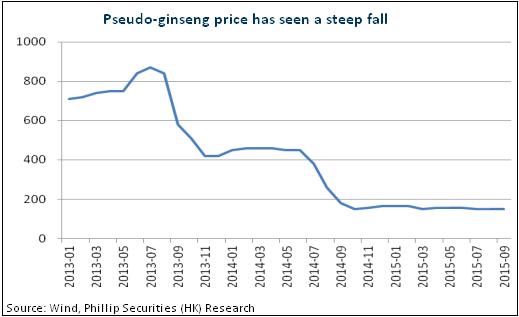

The main products of KPC include three natural botanical drugs, namely Xuesaitong series, Tianxuanqing series and Coartem series. Generally speaking, there is still sufficient growth momentum for the Company's products. Xuesaitong series belongs to of cardiovascular drugs of Panax notoginsenosides group. In the current market of Panax notoginsenosides group, even though the market share of Zhongheng Group is as high as 55%, it is adversely affected by the recent bribery case and thus its market share may shrink in the future. It may be beneficial to KPC which ranks the third in the market currently. It is also worth to note that domestic supply of Pseudo-ginseng nearly doubles the demand and such situation is unlikely to change in short term. The price level of Pseudo-ginseng would remain at low level, which helps to enhance the profitability of products of Xuesaitong series.

This year, KPC adopts the new strategy of positioning itself as a provider of internationalized medicine focusing on cardiovascular drugs and specializing in chronic diseases. The Company would take botanical drugs as its core and comprehensively develop high-end chemical and biological drugs. TEVA is a pharmaceutical company which ranks among the top 20 worldwide. In the 15 years following KPC's acquisition of the rest of 49% equity of Baker Norton, TEVA would still appoint KPC as the sole registered and distribution agent in China. Long term supply agreement would be established. The registration of TEVA's future products in China would still bring considerable growth for KPC. What's more, the Chinese market of diabetes drugs is expected to have persistent fast growth. KPC is now entering the innovation of diabetes drugs and future development should be promising.

Increased shareholding by management demonstrated confidence on the Company

KPC Pharmaceuticals's main business of original natural botanical drugs demonstrated steady internal development and the marketing reform is expected to enhance sales of products. In addition, the price of raw material of Pseudo-ginseng still maintains at low level, so the Company's performance could keep fast growth. Meanwhile, the Company has specific strategical transformation and goals for external development. Therefore, sustainable long-term development would be expectable. Recently, the executives and management level of the Company increased their holding of the Company's share at the price of around RMB30. Such act reflected that all members of the Company had strong confidence on the future development. We set the target price at RMB42.63, which is correspondent to 40x of 2015e EPS, and maintain the rating of “Buy”. (Closing price as at 30 Oct 2015)

Marketing reforms boosted up rapidly grown results

KPC Pharmaceuticals announced that the Company recorded growth of net profit of 40-60% in the previous three quarters, with the net profit of RMB203 million in the same period last year and the earning per share was RMB0.596. The main reason of growth of profit is the implementation of a series of measures including fine-tuned marketing reform, which boosted up the sales growth of various highlighted products.

Since 2013, the marketing reform of KPC is divided into two areas, namely internal and external. Internally, the Company implemented departmentalization by products, including Luotai(Xuesaitong), Tianxuanqing, Xuesaitong soft capsules, special oral medication and generic drugs, and flattened the organization structure of the Company. What's more, the Company's mode of promotion changed: from province-level agents narrowed down to city/county-level. In some key markets, it even specified to a single or several hospitals. The Company also re-developed the market niche not yet covered by the province-level agents previously, dismissed the agents with unsatisfactory business results, and also strengthened the academic support for the agents. By adopting progressive adjustment of salary system for frontline sale teams, income is more closely related to business results, and thus initiativeness of staffs is enhanced. Middlemen were eliminated in the sales channels through serial reform and transaction cost was reduced and the Company's profitability was boosted. This also improved the Company's ability to control the market end, and at the same time, broadened the coverage of the Company's products. We believe that the Company's marketing reform could bring a new round of growth to the core products of the Company.

Market share of product line of Xuesaitong is expected to expand

The main products of KPC include three natural botanical drugs, namely Xuesaitong series, Tianxuanqing series and Coartem series. Generally speaking, there is still sufficient growth momentum for the Company's products.

Firstly, Xuesaitong series belongs to of cardiovascular drugs of Panax notoginsenosides group. With the aging population and the change of diet structure, the prevalence rate and the mortality rate of cardiovascular diseases demonstrated an uptrend in China. Thus, the market for cardiovascular drugs is expanding consistently. Moreover, cardiovascular diseases are chronic diseases which require long-term use of drugs. The side effects of processed traditional Chinese medicine are limited and it is a distinguish advantage. In terms of market structure, there are only two producers to produce Xuesaitong (freeze-dried powder for injection) and Xuesaitong soft capsules and this creates an advantageous oligopoly market. In addition, in the current market of Panax notoginsenosides group, even though the market share of Zhongheng Group is as high as 55%, it is adversely affected by the recent bribery case and thus its market share may shrink in the future. It may be beneficial to KPC which ranks the third in the market currently. It is also worth to note that domestic supply of Pseudo-ginseng nearly doubles the demand and such situation is unlikely to change in short term. The price level of Pseudo-ginseng would remain at low level, which helps to enhance the profitability of products of Xuesaitong series.

Secondly, Tianxuanqing series mainly applies to neurological diseases. Being the innovator of research and production of Tianxuanqing, the Company has a market share of 40%, which ranks the top in the market, with a rate of increase of more than 15%. The current points of sales mainly concentrate in Jiangsu Province, Shaanxi Province, Beijing and Yunnan Province etc. There is still much room for development in other areas. The Company is putting effort on promotion to hospital clients, the growth rate is expected to increase in the future. Moreover, the Company's Tianxuanqing gastrodin injection is the only brand having rewarded the qualification of excellent quality and excellent price. Its price doubles the ordinary gastrodin injection and has advantages in clinical promotion. The Company solely sells Acetagastrodin tablets, which have price differentiation from the other ordinary gastrodin tablets.

Last but not least, Coartem is a kind of artemether drugs, which is the most effectively drugs to treat malaria up-to-date. The Company is the largest producer of artemether and related products worldwide, owning the whole supply chain of artemether including plantation, production, international sales network. Due to the current overcapacity, the utilization rate is merely 20%, and the price level of raw drug materials is also low. In the future, when the Company's medicine like artemether injection get the recognition by WHO, new growth would be brought to the Company and the profitability is expected to be improved.

New strategy would focus on chemical drugs and biological drugs

This year, KPC adopts the new strategy of positioning itself as a provider of internationalized medicine focusing on cardiovascular drugs and specializing in chronic diseases. The Company would take botanical drugs as its core and comprehensively develop high-end chemical and biological drugs. Therefore, the board of directors appointed Dr. Dai Xiaochang to be the new CEO. This would make the core management team more international.

Furthermore, being the sale channel of KPC's chemical drugs, Kunming Baker Norton originally was the joint venture of KPC and the international pharmaceutical giant, TEVA. The Company has recently acquired the rest 49% equity and now possesses 99% equity of Baker Norton. Since its establishment, Baker Norton followed the marketing mode of international pharmaceutical companies and made use of its international background and the advantage of marketing network. Baker Norton also continually introduces overseas products and acts as the agents, including alfacalcidol soft capsules, amoxicillin and azithromycin etc. It is worth to point out that TEVA is a pharmaceutical company which ranks among the top 20 worldwide. In the 15 years following KPC's acquisition of the rest of 49% equity of Baker Norton, TEVA would still appoint KPC as the sole registered and distribution agent in China. Long term supply agreement would be established. The registration of TEVA's future products in China would still bring considerable growth for KPC.

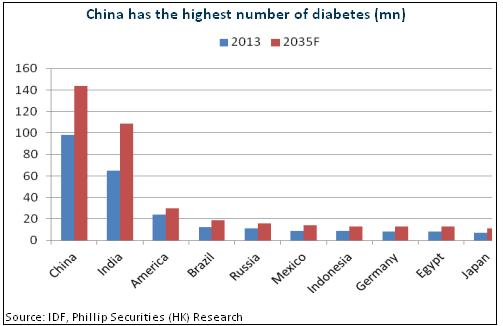

In the area of biological drugs, the Company planned to devote RMB83.13 million in a collaboration with Professor Wang Qing-hua on the development of a high-end long-lasting hypoglycemic drug namely GLP-1. It marks the Company's entering the market of diabetes treatment and development into the area of biopharmaceutical. Currently, China has the highest number of diabetes, accounts for 25% of the worldwide diabetes cases. However, the total expenses of diabetes treatment merely account for 7% of the worldwide sum. Treatment expenses per capita in China only account for 27% of the worldwide per capita expenses. Therefore, the Chinese market of diabetes drugs is expected to have persistent fast growth. KPC is now entering the innovation of diabetes drugs and future development should be promising.

Catalyst

Better-than-expected sales of drugs;

Faster-than-expected progress of acquisition.

Risks

Price drop of drugs;

Monitoring policies on Chinese medicine injection;

Price of Pseudo-ginseng stops declining and starts increasing.

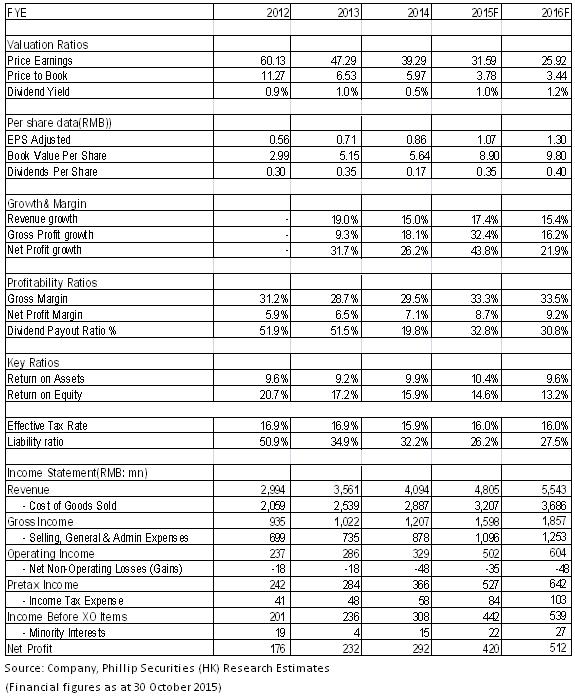

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()