-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Friendtimes (6820.HK) - FoE has set highest monthly revenue record, the company has a strong pipeline in the upcoming years

Monday, April 26, 2021  5931

5931

Friendtimes(6820)

| Recommendation | Buy |

| Price on Recommendation Date | $2.630 |

| Target Price | $3.530 |

Weekly Special - 002050 Sanhua

Investment Summary

The company's 2020 result is in line with expectation

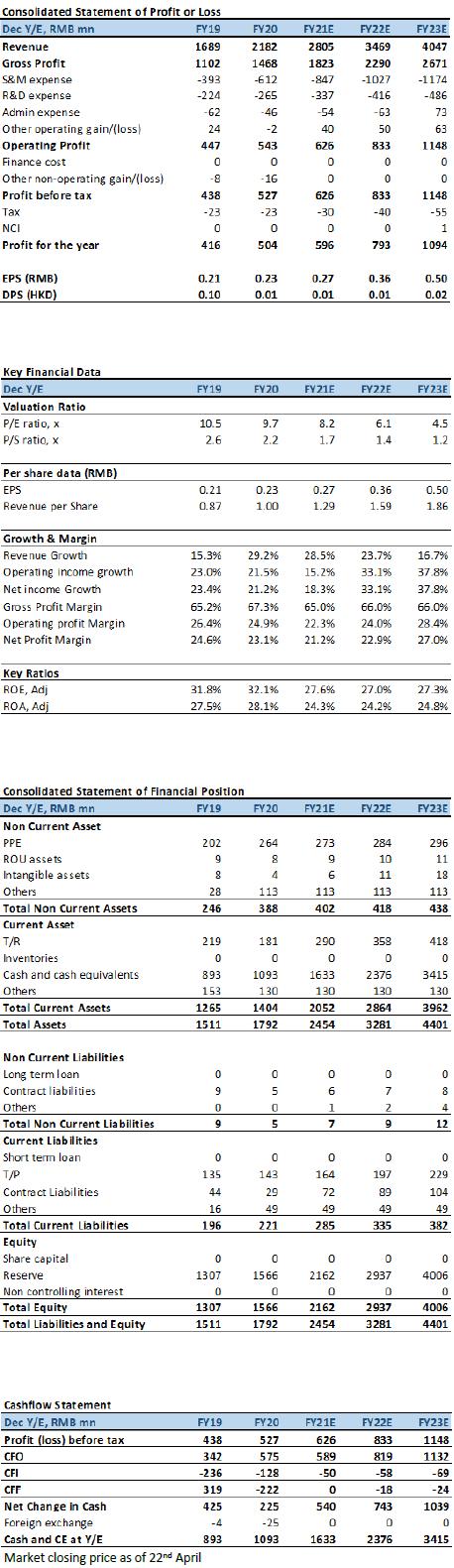

The company's 2020 result meets our previous expectation. The revenue for 2020 was RMB 2.18 billion (+29.2% YoY). The YoY rise was mainly driven by the strong performance of The Fate of the Empress (浮生為卿歌). In terms of the geographical breakdown, the revenue generated from China region and overseas region were RMB 1.71 billion (+53.0% YoY)/RMB 0.47 billion (-17.7% YoY), respectively. As at 31 December 2020, the company has released and is operating 34 mobile games in different languages worldwide, and the accumulated total number of registered users reached 130.8 million (+21.2% YoY). Further, the company has strengthened its monetization ability in 2020, the monthly average revenue per paying user (ARPPU) in 2020 was RMB 715.5 (+34.6% YoY).

The company's 2020 GP was 1.47 billion (+33.2% YoY), with a GPM of 67.3% (+2.0ppts YoY). The 2020 S&M expense was RMB 0.61 billion (+55.7% YoY), with expense ratio of 28.1% (+4.8ppts YoY). The increase in both S&M expense and expense ratio in 2020 was mainly attributable to the fact that the 1) the company had no new title launched in 2019, hence the 2019 S&M expense was at a low cardinal number 2) the company has invested a lot on the promotion of The Fate of the Empress (浮生為卿歌) in 1H20. The 2020 R&D expense was RMB 0.26 billion (+18.4% YoY), with respective expense ratio at 12.1% (-1.1ppts YoY). The 2020 admin expense was RMB 46.33 million (-25.4% YoY), with respective expense ratio at 2.1% (-1.6ppts YoY), The drop in both admin expense and admin expense ratio YoY were because the admin expense in 2019 included some one off items such as listing expenses. The company recorded a NP of RMB 0.50 billion (+21.2% YoY), which is in line with our forecast of RMB 0.52 billion.

The Fate of the Empress (浮生為卿歌) set highest monthly revenue record for the company

The Fate of the Empress (浮生為卿歌) was launched on 31th December of 2019. After the launching, the game has achieved impressive results in terms of the grossing. The game has set the highest monthly revenue for a single product of the company in 2020. On the other hand, the game's highest record was ranked the 5th place in China's iOS Top Games. It ranked the 20th place in China's iOS Top Games on average in 2020, demonstrating its strong stability. Apart from its strong performance in the China region, the game's performances in overseas regions were also eye-catching. The game was launched in Korea in June 2020, and the highest ranking reached 15th place in South Korea's iOS Top Games. As for now, the Fate of the Empress (浮生為卿歌) has been launched in China, Taiwan, Hong Kong, Macau and overseas regions such as South Korea and Southeast Asia and is expected to be launched in Japan and other regions such as North America in the future.

Since the company has adopted the self-distribution strategy for The Fate of the Empress (浮生為卿歌), hence the company has invested a lot on the game's promotion in 1H20 and it took the game nearly 6 months to breakeven. In 2H20, the game has become profitable and has entered its pay-back period as the promotion expense for the game drops. It is expected the margin for the game in 2021 will be higher than that of 2020. With the frequent game updates and optimizations (up to 20 updates in the Chinese version in 2020), we expect the game can contribute stable grossing and NP for the company is the upcoming years.

In addition, the company will focus on the Fate (浮生) series and develop the “Five Episodes of the Fate Series”. The second generation product Code: FS2 (代號:FS2) is under development and is expected to be launched in 2022. Further, the company is interested in cooperating with film production companies to bring its ancient Chinese style creations to the silver screen through licensing, in order to further enhance the influence of the relevant IPs.

The company has a strong pipeline

The company has a strong pipeline. Fate: The Loved Journey (此生無白), a Chinese-style fairy social mobile game will be launched on all platforms in China on 28 April 2021. As of 16th April, the game had a TapTap score of 8.8, with over 57k game reservations. Further, the company's pipeline also included Promise of Lingyun (凌雲諾), a glamorous Chinese-style social mobile game with modern art, and A Story of Lala's: Rising Star (杜拉拉升職記), an authentic inspirational female-oriented stimulation mobile game. Both of the games are expected to be launched in 2021.

Valuation

We continue to be optimistic about the potential of the female-oriented game sector and the company's leading position in the sector. After considered that 1) the grossing of old titles are dropping quicker than we expected 2) the company is expected to launch 3 games in 2021, and the S&M expense tend to be higher at the early stage. We adjust our 2021 NP downward and 2022 NP upward to RMB 596/793 million from RMB 686/766 million and introduce 2023 NP forecast of RMB 1093 million. We lift our 2021 forecast PE to 11x and TP to HKD 3.53, with respective 2021/2022/2023 PE at 11.0x/8.3x/6.0x. We maintain Buy rating. (Market closing price as of 22nd April) (exchange rate: RMB 0.85/HKD)

Risk

1) The tightening on Game regulations

2) The Games underperform comparing to expectation

3) Games launching are delayed due to unexpected reasons

4) Failure in game genre expansion

Financial Statements

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()