-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Youzan (8083.HK) - Take Private Proposal of China Youzan, Proposed Listing of Youzan Technology on HKEX Main board

Friday, March 12, 2021  20020

20020

China Youzan(8083)

| Recommendation | Buy |

| Price on Recommendation Date | $2.630 |

| Target Price | $4.230 |

Weekly Special - 358 JIANGXI COPPER

Investment Summary

Take Private Proposal of China Youzan, Proposed Listing of Youzan Technology on HKEX Main board

The company has announced on the 28th of February, 2021, that the Offeror Betacafe and the company proposed to distribute stocks of Youzan Technology and cash to China Youzan's shareholders. Youzan Technology will be listed on the main board of HKEX by way of introduction. After the distribution of stocks and cash, China youzan will be taken private. According to the proposal, each stock of China Youzan will have the right to claim HKD 0.1352 cash (corresponding to the RMB 2.334 billion valuation of the company's payment and other business) and 0.0508 stocks of Youzan Technology.

According to the valuer JLL, as of 30th of November, 2020, the estimated value of Youzan Technology was RMB 54.1 billion (HKD 64.8 billion), with respective stock price at RMB 35.73 (HKD 42.81). Based on the estimated value of Youzan Technology, the intrinsic value of China Youzan should be HKD 2.3088, which represents a discount of 30.2% comparing to the closing price of 26th of February 2021 (the previous trading day on announcement date), but represents a premium of 12.6% comparing to the closing price of 30th November 2020 (the valuation reference date). We believe that the intrinsic value of China Youzan (HK$2.3088) calculated based on the valuer's valuation is not the actual transaction and market-recognized price. Therefore, the intrinsic price is not very informative. In general, we believe that this transaction solves the company's two major problems, namely 1) the company is listed on the GEM and hence lacks stock liquidity 2) the company is only the controlling shareholders of Youzan Technology (The operating company of the SaaS business, formerly known as Qima Holdings), hence there might potentially be a certain discount on the valuation.

The potential positive factors of Youzan Technology being listed on HKEX main board

1) After Youzan Technology is listed on the main board, the stock liquidity will greatly improve. In addition, based on the current market cap of China Youzan, Youzan Technology is expected to be included in multiple indexes and stock connect trading list soon after its IPO on the main board. The inclusion in the stock connect is likely to introduce mainland investors to contribute the company's revaluation and drive the company's valuation even higher.

2) As of December 31, 2019, the asset value of China Youzan's payment and other business segment was RMB 4.8 billion, while the revenue generated from this segment was only RMB 170 million. The corresponding revenue/asset ratio was 3.6%, which is much lower than the revenue/asset ratio of 31.7% for the company's SaaS business. Therefore, the operating efficiency of Youzan Technology (SaaS business) will be significantly higher than that of China Youzan. On the other hand, despite the separation of the payment business from the listed entity, Gaohuitong, which holds the payment license, will continue to serve Youzan Technology's merchants.

Valuation and Investment Thesis

According to F&S, as of end of 2019, the company has the highest market share among all cloud-based commerce service provider in China, with a market share of 6.3%. We continue to be optimistic about the rapid growth of the cloud-based commerce service sector of China and the company's leading position in the sector.

We maintain our previous financial forecasts of the company and maintain the 2022 target P/S of 27.5. We maintain the target price at HKD 4.23, with respective 2020/2021/2022 P/S at 65.6x/39.9x/27.5x (51.9% of revenue). We maintain the Buy rating. (Market closing price as of 10th March) (exchange rate: RMB 0.85/HKD)

Risk

1) The delay in Youzan Technology listing and take private of China Youzan

2) The expansion of SaaS customers is worse than expected

3) The increased industry competition

4) GMV increase less than expected

5) Merchants renewal rate less than expected

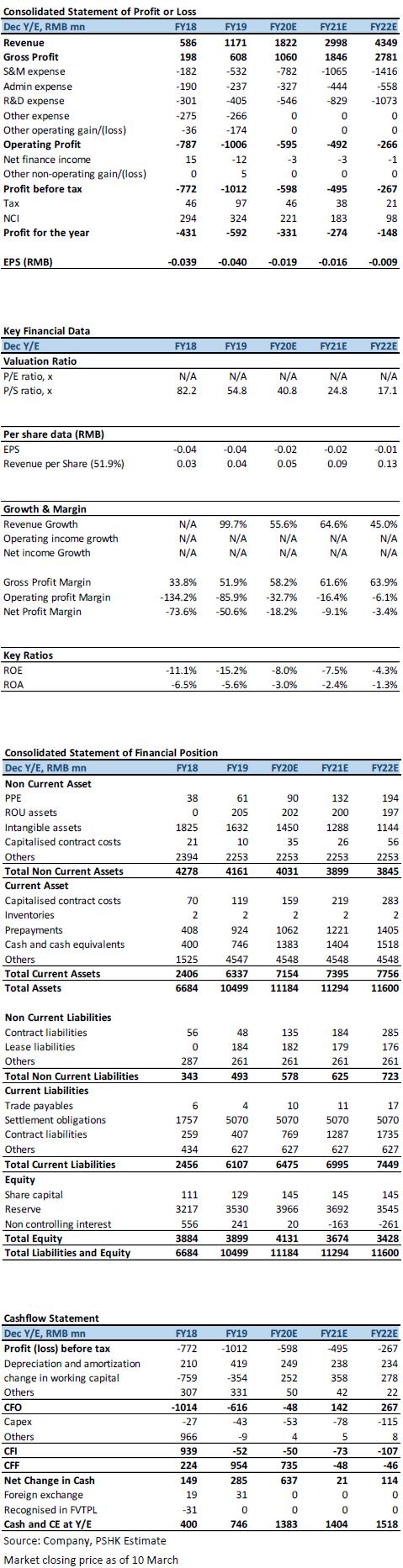

Financial Statements

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()