-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Xtep Int`l (1368.HK) - Three-year rebranding completed, multi-brand strategy launched

Wednesday, September 23, 2020  13425

13425

Xtep Int`l(1368)

| Recommendation | BUY |

| Price on Recommendation Date | $2.330 |

| Target Price | $2.920 |

Weekly Special - 002472.CH Shuanghuan Driveline

Investment Summary

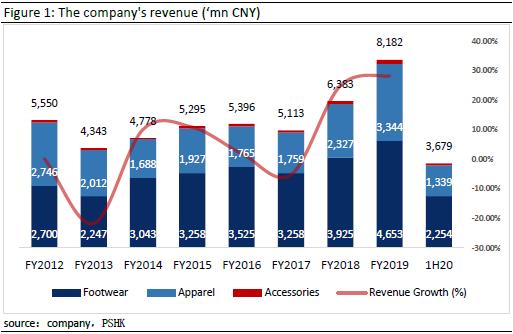

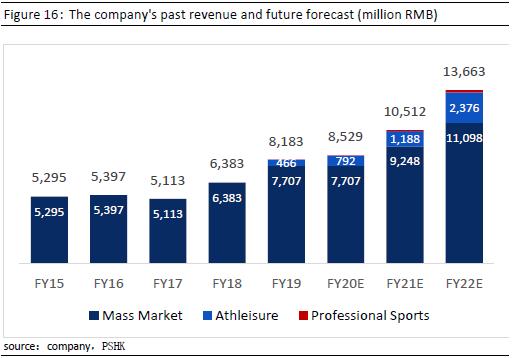

The predecessor of Xtep International was established in Jinjiang in 1987. Like other shoe factories in Jinjiang, it provides OEM services for international sports brands. In 2001, Xtep established its own brand, with fashion sports as its brand positioning, transformed from OEM service provider to a brand owner. It was listed on the Hong Kong Stock Exchange in June 2008. Its main business is the design, development, manufacturing and marketing of sporting goods. The company achieved total revenue of CNY 8.183 billion in FY19, with revenue from sports shoes, apparel and accessories accounting for The ratios were 56.87%, 40.87% and 2.26% respectively. The company's market share ranks third among domestic sports brands and sixth in the industry.

Main brand positioning in running. Multi-brand strategy started

Since 2015, the company has shifted its brand positioning from fashion sportswear to professional sports brand with stylish and functional products, paying more attention to product functionality, building a running shoe matrix covering amateur to professional needs, and reforming the brand over three years. The company established the first domestic running research center in 2016. At the same time, the company adjusted its sales channels, introduced flat channels and the 433 delivery model to improve the company's store efficiency and operational efficiency. After the main brand returned to stability, the company launched a multi-brand development strategy in 2019, and expanded the brand matrix through joint venture operations and acquisitions. Its brands include Saucony, Merrell, K- Swiss and Palladium and other international brands.

1H20 result shows the potential growth in new brand

In the company's FY20 interim results, the company's revenue under the epidemic increased by 9.6% YoY, mainly due to the increase in sales brought to the company by the new brand. In 1H20, revenue from mass sports was CNY 3.201 billion, accounting for Revenue 87.0%, and revenue from athleisure was CNY 459 million, accounting for 12.5% of the company's total revenue in the first half of the year. Another reason for the decrease in revenue from the main brand is that the rent and decoration subsidies to the distributors paid by the company are recorded in the sales in the form of discounts. It is expected that the main brand can maintain double-digit growth in the future, and Palladium will be developed first in the athleisure. The goal is to open 30 new stores in the mainland this year, and it is expected to add more than 100 stores next year. K-Swiss will continue to provide growth momentum for the athleisure business after the brand rectification. The rebranding is expected to be completed in 1Q22.

Valuation and Investment Recommendation

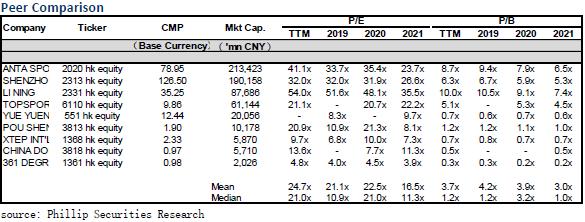

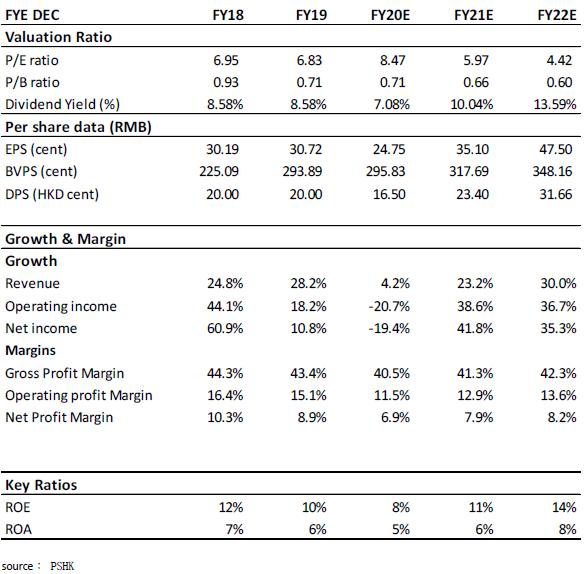

After three years of brand reform, the company's main brand has begun to show initial results. In 2019, it has also begun to actively expand its multi-brand strategy, adding four international brands through joint ventures and acquisitions, and positioning in different market segments. Among them, the four brands have a large potential growth space in the Greater China region. Considering that the current GPM of the company's new brands is low, in the future, the DTC model can effectively increase the GPM to 50-60%, and the potential growth is huge. It is estimated that the company's EPS for FY20E/FY21E is CNY 24.75/35.10 cents, giving the company a target price of CNY 2.92, P/E corresponding to the FY20E/FY21E 10.62x/7.49x.

Company Profile

The predecessor of Xtep International was established in Jinjiang in 1987. Like other shoe factories in Jinjiang, it provides OEM services for international sports brands. In 2001, Xtep established its own brand, with fashion sports as its brand positioning, transformed from OEM service provider to a brand owner. It was listed on the Hong Kong Stock Exchange in June 2008. Its main business is the design, development, manufacturing and marketing of sporting goods. The company achieved total revenue of CNY 8.183 billion in FY19, with revenue from sports shoes, apparel and accessories accounting for The ratios were 56.87%, 40.87% and 2.26% respectively. The company's market share ranks third among domestic sports brands and sixth in the industry.

Company development process

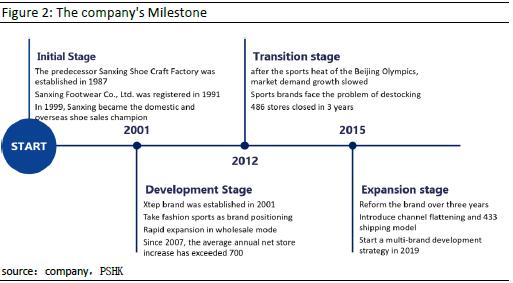

Initial stage: 1987-2000

The predecessor of the company, Sanxing Shoe Manufactory, was established in 1987, and Sanxing Shoes Manufactory Ltd. was registered in 1991. The main business is to provide OEM services for internationally renowned brands, and the products are sold to more than 40 countries and regions. The company introduced modern technology in 1997 to form a one-stop production system. In 1999, Sanxing became the domestic and overseas shoe sales champion. It has 45 factories and employs nearly 4,000 employees in Jinjiang.

Development stage: 2001-2011

Xtep was established in 2001, with fashion sports as its brand positioning, and it was the first domestic sports brand focusing on fashion sports. At the beginning of the brand establishment, the company used entertainment stars as endorsements of sporting goods. Unlike other brands endorsed by athletes at that time, it signed contracts with famous idol stars such as Nicholas Tse, Twins, Boy`Z, Wilber Pan and Jolin Tsai. The company also increased its brand awareness by sponsoring popular variety shows at the time. During this period, the company began to switch from export sales to domestic sales. At the same time, it also expanded rapidly in a wholesale mode. Since 2007, the average annual net store increase has exceeded 700. Among them, there were more than 1,000 new stores in 2008, the highest since its listing.

Transition stage: 2012-2014

After the sports boom in the Beijing Olympics, the growth of market demand slowed down, which brought the extensively developed sporting goods industry into an adjustment period, and all sports brands faced the problem of destocking. Xtep controlled inventory levels through order control and increased discounts, and at the same time adjusted channels to optimize operating efficiency, closing 486 stores in three years.

Expansion stage: 2015 to present

Since 2015, the company has shifted its brand positioning from fashion sportswear to professional sports brand with stylish and functional products, paying more attention to product functionality, building a running shoe matrix covering amateur to professional needs, and reforming the brand over three years. The company established the first domestic running research center in 2016. At the same time, the company adjusted its sales channels, introduced flat channels and the 433 delivery model to improve the company's store efficiency and operational efficiency. After the main brand returned to stability, the company launched a multi-brand development strategy in 2019, and expanded the brand matrix through joint venture operations and acquisitions. Its brands include Saucony, Merrell, K- Swiss and Palladium and other international brands.

Multi-brand strategy launched

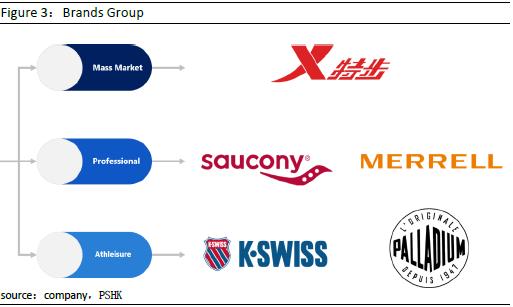

The company currently owns five major brands, positioning three major markets according to product image: mass market, professional market and athleisure market, covering multiple segments such as running, basketball, comprehensive training, tennis, and leisure. The main source of the company's revenue comes from the main brand. In FY19, revenue from the main brand was approximately CNY 7.71 billion, accounting for 94.2% of total revenue, and 97.0% in the first half of 2020. The newly acquired K-Swiss and Palladium are classified as sports fashion markets. They were incorporated into the table in August 2019. FY19 revenue reached CNY 466 million, accounting for 5.7% of the company's annual revenue. Revenue in 1H20 contributed approximately CNY 459 million, accounting for 12.7% of total revenue.

Main brand positioning in mass market

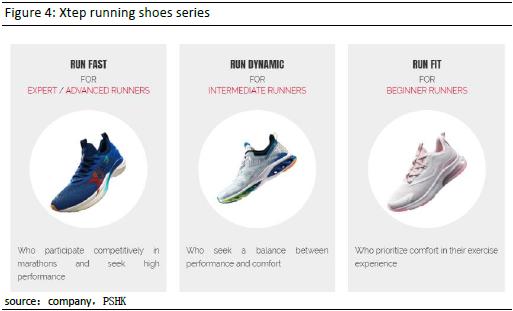

The company's main brand was established in 2001. In 2015, the company carried out a brand reform from fashion sportswear to professional sports brand with stylish and functional products, emphasizing the sports attributes of the products, and developing two series of professional sports and sports life with running as the core. Aiming at being runners` preferred brand.

The main brand is mainly positioned in the mass sports market, with running as the brand's main positioning. It is divided into three series according to user needs: fast running, dynamic running and comfortable and easy running, which respectively satisfy professional/elite runners and ordinary runners. And for junior runners, the pricing is distributed between CNY 259 and CNY 999. In 2020, the China Speed series will be launched, with three running shoes China Speed, China Speed x and China Speed 160x, with prices starting at CNY 399 , CNY 499 and CNY 999 respectively.

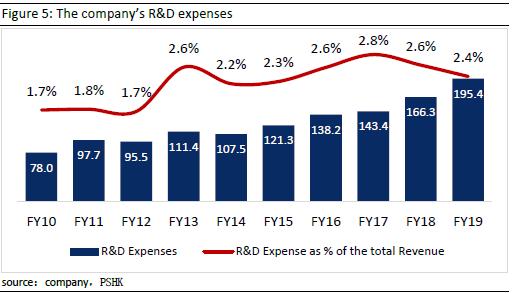

Continue to invest resources in product development

The company's investment in product research and development continues to increase, and in 2016 it began to set up the country's first running exclusive R&D center for shoe design, research and development and testing. A research team composed of more than 40 researchers study foot shape, body shape and gait and other data, through cooperation with leading international fiber material developers such as 3M, Dow Chemical Company, INVISTA, etc., to develop running products suitable for different runners.

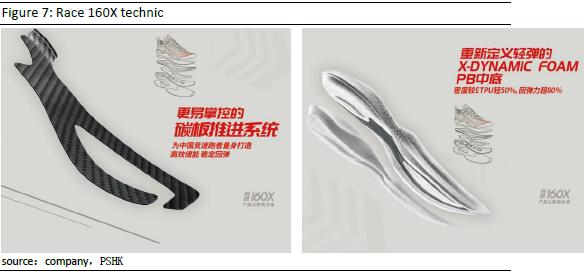

Proven technology with track record

The racing 160X carbon plate running shoes launched by the company at the end of 2019 attracted attention in the domestic running community. At the end of 2019, Dong Guojian ran 2 hours, 8 minutes and 28 seconds in the Berlin Marathon. After 12 years, it became the fourth people in China who ran into the 210 record and achieved China's second best results. The racing 160X uses Xtep's X-Dynamic Foam PB midsole, which is the same material as Li Ning san and Nike NEXT%.

Based on the full palm cushioning propulsion system composed of the racing 160x arc-shaped support plate and the elastic midsole material, Xtep launched the China Speed series in 2020, which is different from the professional racing shoes image of the racing 160x, the China Speed series More suitable for daily use. China Speed 160x is an extension product of Racing 160x. The upper is updated from mono yarn to flying woven upper, and the price is CNY 100 higher than Racing 160X.

Sports + Entertainment, dual-track parallel brand marketing

In terms of brand promotion, the company focuses on the segment of running shoes. Since 2007, it has sponsored marathon events, and the sponsored events have also increased to 53 in 2019. Since 2016, the company has built the first Xtep running club in Beijing Olympic Forest Park, and then established other clubs in Changsha, Hefei, Nanjing, Xiamen and other places to organize more than 2,000 running events, including fun running event Xtep Penguin Run, cooperated with Tencent since 2017. It has deepened the public's positioning of the company as the “Chinese runners` favorite brand”. During the epidemic, in addition to sponsoring the Xiamen Marathon in January, the company also sponsored 5 online events. Participants tracked their performance through fitness apps, attracting nearly 700,000 participants.

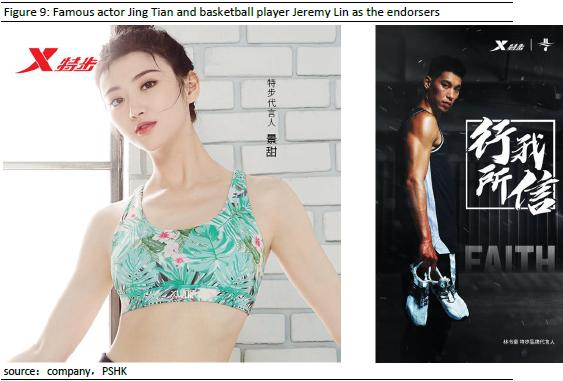

At the same time, the company conducts brand marketing with a dual-track system of sports and entertainment. In addition to sponsoring marathons and running events, the company also has celebrities and key opinion leaders endorsements and other entertainment marketing. The company's brand spokespersons include well-known artists such as Nicholas Tse, Jing Tian and Jiro Wang. In addition, in August 2019, the company hired basketball player Jeremy Lin as the brand spokesperson for Xtep and at the same time as the Xtep charity ambassador to promote basketball. The company start exploring the subdivision of basketball. In addition, the company signed Chinese sprinter Zhou Zheng and marathon athlete Dong Guojian as key opinion leaders to strengthen the professionalism image of the brand.

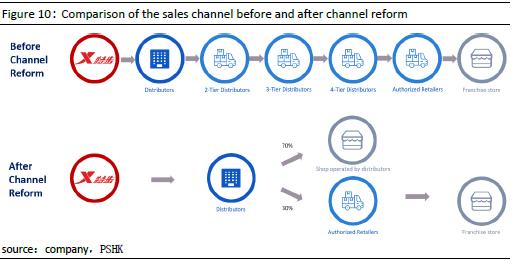

Flatten distribution channels to improve company operating efficiency

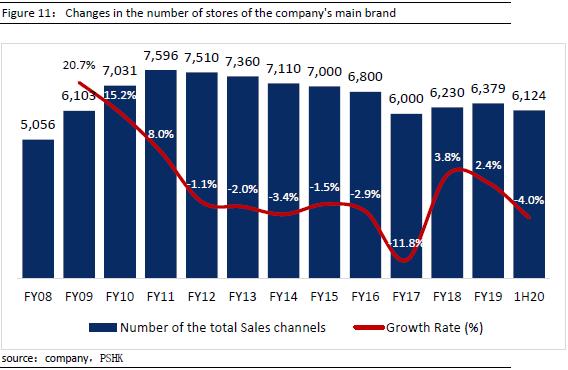

In terms of brand sales channels, one of the company's key reforms since 2015 is to strengthen the management of terminal sales. By encouraging exclusive general agents to turn from distributors to retailers, the distribution level has been reduced from 5-6 levels to at most 2 levels of flat distribution channels now. By mid-2020, 70% of the company's 6,124 stores will be operated by 40 exclusive distributors, covering 31 provinces, with an average of about 1-2 exclusive distributors per province. The company also provides guidance on operations such as store location, decoration and display, product pricing and discount rates.

Industry analysis

The sportswear industry is steadily improving

In the past ten years, the global sports shoe market has steadily expanded, and the concept of national sports has driven the growth of global sports consumption. According to a report by China Forward Industry Research Institute (中國前膽產業研究院), the global sports shoe industry market size has risen from US$66.7 billion in 2010 to US$146.5 billion in 2018, growing at a CAGR of 10.3%, and it is estimated that the market is close to the level of 170 billion US dollars in 2019. Affected by the COVID-19, this year, the sports shoe market is expected to decline in 2020. With the continuous recovery of the world economy, emerging markets with huge consumption potential such as India and China will drive the global economy. The institute also predicts that the global sports shoe market will maintain a medium-speed and steady growth, and is expected to reach a scale of US$379.1 billion in 2025, with a compound annual growth rate of about 18.7%.

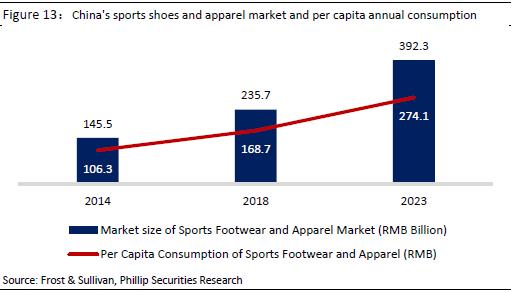

According to Frost & Sullivan's report, in terms of total retail sales (including value-added tax) in 2018, China has become the second largest sports footwear retail market after the United States. The total retail sales (including value-added tax) of China's sports shoes and apparel retail market increased from RMB 145.5 billion in 2014 to RMB 235.7 billion in 2018. At the same time, China's per capita annual consumption expenditure on sports shoes and apparel products also increased from RMB 106.3 in 2014 to RMB 168.7 in 2018, representing a compound annual growth rate of 12.2%. It is estimated that by 2023, total retail sales (including value-added tax) and per capita annual consumption expenditure will reach RMB 392.3 billion and 274.1 respectively. Nevertheless, China's consumption expenditure on sports shoes and clothing is lagging behind other major developed economies. According to Frost & Sullivan's data, in 2018, China's per capita annual consumption of sports shoes and clothing accounted for all types of shoes and clothing. The per capita annual consumption is only 12.5%, while the United Kingdom, the United States and Japan are 27.7%, 31.8% and 24.3% respectively. At this stage, there is still great potential for growth.

Company competitive advantage

The company's newly acquired brands have a long history

In 2019, the company launched a multi-brand strategy. In addition to the original main brand, through joint ventures and mergers and acquisitions, it added Saucony, Merrell, K-Swiss and Palladium to its brand matrix to expand the two markets of athleisure and professional sports.

In March 2019, the company and the Wolverine Group of the United States operated the two major brands of Saucony and Merrell in China, Hong Kong and Macau through a joint venture. Saucony was established in 1898. As a century-old American brand, Saucony and ASICS, New Balance and Brooks are tied as the four major running shoe brands. In 2020, the brand has 12 stores in first- and second-tier cities. Considering that Saucony running shoes are mainly designed by European and American designers, and the design does not fully conform to the foot shape of Asians, the company will also improve the products in China in the future, and will also control the price increase rate in the future to attract consumer. Merrell was founded in 1982 and is a well-known outdoor sports brand in the United States. Its products are mainly outdoor hiking shoes. The two major brands are mainly positioned in the professional sports field. Affected by the epidemic, the company adjusted its annual store opening target to 30-50 in the middle of the year, mainly Saucony.

In August 2019, the company proposed to E-Land to acquire 100% of the K-Swiss and Palladium brands of US$260 million. The K-swiss brand has a history of more than 50 years, and its classic five parallel strips are its product icon. In the future, the company will develop its brand with the positioning of fashion sports, and rebrand from brand positioning, marketing, research and development and product innovation. K-swiss will target the first-tier cities in mainland China and develop in the form of independent stores. As of June 30, 2020, K-swiss has 42 self-operated stores in the Asia-Pacific region. Palladium was founded in 1947 as a French military boot brand. It combines military boots with fashionable and casual elements. It has sales outlets in more than 80 countries around the world, and mainly wholesales in Europe and the United States. At present, part of the domestic stores are operated by E-Land as an agent. At the same time, the company has begun to develop the market in a DTC mode. As of June 30, 2020, Palladium has 31 and 3 self-operated stores in Asia Pacific and Europe respectively.

Financial Analysis

Revenue analysis

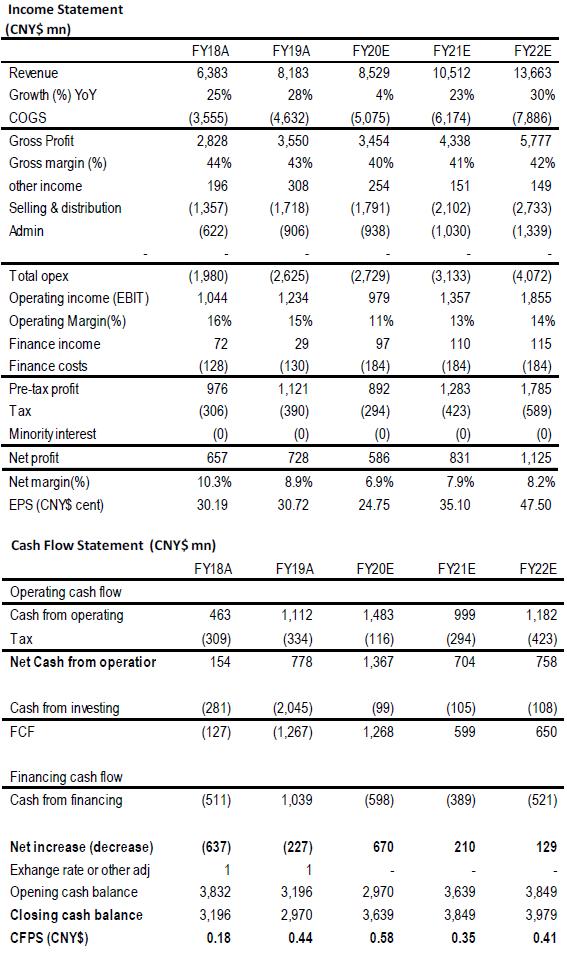

The company started its brand reform in 2015. After three years of reform, the company's revenue recorded significant growth during the past two years , with revenue growth of 24.83% and 28.19% in FY18 and FY19, respectively. The company's total revenue increased from CNY 5.295 billion in FY15 to CNY 8.183 billion in FY19, an increase at CAGR 9.10% . Starting in August of FY19, the company completed the acquisition of K-Swiss and Palladium businesses and merged them into the financial statement. Of the total revenue in 2019, CNY 466 million came from the athleisure business, accounting for 5.69% of the total revenue. Meanwhile the main brand accounted for 94.18%.

In the company's FY20 interim results, the company's revenue under the epidemic increased by 9.6% YoY, mainly due to the increase in sales brought to the company by the new brand. In 1H20, revenue from mass sports was CNY 3.201 billion, accounting for Revenue 87.0%, and revenue from athleisure was CNY 459 million, accounting for 12.5% of the company's total revenue in the first half of the year. Another reason for the decrease in revenue from the main brand is that the rent and decoration subsidies to the distributors paid by the company are recorded in the sales in the form of discounts. It is expected that the main brand can maintain double-digit growth in the future, and Palladium will be developed first in the athleisure. The goal is to open 30 new stores in the mainland this year, and it is expected to add more than 100 stores next year. K-Swiss will continue to provide growth momentum for the athleisure business after the brand rectification. The rebranding is expected to be completed in 1Q22. As of the professional sport, Saucony and Merrell are currently in the early stage of development in the mainland, and it is expected that it will take some time to contribute a significant proportion of the company's revenue.

Profitability

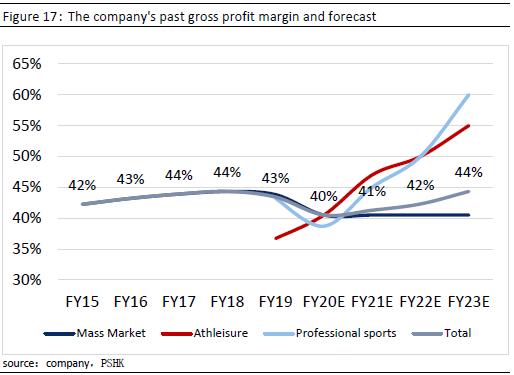

The company's profitability is stable. Before 2018, the company's revenue was mainly based on the main brand. After the brand reform, the average GPM was 43.39%. Because the company developed the main brand in a wholesale mode, the company distributors gave a 38% discount when purchasing. In terms of GPM, it is similar to a sports brand that also focuses on wholesale. In the first half of FY20, the GPM of the main brand dropped by 4.1 percentage points from the same period last year to 40.5%, mainly due to the exchange of Q3 products with agents for Q1 products to ease the inventory pressure of agents, and then sale to other retailers at a discount The business results in lower GPM. The gross margins of fashion sports and professional sports are 40.5% and 38.7%, respectively. Palladium and K-Swiss` overseas businesses are mainly developed in a wholesale mode, while Saucony is currently mainly based on e-commerce, which makes the GPM relatively low. The new brand will develop in the DTC model in China in the future, and the GPM is expected to improve. It is expected that the GPM can reach 50-60% in 3-5 years as the proportion of direct sales increases. The main brand will also adjust the price doubling rate in the future to strengthen brand competitiveness.

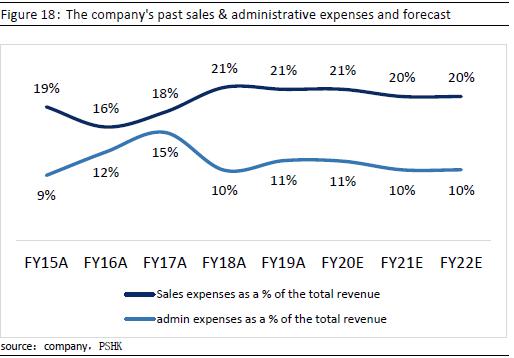

Expenses for the period

After three years of reform, the company's period expense ratio was relatively stable. In 2019, the company's brand acquisition cost the company approximately CNY 100 million, including legal affairs, auditing, inventory impairment, and severance. After the brand reform, the company's sales expenses averaged 21%. In 1H20, due to the epidemic, the company reduced some of its advertising and promotion expenses. Sales expenses in the first half of the year accounted for 18.6%. Administrative expenses account for about 10% of sales and are expected to remain unchanged in the future. In terms of overall sales and distribution, general and administrative expenses, due to the increase in the provision for receivables in the first half of this year, the overall accounted for 29.3% of revenue, which is higher than 27.3% of last year. If the related effects are excluded, the proportion of expenses is lower than that of last year.

Company valuation

After three years of brand reform, the company's main brand has begun to show initial results. In 2019, it has also begun to actively expand its multi-brand strategy, adding four international brands through joint ventures and acquisitions, and positioning in different market segments. Among them, the four brands have a large potential growth space in the Greater China region. In the future, the company will develop brands in the form of direct operation, which is expected to increase the company's current GPM and provide the company with growth momentum from revenue and gross profit. The performance of the first half of the year reflects the growth potential of the company's new brand. However, due to the impact of the epidemic, the company's store opening plan has slowed down, and the store opening plan has been postponed to the second half of the year. It is expected that the company can grow rapidly with new brand strength after the epidemic.

Considering that the current GPM of the company's new brands is low, in the future, the DTC model can effectively increase the GPM to 50-60%, and the potential growth is huge. It is estimated that the company's EPS for FY20E/FY21E is CNY 30.06/35.19 cents, giving the company a target price of CNY 2.92, P/E corresponding to the FY20E/FY21E 10.62x/7.49x.(Closing Price as at 21 September)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()