-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Sitoy Group Holdings Limited (1023.HK) - Fair Valuation

Monday, November 12, 2012  10627

10627

Sitoy Group Holdings Limited(1023)

| Recommendation | HOLD |

| Price on Recommendation Date | $4.730 |

| Target Price | $5.040 |

Weekly Special - 2333 Great Wall Motor

Company Overview

Sitoy Group Holdings Limited (Sitoy) is engaged in developing and manufacturing of handbags, small leather goods, and travel goods on behalf of high-end luxury brands, such as Coach, Fossil, Michael Kors, Lacoste and Prada, and high-end travel brands, such as Tumi.

FY12 Results Highlights

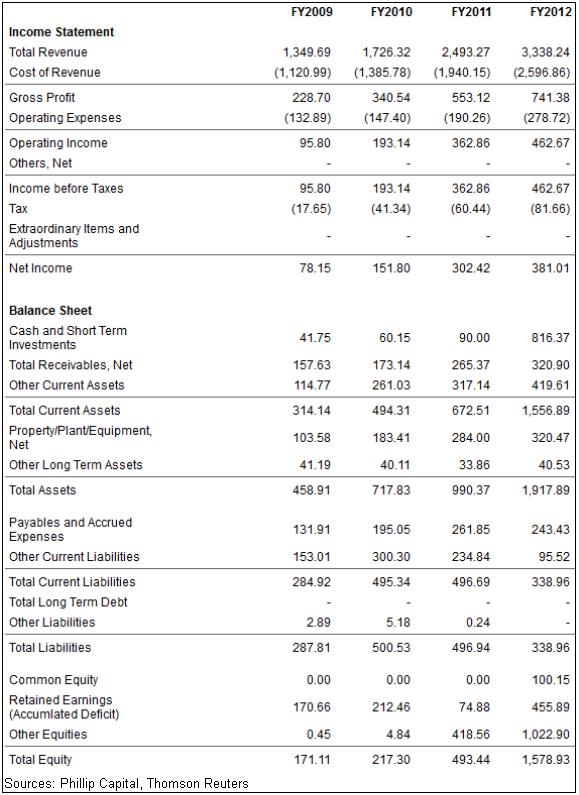

-Revenue soared 33.9% yoy to approximately HK$3,338.2 million.

-Gross profit margin remained stable at 22.2%.

-Direct labor costs surged 40.8% yoy to approximately HK$538.7 million, accounting of 16.1% of revenue. (FY11: 15.3%)

-As at 30th June 2012, total production capacity reached 20.0 million units, with a utilization rate of approximately 80%.

-Net income came in approximately HK$375.3 million, up 18.7% yoy.

Summary

We upgrade our forecast FY13 EPS to HK$0.42 and leading P/E to 12x. The current share price of HK$4.73 and an implied FY2013 leading P/E of 11.26x, representing a 6.6% upside potential. We upgrade our 12-month target price of Sitoy to HK$5.04 with a “Hold” rating.

Robust top line growth

Revenue soared 33.9% yoy to approximately HK$3,338.2 million. This increase was primarily due to an increase in the sales volumes of products to 15.48 million units from 12.28 million units as a result of growing demand from the high-end and luxury brand customers, as well as the start of the retail business in February 2011.

The growth was stemmed from robust sales to North America and Europe market. Revenue from North America soared 34% yoy to HK$2,270.28 million; while revenue from Europe surged 43.36% yoy to HK$ 608.57. The robust demand for high-end and luxury goods, mainly driven by the China market, fueled the demand of the Company's product.

Coach Inc (COH US), who is believed to be the Company's largest customer, recorded a 14.5% yoy growth in revenue and opened 30 new stores in China in FY12. Parda S.p.a. (1913.HK), another customer of the Company, recorded a 36.4% growth in revenue yoy in 1H12, of which the revenue from Asia Pacific market soared 34.7% yoy. As international luxury brands continue to battle for the China and Asia Pacific market, the robust demand of luxury goods will become the cornerstone of Sitoy's prospect.

New production capacity is in the pipeline

Sitoy increased the production line from 191 to 215. Total production capacity of handbags, small leather goods and travel goods increased to 20 million units in FY12 from 16.1 million units in FY11. Utilization rate stretched from 76% in FY11 to 80% in FY12.

The construction of two buildings as part of the phase 2 expansion in Yangde facility was completed in Nov 2011. The Company plans to complete the expansion of the remaining portion of the Yangde phase 2 expansion by 2014. The Company will invest HK$80 million CAPEX on the phase 2 expansion which will bring the total annual production capacity to 22 million units by the end of 2013. Furthermore, the Company expects the total production capacity to increase by 40% to 28 million units upon the completion of Yangde phase 2 construction in 2014. In addition, about HK$25 million will be used for the purchase of manufacturing facilities and upgrade of equipment in 2013.

GPM was stable while NPM squeezed

In our previous report, we forecasted that the hike in labor and raw materials costs would erode the gross profit margin of the Company. In FY12, costs of raw materials totaled HK$1991.99 million, up 31.58% yoy and accounting of 59.7% of total revenue, while direct labor costs came in HK$538.68 million, soaring 40.86% yoy and accounting of 16.1% of total revenue. We were surprised that Sitoy was able to maintain its gross profit margin at 22.2%.

Sitoy explained that the Company deployed a cost-plus business model that can pass the rising cost to its customers. We believe the success of cost-plus business model is highly relied on the limited supply of O.E.M. for luxury goods. Hence, we believe that the Company will be able to maintain its profit margin in near-mid term. However, with the mature of other low-cost production center in Asia such as Vietnam and Cambodia, we believe the squeeze in gross profit margin is inevitable in long-term.

Despite the GPM remained stable at 22.2%, the rising selling expenses dragged down operating margin by 0.8% to 13.9%. Selling expenses accounted for 2.9% of revenue in FY12, comparing with 2.2% a year ago. About HK$21.2 million was spent in the marketing of the retail business. Meanwhile the rising taxation expenses further narrowed net profit margin by 0.7% to 11.4% in FY12. Effective tax rate increased from 16.7% in FY11 to 17.6% in FY12.

Rosy growth in retail business, yet profitable.

In FY12, revenue generated from the retail business was HK$14.4 million; revenue from the 2H12 was 174.1% more than the 1H12. As at 30th June 2012, the Company owned and operated 22 retail stores, among which 6 were stand-alone retail stores and 16 were department store concession counters. Those retail stores spanned across Beijing, Shanghai, Guangzhou, Shenzhen, Hong Kong, Chongqing, Chengdu, Wuhan and Yangzhou, China. The Company aims to open a total of 100 stores by the end of FY15. We expected the Company to focus on opening department store concession as it requires less capital input and mitigates the operating risk of retail business.

Although revenue generated from the retail business was HK$14.4 million, the retail business remained a loss, as the revenue was even not enough to cover the HK $21.2 million selling expenses. We remained conservative whether the retail business will become a profit contributor in FY13.

Debt free position and healthy cash flow

Since the IPO of the Company, Sitoy cleared all its debt and maintain a zero debt balance by the end of FY12. In addition, the Company recorded healthy cash flow from operation since FY09 which we expect to continue. In FY12, although the cash flow from operation reduced due to increase in income tax and working capital, we believe the operational cash flow was strong enough to support future expansion of the Company. Meanwhile, we estimate the Company's CAPEX will be about HK$100 million per year from FY13-14 and the Company plans to pay dividends of no less than 30% of net profit attributable to the share holders, we believe the operational cash flow will be able to cover CAPEX and dividend from FY13-14.

Major risk- Eroding consumer sentiment

The Hong Kong retail sector is a good proxy for the consumer sentiment of China. After years of robust growth in the Hong Kong retail sector, the YTD Sep 2012 data shows that the growth of Hong Kong retail sector began to slack off in 2012. The data from Census and Statistics Department, HKSAR shows that the yoy growth rate of retail sales tumbled in FY12. At this moment we remain optimistic to the Company's prospect as revenue growth of Coach and Prada, major customers of the Company, show no signs of slacking off. However, the full-blown of another round of financial crisis or further erode in consumer sentiment remain the major risk of the Company.

Valuation

We upgrade our forecast FY13 EPS to HK$0.42 and leading P/E to 12x. The current share price of HK$4.73 and an implied FY2013 leading P/E of 11.26x, representing a 6.6% upside potential. We upgrade our 12-month target price of Sitoy to HK$5.04 with a “Hold” rating.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()