-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of Feb. 2015

Monday, March 2, 2015  12744

12744

Report Review of Feb. 2015

Weekly Special - 000157.SZ Zoomlion

Sectors:

Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing), New energy & Environmental Goods (Zhang Kun)

Mainland Financial (Xingyu Chen)

The market was adjusted continually in Feb 2015, the investors hold the conservative investment strategy due to the Chinese Spring Festival, but HSI trended to go up from 24,500 at the beginning of this month to 25,000 currently, up 2.3% approximately. Investors` investment strategy was still conservative, and according to the banks` performance, share prices were adjusted due to the strong growth in recent months, overall, the performance of banks were better than that of HSI.

As at the end of 27th Jan morning, domestic listed banks` share prices increased by 3.0% on average compared with the beginning of this month, only CEB and HRB recorded the negative growth. According to share prices, Stated-owned banks had the better performance, ICBC and CCB's prices grew 4.0% and 5.5% respectively, and BOC's price also increased by 4.9%. Most of joint-stock commercial banks` share prices recorded the lower growth, of which CMB's price increased by 3.8 compared with the beginning of this month, and HRB had the large decrease as 1.4%, meanwhile, HRB's prices also dropped around 0.7%.

According to the banks` operating performances, they still maintain at the stable level, and share price performance is better than HSI, therefore the banks` performance meet our expectation, and we still hold the cautiously optimistic view on the banks` prices in future. Maintain the banking sector on Buy rating.

Mainland Telecom (Fan guohe)

4G market continues to boost. The data shows that the accumulative number of mobile users of China Telecom in January 2015 reached to 187 million and the accumulative number of users of China Mobile reached to 809 million, among which, number of 4G users broke 100 million. The number of mobile users of China Unicom in January 2015 only increased 83 thousand, hitting a new low record. Meanwhile, the shipment volume of domestic cellphone market in January 2015 was 47.061 million, among which, the sales volume of 4G cellphone reached to 36.117 million, accounting for 77% of the total cellphone sales volume.

In addition, QUALCOMM Incorporated monopoly case was closed with penalty of RMB 6.1 billion yuan, and the change of "forced cross-licensing" strategy also made the manufacturers have choices. It is predicted that Huawei, ZTE and other manufacturers will not sign cross-licensing agreement so as to save the expenditures of patent fee. Comparatively speaking, Xiaomi and other emerging manufacturers may need to pay more patent fee.

FDD license has not been issued in 2014. However, considering the problem of balance of industry competition pattern, we predict that the license may be issued very soon in 2015, thus intriguing a new round of industry investment opportunities. Under the big background of information safety, domestication of telecommunication equipment becomes a trend. Besides, cellphone terminal businesses are stepping out of the low ebb, we believe that ZTE Corporation's result will continue to grow rapidly. In addition, based on the rapid advance of 4G network construction, demand of network optimization will start. Hence, actively paying attention to Comba Telecom and other leading manufacturers are recommended. Meanwhile, the rapid promotion of Apple Pay mobile payment model will facilitate the accelerated development of global NFC industry. We are optimistic about the financial electronic payment industry and recommend PAX GLOBAL and so on.

Mainland Property & Oil/Gas service (Chen geng)

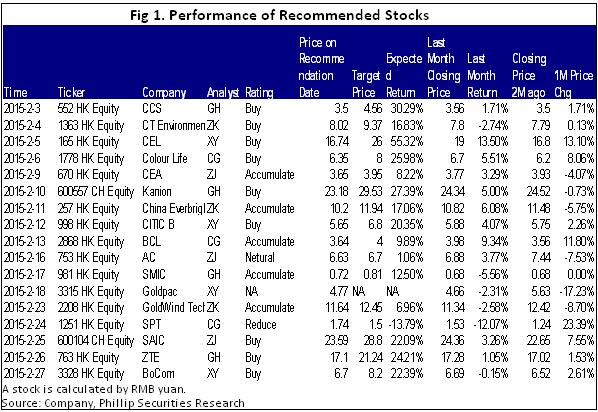

In February, 2015, I wrote three research reports on Colour Life, BCL and SPT, which got success by unique operation model. We recommend “Colour Life”. We expect that larger area of property management, higher commission ratio of service and more revenue of maintenance will promote CAGR of the revenue and profit to reach 78% and 137% in 2013-2015. In addition, the company will enhance the cooperation with IT and internet companies to explore new model on community management, which are optimistic about business transformation and valuation promotion. To sum up, we give Colour Life "Buy" rating, with the target price of 8 HKD for 12 months, amounting to 25 times of the expected P/E ratio in 2015.

Automobile & Air (ZhangJing)

This month we updated 4 equity reports including, China Eastern Airlines (670.HK), Air China (753.HK) and SAIC (600104.CH). We prefer China Eastern Airlines and SAIC with the more attractive future.

As for China Eastern Airlines, the company's first quarter result may see better improvement driven by the robust growth of profitability routes in this Spring Festival like Korean & Japan market, Southeast Asia market, plus with the low fuel price continues. The latter SAIC has extremely appealing dividend payout rate and stable growth ratio (under the new production circle), plus SOE reform expectation.

New energy & Environmental protection (ZhangKun)

In this month, Emerson Analytics, an institution doing short trades, published a report for trading the Sound Global (967.HK) from the short side, and then, the share price of the Sound Global fell significantly, affecting all the companies in the whole sector of sewage treatment. The share prices of these companies also fell by different percentages. After this, the Sound Global published three reports for clarification. Our opinions on this are as follows:

1. The institution of short trading has got no direct evidence to prove its views. The evidence used for the suspicion that Beijing Yipu, the branch of the Sound Global, may be just a shell company was merely the facts that hardly any information related to it could be found on the internet and that Beijing Yipu failed to make timely payment of a sum of social insurance contribution in 2011. It is difficult for such evidence to be convincing.

2. Sound Global does not have significant problems on operation, but defects exist in the internal governance of the enterprise and in some information disclosures and these minor problems become a proverb of the shorting institution.

3. We believe in the future development of Sound Global. This sharp tumble has an obvious influence on the share price in the short term, but in the long run, with the future company management starting up share repurchase program and with the release of the annual report, the market will regain its confidence in Sound Global.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()