-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Teletext

Please enter a stock code or name to get quote details.

| Day High | -- | Day Low | -- |

| Open | -- | Prev. | -- |

| Turnover | -- | Volume | -- |

| Day Change | -- | Lot Size | -- |

| Lot Amount | -- |

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

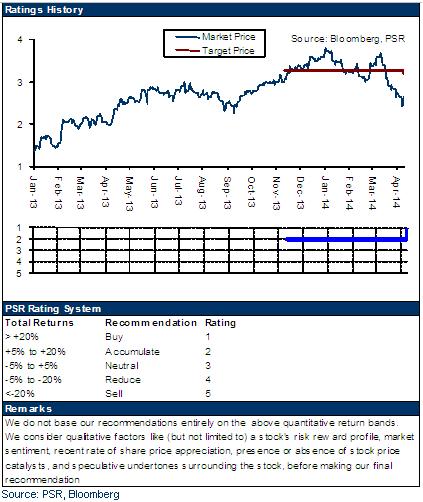

Huaneng Renewables (958.HK) - The layout in the southwest in future

Thursday, April 10, 2014  2584

2584

Huaneng Renewables(958)

| Recommendation | Buy |

| Price on Recommendation Date | $2.640 |

| Target Price | $3.190 |

Weekly Special - 2333 Great Wall Motor

Introduction of the company

By capacity, the company as wind power operator ranks the third domestically and the seventh globally. In June 10th, 2011, the company went public in Hong Kong Stock Exchange. The dominant shareholder, China Huaneng Group, as an electricity generating company, ranks the first domestically and the second globally.

Summary

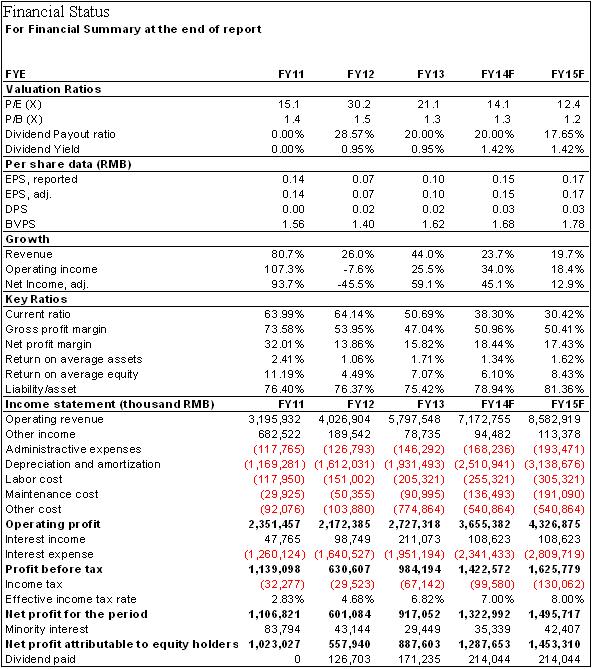

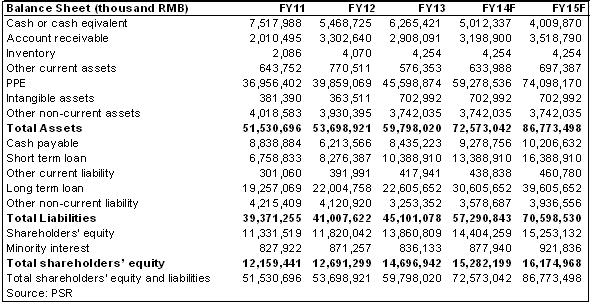

-The Company's revenue achieved to RMB5.8 billion in 2013, up 44.0% y-y, operating profit was RMB2.73 billion, increased by 25.5% y-y, and net profit attributable to the equity holders of the company grew 56.9% y-y to RMB0.89 billion, with the EPS of RMB10.37 cents, and the DPS of RMB0.02 cents, lower than our expectation.

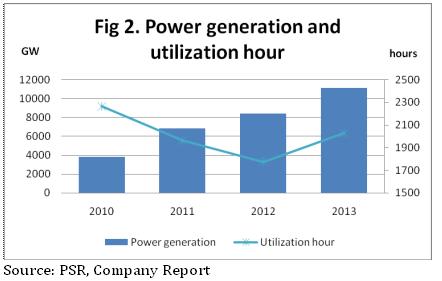

-The total power generation increased by 32.6% y-y to 11,143 GWh, with over 99% of wind power generation, and solar power generation also achieved to 1,198.4 MWh. The growths all exceeded 50% in Inner Mongolia, Shanxi, Guizhou and Shaanxi mainly due to the mitigated grid congestion in Inner Mongolia and the increase of installed capacity in the other three provinces.

-The annual average utilization hours of the Company's wind farms reached 2,029 hours, large increase compared with 1,774 hours in 2012, but lower than the national average of 2,074 hours, the Company's efficiency was close to the national average in recent years.

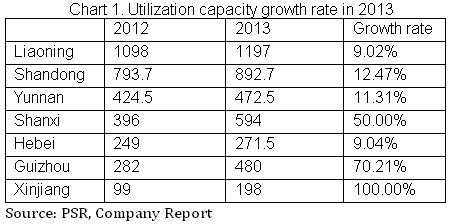

-The Company's installed capacity grew by 1,093.5 MW, including wind power projects of 763.5 MW, solar projects of 330 MW and a total of 6,220.9 MW wind power installed capacity. Newly added wind power installment mainly located at Shanxi, Guizhou and Xinjiang with high generation efficiency, and newly added solar power installment mainly located at Gansu and Qinghai with rich solar resource.

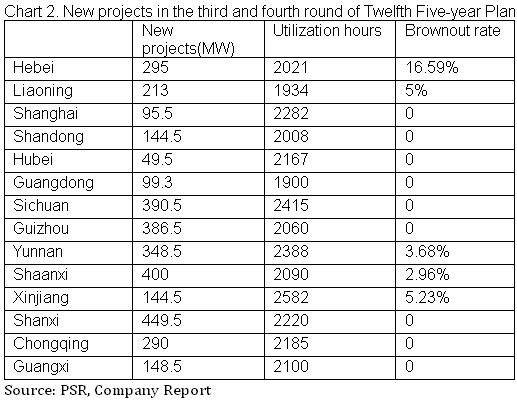

-The Company gained the most wind power projects in the Twelfth Five-year Plan announced by National Energy Administration (NEA) in the third and fourth round, exceeded Longyuan and Datang. Total installed capacity of the approved projects in the third round was 1,631 MW and 97% of the capacity located at no-power brownouts areas. The capacity achieved to 1,915 MW in the fourth round, 92% of the capacity located at no-power brownouts areas. The utilization hours of wind power will again exceed the national average benefited from the operations of these high effective projects.

-A Under the combined influence from nonrecurring items, the company's real profitability is slightly underestimated. The company's liabilities were not serious compared with the peers, total liabilities to total assets ratio decreased continually after 2012, and currently, it recorded net cash with the amount of RMB6.265 billion, which has full capability to develop and construct the large-scale projects.

-The Company gained large-scale projects in 2013, much more than that of Longyuan and Datang, therefore the installed capacity will increase sharply in the next two years, and we estimate the average capacity would achieve to 2 GW, some of them are photovoltaic projects, and newly added projects mostly situated in regions with favorable on-grid access, the Company's generating efficiency will be further increased. Considering the valuations of Longyuan Power (916.HK) and Datang Renewable Power (1798.HK), there is an accelerated growth of the Company's development in future with stronger profitability, and the Company will hold the leading position among the largest three wind power operators. We estimate the Company's target price would be HK$3.19, equivalent to 17/15xP/E2014/2015E, and recommend `Buy` rating.

Top of Page

|

請即聯絡你的客戶主任或致電我們。 市場拓展部 Tel : (852) 2277 6666 Email : marketing@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()