-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Bosideng (3998.HK) - Early winter, and the sinking market continues to release its consumption power

Friday, January 15, 2021  15002

15002

Bosideng(3998)

| Recommendation | Accumulate |

| Price on Recommendation Date | $4.050 |

| Target Price | $4.500 |

Weekly Special - 3306 JNBY Design Limited

Investment summary

The company announced on January 5 the retail performance of the first three quarters of the FY21 (April to December 2020). In the branded down apparel business, based on GMV, the core brand Bosideng increased by 25% YOY, while other brands a YOY increase of 40%+.

The company's brand down income increased while other business income decreased

The company's main down apparel business GMV has grown faster than we expected. Under the influence of the epidemic at the beginning of the year, potential problems such as inventory backlogs have made us more reserved for the company's annual revenue. However, many places across the country entered the winter earlier this year, and the company's discount management controlled appropriately, the adverse effects of the epidemic have been digested in the first half of the fiscal year. In the Q3, the growth rate was significantly higher than that in the 1H21. The company's interim performance report showed that Bosideng/other brand down jacket revenue growth rates in the 1H of the fiscal year were 19.7%/ 2.58%. Based on this calculation, the company's revenue growth rate from down jackets in the Q3 increased significantly.

Double 11 event combined with live broadcast to show the brand new image of the products

In the Q3, the company's online omni-channel sales during the "Double 11" event reached RMB 1.5 billion, ranking second among the apparel brands and first among Chinese apparel brands. During the "Double 11" period, the online retail sales of the company's branded down jackets increased by more than 35% year-on-year. Among them, the online sales of the core brand-Bosideng increased by more than 25% year-on-year. During the event, the company made good use of new promotion methods such as e-commerce live broadcasts, and cooperated with Li Jiaqi, a well-known Taobao e-commercial livestreaming KOL. On October 20, November 2 and November 11, the company entered Li Jiaqi's live broadcast room to meet the target customers and communicate directly. The duration of the live broadcast ranked first in the industry in the live broadcast of Tmall apparel merchants, with a single-day live broadcast viewing volume of 3.56 million. In recent years, the company's main brand has focused on brand rebranding, combining fashion elements with down jackets. During the live broadcast, the company showed consumers a new down series—Light Down Apparel Collection, Outdoor City Collection, and Designer Collaboration Collection, etc., combining fashion and quality Down jackets, refreshing young consumers` inherent image of Bosideng products.

Sinking market consumption power continues to release

Another noteworthy item in the Q3 was the company's other brands of down jacket GMV growth of more than 40%. Since 2018, the company has proposed a strategy of focusing on the main brand, focusing on reforming the main brand, enhancing the brand positioning and filling the blank position in the domestic down market in the middle and high-end market. The blank market after the main brand improved is replaced by the other two brands—Snow Flying and Bengen. Snow Flying is positioned in the mid-end market, with product styles focused on sports and fashion, and its main sales targets are young consumer groups. Bengen is targeting the 25-35-year-old customer group in second- and third-tier cities. In the company's fiscal year 19/20, the revenue of down jackets from other brands accounted for 11.7% of the revenue of branded down jackets and 9.1% of the total revenue. According to statistics conducted by the China Report Hall in 2019, the down penetration rate in China is about 10%, which is lower than the 30%-70% in European and American countries. In recent years, China's sinking market has continued to release its consumption power, which is expected to become another source of company revenue growth in the future.

Valuation and investment advice

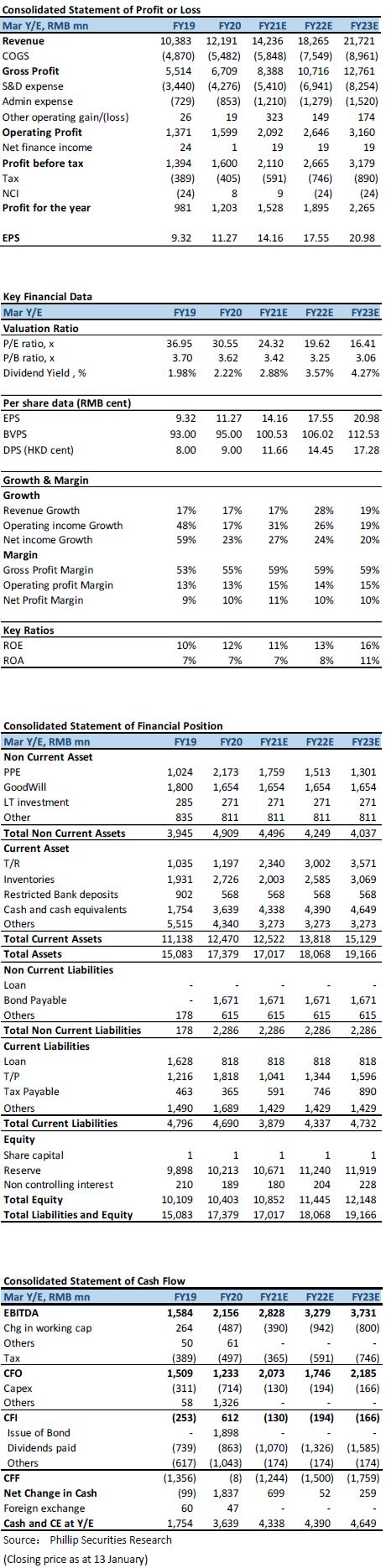

Affected by the La Niña phenomenon this year, the country generally enters the winter earlier, and this year's Lunar New Year's date is later, the entire winter consumption period has been longer than before. In the first half of the year, the company developed self-operated channels under the epidemic situation, and this year's branded down sales started earlier. During the Double 11 event, the company made good use of publicity methods to showcase the brand new Bosideng to the target customer group, and continued to move forward on the road to brand upgrade. Taking the right time and place, Bosideng's operating performance this year has continued to beat market expectations. It is expected that under the cold winter environment this year, the company will continue to grow in the Q4. We further increase the company's FY21E revenue growth forecast of the down apparel business to 25% (previously 20%). The company's FY21E/FY22E EPS is expected to be RMB14.19/17.59 cent. The target price is maintained at HKD$4.50, corresponding to 28.54x/23.00x P/E in FY21E/FY22E. Considering the current price level, downgrade the rating to Accumulate.

Risk

-The development of women's clothing business is not as expected

-Increased industry competition

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()