-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CSPC Pharmaceutical (1093.HK) - Robust sales of innovative drugs

Monday, July 9, 2018  14130

14130

CSPC Pharmaceutical(1093)

| Recommendation | Accumulate |

| Price on Recommendation Date | $21.400 |

| Target Price | $24.800 |

Weekly Special - 3993 CMOC Group Limited

Investment Summary

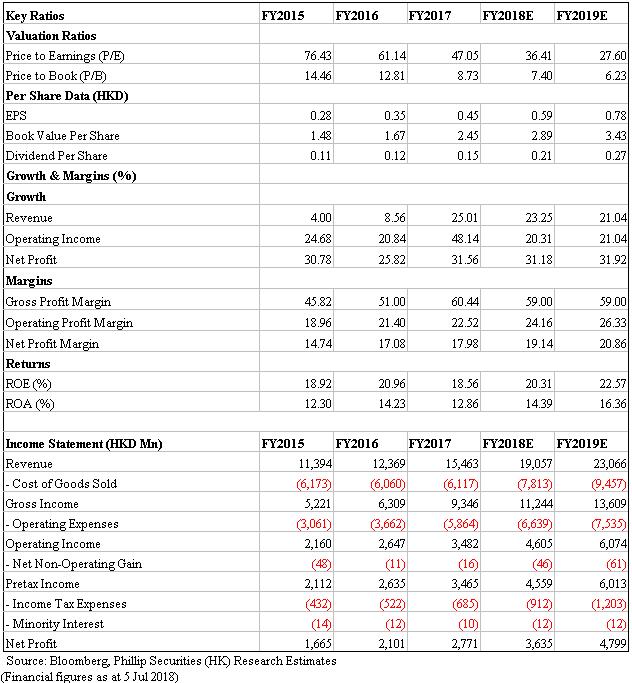

During the last month, the stock price has dropped by ~17%, after which we see Accumulate opportunity. The management maintains annual NP growth guidance of 20-30% intact for future 5 years. We highlight that CSPC as a leading firm among HK listing peers has solid fundamentals and maintain 18E/19E EPS estimation of HKD0.59/0.78 and target price HKD24.8, implying forward PE 36.8x. (Closing price at 5 Jul 2018)

Business Overview

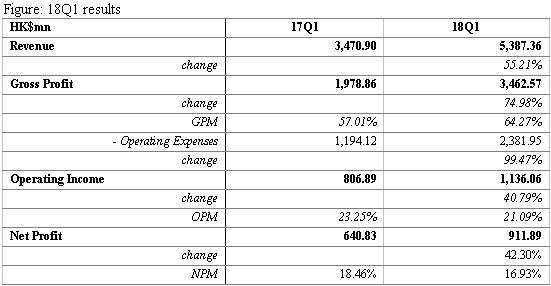

Solid 18Q1 results. The company reported 18Q1 topline growth of 55% (HKD5.39bn) and lower operating income growth of 41%. This is due to rising selling expenses and increasing R&D investment, which led operating margin dropped by 2ppts. While net profit maintains proportionated growth of 42%. We expect the company to achieve good results in first half.

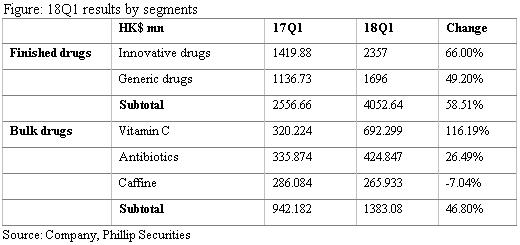

Finished drugs beat our expectations, given notable YoY growth of 58.5%. Innovative drugs (60% in segment income) recorded 66% growth while common generic drugs reported 49% growth. In future, the company will continue to enlarge sales team of innovative drugs, explore blank markets and strengthen academic promotion. On generic drugs, the company targets continuously stable growth through introducing TCM products and pediatric drugs, to build branded generic drugs.Bulk drugs. VC continues to benefit from relatively high price since last year, given Q1 sales was up by 112% which simultaneously contributed to profitability. Antibiotics reported moderate growth of 24% resulting from recovering price. However caffeine generated less profit attributable to rising costs.

Focusing on biotech targets. The company can externally expand through acquiring biotech targets to enrich product mix. Back to the beginning of 2018, CSPC announced acquisition of ~40% interest of a biotech firm. In future, it is expected to seek target firms with relatively mature pipeline of biologic drug products.

Valuation Thesis & Risks

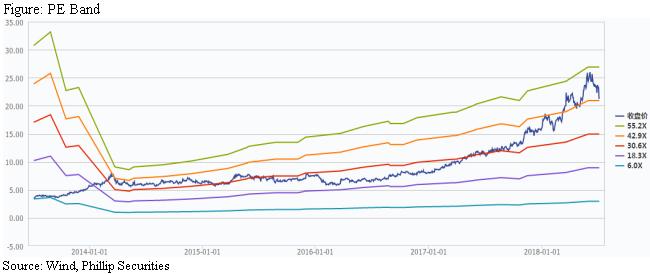

Our model derive TP of HKD24.8: Given recently intensifying short-term volatility, we highlight Accumulate opportunity for medium-term investment. Robust Q1 results enhance our confidence towards 2018 performance, but concerns of rising selling costs and R&D expenses lead to unchanged 18E/19E EPS estimation of HKD0.59/0.78 and target price of HKD24.8, with target PE 42x. Risks include: rising selling and R&D expenditure; M&A or R&D fail expectations; policy risks.

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()