-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CSPC Pharmaceutical (1093.HK) - Some drugs may face price-cut risks while current valuation is attractive enough

Thursday, January 17, 2019  7647

7647

CSPC Pharmaceutical(1093)

| Recommendation | BUY |

| Price on Recommendation Date | $12.060 |

| Target Price | $21.000 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

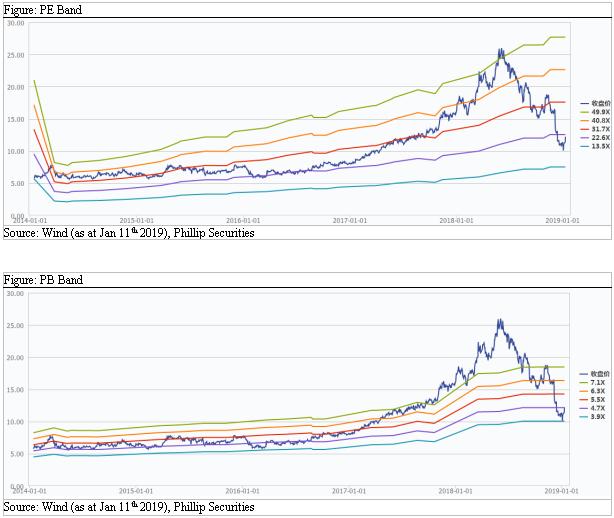

Recently the share price fell to 2017 level, with current PE ratio of 26.5x, which makes the stock attractive, considering CSPC is pharmaceutical leader in HK market. Yesterday, the management stated that in 2019E the group's earnings would increase by 20% to 30%, and the sales of NBP products (恩必普產品) would increase by 25% to 30%. However, as some drugs still have potential price-cut risks in future GPO, we lower 2019 EPS forecast to be HK$0.70, based on 30x target PE, get target price of HK$21.0, and suggest buying during price trough.

Business Overview

2019 growth guidance is announced. The management announced that in 2019E the group's earnings would increase by 20% to 30%, and the sales of NBP products (恩必普產品) would increase by 25% to 30%.

Some products face price-cut risks. We have noticed that in the pilot cities, CSPC abandoned the bid because of the low price in the second round of price negotiations. We thus estimate that CSPC may be barely affected GPO and rapid earnings growth may go on. However, Ou Lai-Ning appeared in the GPO negotiation list in Guangzhou, so we still highlight that there may be potential price-cut risks in future. Therefore, we lowered the revenue forecast of Oulaining and mildly increased the expense ratio to reflect the potential increase in the overall sales expenses.

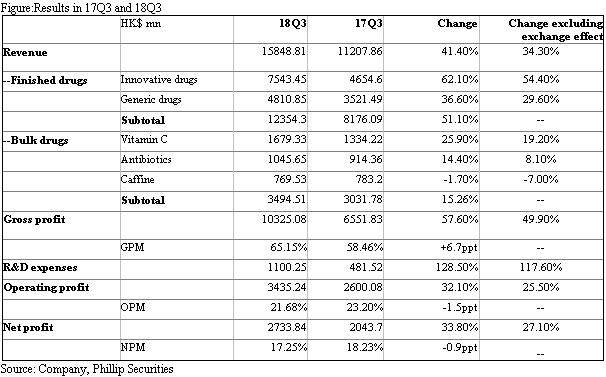

18Q3 growth slowed down. In the first three quarters, the company recorded sales revenue of HK$15.85bn, up by 41.4% yoy (18H1 41.4%), and profit attributable to shareholders was approximately HK$2.73bn, up 33.8% yoy (18H1 41.1%). By business segments, finished drugs remained strong, with sales revenue of HK$12.35bn, an increase of 51.1% yoy. Among them, innovative drugs recorded sales revenue of approximately HK$7.543bn, up 62.1% yoy; generic drugs recorded sales revenue of HK$4.811bn, up 36.6% yoy. On API business, the average selling price of vitamin C remained at a high level, but due to recovering market production capacity and supply, ASP began to fall in the third quarter. The total supply and demand in the antibiotic market is roughly balanced.

Acquired R&D companies and product rights to enhance R&D pipelines. In Jan, one subsidiary, Ouyi, will receive the exclusive development and commercialization rights of Hangzhou Yingchuang to license small molecule products in China and US. CSPC will pay an exclusive license fee of RMB25mn as a down payment and development milestone payments of RMB200mn, and to pay sales royalties based on sales amount. Five innovative oncology small-molecule drug candidates are attained. In addition, the company acquired 100% equity of Yongshun Technology Development Ltd. at a consideration of RMB252.88 mn. Yongshun is mainly engaged in R&D of innovative monoclonal antibodies for targeting tumor antigens and immunotherapy of various kinds of cancers. At present, these three products have received IND approvals from NMPA. The acquisition will help enrich the CSPC's pipeline in the field of biopharmaceuticals and strengthen overall R&D capabilities.

Valuation & Risks

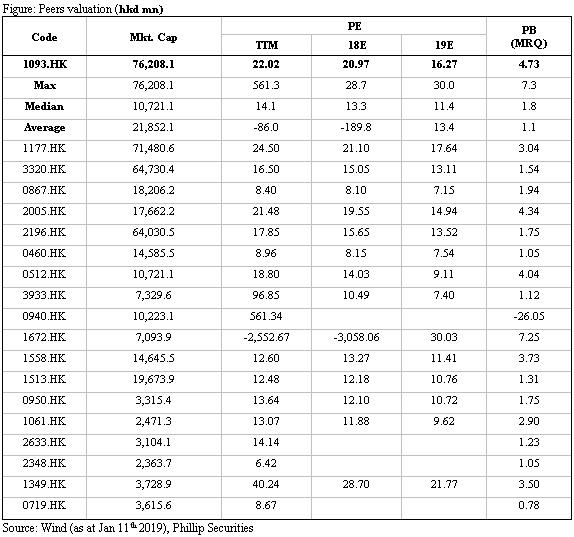

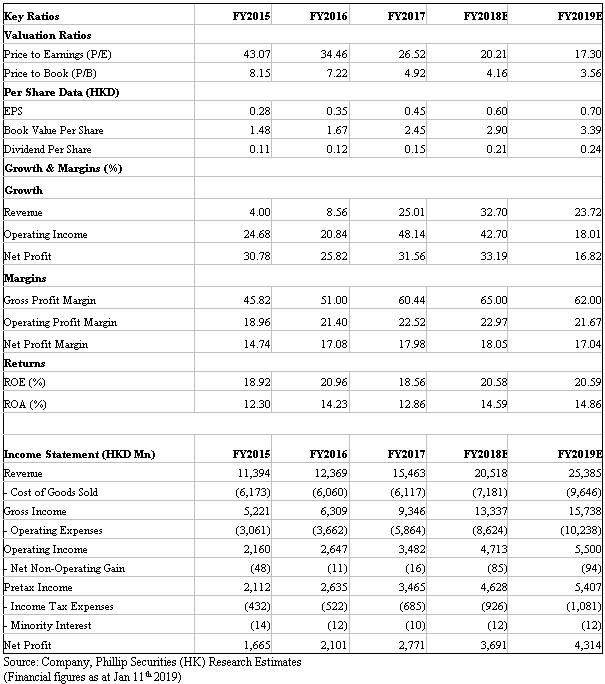

We give 2019 target price of HK$21.0. Current PE is about 26.5x. Considering that CSPC is a leader in Hong Kong stock market, we highlight that the current price is attractive. 19E EPS is forecasted to be HK$0.70, based on a target PE of 30x, and the target price is HK$21.0.

Risks include: risk of drug development failure; sales expansion is less than expected; costs are rising.Figure: 18H1 results by segments

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()