-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

ZFET Co.,Ltd. (002479.SZ) - Slowed down in Q3, yet the growth of annual result can still be expected

Friday, November 17, 2017  15737

15737

ZFET Co.,Ltd.

| Recommendation | Buy |

| Price on Recommendation Date | $10.880 |

| Target Price | $15.000 |

Weekly Special - 3306 JNBY Design Limited

Summary of Investment

-Senior management holds more shares to show confidence, and private placement was approved by the China Securities Regulatory Commission.

-The growth of annual result is highly certain;

Investment Rating

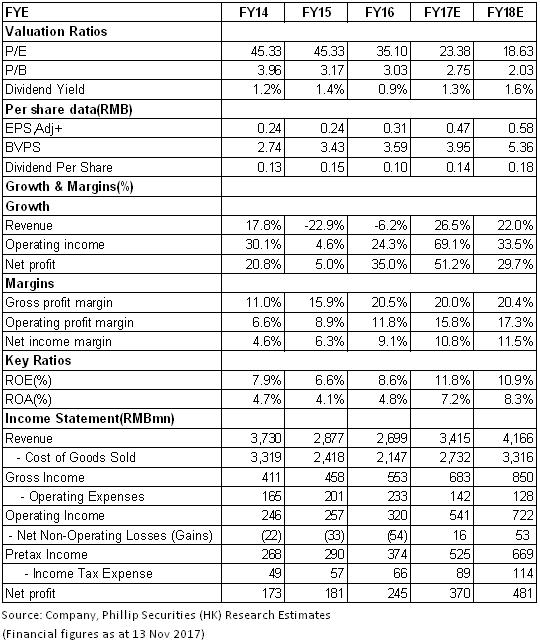

The influence of share issuance isn`t considered temporarily, and it is predicted that the net profits of the Company of 2017 and 2018 will be 370, 481 million; the EPS is 0.47, and 0.48; the P/E ratio will be 23.4 times and 18.6 times, respectively. The rating of "Buy" is given. (Closing price as at 13 Nov 2017)

The net profit declined slightly in Q3. According to the reports of the first three quarters of 2017, FC Environment recorded a revenue of RMB2,476 million, up by about 33% YoY. Net profit attributable to parent company was RMB248 million, up by 37.3% YoY and up by 43.3% YoY after deduction of non-recurring profit and loss. EPS was RMB0.31. Specifically, Q1, Q2 and Q3 reported revenues of RMB793 million (+20%), RMB913 million (+41%) and RMB769 million (+39%), respectively, and net profits after deduction of non-recurring profit and loss of RMB79 million (+87%), RMB113 million (+53%) and RMB49 million (-5.9%), respectively. In general, Q3's revenue grew rapidly, and the net profit decreased slightly YoY. The main reason is the rise of prices of raw materials and the influence of environmental protection supervision on the downstream users` demands.

The Company predicted that the net profit attributable to parent company of the year will be RMB318 to RMB392 million, up by 30%-60% YoY. The annual result growth mainly comes from the facts that the Company has carried out the new Coal Heat Linkage Mechanism in the Fuyang Base and increased the heat supply price, and the productivity of newly constructed project has been gradually released. Correspondingly, in Q4 the Company reported net profit of RMB70 million to RMB144 million, a y-o-y increase of 9.3%-125%, which is higher than that of Q3. It is predicted that the short-term influence of environmental protection supervision will be gradually alleviated, and the downstream users` demands may gradually recover.

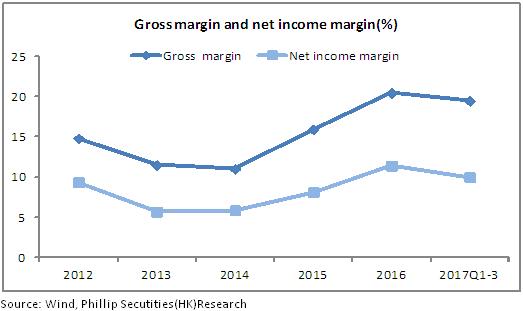

Rise of coal price led to the reduction of gross margin. With regard to profitability, as a result of the rise of prices of raw materials, the gross margin decreased by 2.3% to 19.5% YoY; the net profit is 10%, basically the same YoY. The net cash flow of operating activity decreased by 8.7% YoY, mainly because of the increase of the cash paid for raw materials. Specifically, the net cash flow for the operating activities in Q3 was RMB334 million, up by 60.1% YoY and up by 106% QoQ. Thus, the cash flow-back has improved quarter by quarter.

Senior management consecutively holds more shares to show their confidence in the Company's development. From July to September 2017, the Company's President Secretary Mr. Zhang Jie, Director and General Manger Mr. Zhang Zhongmei and Director Mr. Wu Bin increased total shareholding by 2.6 million shares at the price of 10.86-12.26, namely RMB30 million in total, accounting for 3.26% of the total share capital. The current price has a high safety margin.

Private placement was approved by the China Securities Regulatory Commission. On September 28, 2017, the Company's application for private placement of A-shares in 2016 was examined and approved by the Issuance Examination Commission of China Securities Regulatory Commission. This private placement planned to raise RMB920 million, of which 65% is used for the acquisition of 30% equity interest of Xingang Thermal Power and the Expansion Project of Xingang Thermal Power, and the remaining the Transformation Project of Flue Gas Treatment Technology, and the Technological Transformation Project of Combustion System and the Cogeneration Project in the North of Liyang City. After private placement, it is expected that the Company's revenue and profit scale will largely increase, and endogenous growth can be expected in the long run.

Risk Warnings

Macroeconomic and policy risks;

Risks of rise of coal price and continual decrease of gross margin;

Production of newly added project lower than expected;

Risk of private placement below expectations;

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()