-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Overseas Land Investment (688.HK) - Interim Result Showed Stable Growth

Thursday, September 10, 2015  9070

9070

China Overseas Land Investment(688)

| Recommendation | Neutral |

| Price on Recommendation Date | $22.700 |

| Target Price | $20.800 |

Weekly Special - 000157.SZ Zoomlion

Summary

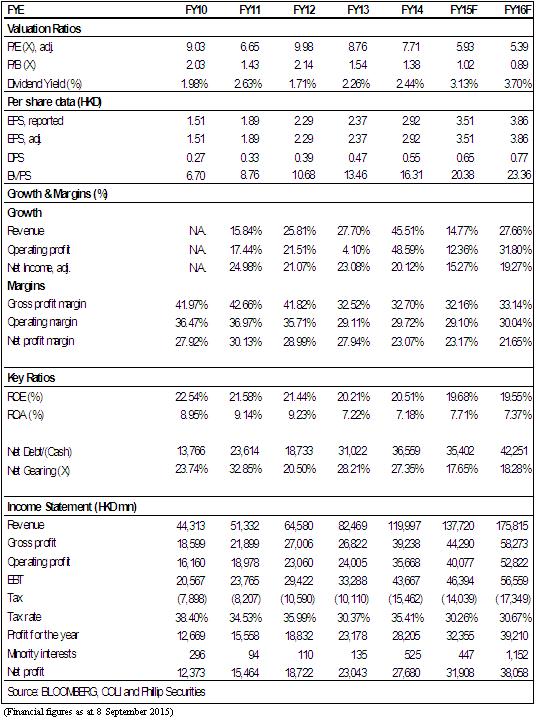

-In 2015H1, benefiting from increased deliverable GFAs, the reported revenue of China Overseas Land (COLI) increased by 19.5% yoy to HKD64.9 billion while its core net profit increased by 20% yoy to HKD13.6 billion. It gross margin was stable at 32%. In H1, revenue from property rental grew by 23% yoy to HKD920 million, mainly driven by increases in rents and occupancy rates. Profit from property rental reached HKD4.26 billion, which included the gain of HKD3.55 billion arising from changes in fair value of investment properties. The core profit of its rental business was HKD710 million, which increased by 16% yoy. Besides, revenue from other operations grew by 32% yoy to HKD1.38 billion, which was mainly generated from the property management business.

-In the first 7 months of 2015, contracted sales of COLI recorded an increase of 16.4% yoy to HKD95.9 billion. Contracted GFAs increased by 29.61% yoy to 6.57 million sq. m. We expect property sales to reach HKD1.1 billion in August, bringing cumulative sales value to HKD107 billion for the first 8 months, which will account for around 60% of its new sales target (HKD180 billion).

-In the coming 4 months, COLI needs to complete a sales target of HKD72 billion, which is equivalent to HKD18 billion per month. Given the traditional peak season of property sales from September to November and that the company has a strong project pipeline for sale, the sales performance of the company in the coming months is worth expecting.

-As of June, the bank balances and cash of COLI amounted to HKD78.6 billion, of which Hong Kong Dollar, Canadian Dollar and Renminbi accounted for 27%, 3.8% and 69% respectively. Interest bearing debts amounted to HKD103.7 billion, of which Hong Kong Dollar, US Dollar and Renminbi accounted for 32%, 46% and 19% respectively. Total net debts amounted to HKD23.1 billion and net gearing dropped from 28% in 2014 to 13.4%, due to more debt having matured in H1, higher cash collection from property sales and lower capex (In 2015H1, additional capex on land acquisitions of the company was just RMB8.3 billion, vs RMB24.5 billion in 2014H1).

-As for the impact of a devaluation in RMB on the fundamental aspects of the company, we expect that the negative impact to be smaller than market expected. Although the company has the largest foreign exchange exposure through its debts (its USD and HKD-denominated debts account for 81% of its total debts, which amount to HKD85 billion), considering the company is holding cash in foreign currency and with an asset size of over HKD50 billion, the actual translation loss of its foreign currency debt exposure is estimated to be around HKD30-50 billion. Besides, this belongs to a long-term foreign currency exposure and spot exposure is limited. As a result, under a scenario of RMB depreciating by 3% per year from 2015-2017, the impact of foreign exchange loss on earnings during the corresponding fiscal years will only be around 5%. Moreover, the dual funding platforms of COLI will also help reduce earnings volatility brought by changes in exchange rates.

-Amid the weak economy, it is quite exceptional for COLI to deliver a solid interim result. In H2, the positive catalysts of the fundamental aspects of the company include a smooth progress in property sales, sales target to be achieved earlier than expected, replenishment of its land bank at lower costs and refinancing of its foreign debts to reduce the negative impact from the devaluation of RMB. Overall speaking, we are cautiously optimistic about the macro environment and the domestic property market, although the overall valuations of the property stocks are already at a relatively low level. We grant an “Neutral” recommendation to COLI, with a 12-month target price of HKD20.8, which is equivalent to 6x and 5.4x of its prospective 2015/2016 PE. (Closing price as at 8 Sep, 2015)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()