-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of August 2013

Monday, September 2, 2013  19231

19231

Report Review of August 2013

Weekly Special - 3306 JNBY Design Limited

Industry:

Local property and Others (Dennis Wu),

Mainland financial, Utilities (Xingyu Chen),

Mainland property, Oil and gas service (Chengeng),

Air, Automobiles, Infrastructure (ZhangJing),

Local Property (Dennis Wu)

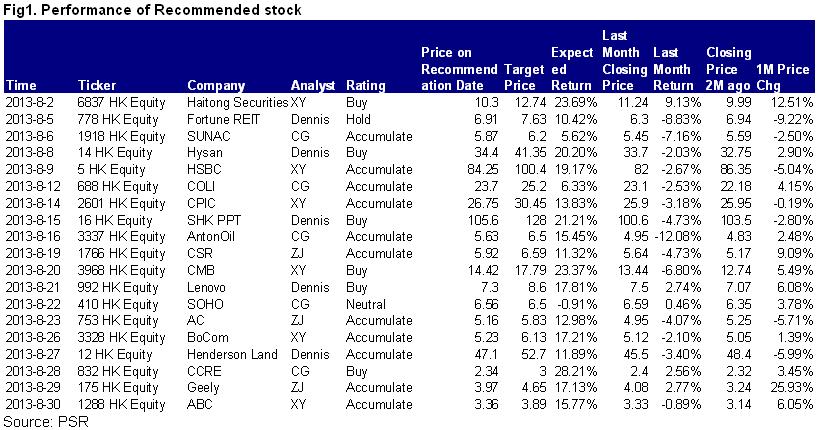

We updated research reports on Fortune REIT (778.HK), Hysan Development (14.HK), Sun Hung Kai Properties (16.HK) and Henderson Land (12.HK) in August.

Fortune REIT (778.HK): For the acquisition of Kingswood Ginza Property in Tin Shui Wai, HK, we think the impact is positive. For the 6 months ended 30 June 2013, NPI of Kingswood Ginza Property was HKD110.4 mn, the implied NPI yield is 3.77% only, but based on Fortune REIT's track records and NT West potential development, we see potential of higher occupancy rate and rents to improve the NPI yield through Fortune REIT's proactive asset management. However, the gearing ratio will jump to 34.5% after financing the acquisition, just below the limit of 35%. It will increase the interest cost largely. We remained the TP of HKD7.63 for valuation.

Hysan Development (14.HK): FY13 interim results beat our expectation: Hysan's revenue came in at HKD1,531 mn, up 38.1% yoy. Underlying profit surged 38.1% yoy to HKD1,033 mn, beat our estimate by 9%. The significant growth was mainly due to rental contribution of HKD366 mn from Hysan Place, higher occupancy rate of retail portfolio after completion of renovations at Lee Theatre Plaza and lower property expenses to revenue ratio. Hysan Place, opened in August 2012, will give full-year contribution in FY13, but even excluding its contribution, Hysan's revenue still rose 14% yoy on a like-for-like basis. The organic growth surprised us.

Sun Hung Kai Properties (16.HK): SHK is now trading at 0.797x P/B and 42.2% discount to our Dec-13 NAV estimate, more than 1 s.d. below the long-term average. SHK is the largest property developer in HK by market capitalization and has many high quality investment properties to support the earnings, we think the NAV discount is too large to reflect the risks of interest rate hike and drop in HK flat prices. We remain our target price of HKD128 based on 30% discount to our Dec-13 NAV estimate. We reiterate "Buy" rating. But we don`t see near-term catalyst for SHK, we suggest investor to buy by phases for long-term investment.

Henderson Land (12.HK): HLD released 1H13 results with underlying profit attributable to shareholders of HKD3.45 bn, down 3.8% yoy and below our estimate of HKD3.95 bn. We want to highlight that the HLD's profit margin of property development in HK dropped to ~20% only, mainly due to the higher construction costs, and it led the underlying profit missed our estimates. But we expect rebound of the margin due to The Reach in Yuen Long expected to be recognized in 2H13. We adjusted down margins forecast and FY13/14 net profit by 4% and 3.8% respectively. Although HLD has better property leasing outlook and smoother farmland conversion progress, we raised the NAV discount to 40% to reflect lower margins in HK development projects and weaker HK residential market. We give a TP of HKD52.70 based on 40% discount to our NAV estimate, with “Accumulate” rating.

Mainland Financial (Xingyu Chen)

HSI showed the adjustment in August after the large rebound in July, by the end of 29th August, HSI decreased by 1.7% slightly to 21,704.78 within one month. During the period, the large weighted sectors such as banking, insurance, and property and so on appeared instable performance caused by the large market volatility. Most of Chinese banks` prices went up slightly compare with the beginning of this month, and their prices increased sharply then dropped immediately at the middle of August.

In this month, the market experienced large volatility mainly because of the “fat finger” incident of Everbright Securities (EBS) at the middle of August. On 16th August, due to the wrong trading order of the arbitrage system adopted by EBS, the prices of the most of blue-ship stocks increased by their daily limit in a very short time, and led the index to jump over 5% within one minute. Although regulatory authorities involved in the investigations immediately and EBS also made an announcement in the afternoon to try to quell the market's concern, the investors held more conservative view on the market's trend, and the index therefore showed the large adjustment after the middle of August.

The trend of H Shares is affected by A Shares obviously. The market held an optimistic view on the banks` performance before because the banks would release the interim results soon, and therefore the banks` prices increased largely in the early of this month, but after EBS's fat finger incident and the announcements of the banks, there are no more good news in the market currently, which then led the prices of the banks to go down in the second half of August.

According to the results of domestic listed banks, the year-on-year growth rate of net profits recorded to 15% approximately in average in 1H2103, and the profit growth rates of joint-stock commercial banks were higher than that of large-sized state-owned banks, and the operating performance met our previous expectation. Therefore, we believe the banks` performances will maintain on stable level in 2013 generally, but the profit growth will decline obviously. Currently, the prices of the most of banks are low with the attractive valuation, and we maintain Buy rating to the banks.

Mainland Property (Chengeng)

In August 2013 I wrote five research reports on Sunac, COLI, SOHO, CCRE and Antonoil, which got success by unique operation model. We recommend COLI. In first half year, sales of COLI accounted for 67% of the sales target of RMB120bn for the year, better than our earlier expectation. We believe that COLI will overfulfill the sales target for the year and consolidate its leading position as the top real property group. We will maintain HKD29 of net assets value per share of China Overseas. It is expected that the 12-month target price will be HKD25.2 with a discount of 13% as compared with NAV, equivalent to 7.9times of expected price-earning ratio in 2014. We keep the “accumulate” rating for COLI.

Automobile (ZhangJing)

In August, we updated 5 research reports including 3 company reports of Geely (175), Air China (753) and CSR (1766). The HSI index experienced an adjustment phase this month, most of stocks therefore entered into the consolidation with the small volatility, and sectors differed. On a closer look, auto sector is benefited from the better-than-expected strong demand of the consumption and most of stocks trended to increase. The trends of air and infrastructure sectors have been static practically due to the instability of macro economy.

We shared our views for China auto industry in 2013H1: The market demand finally started to recovery gradually in 1H2013 from the end of 2012 after China's auto market experienced sharp decrease since 2011, which maintained the increase month by month in terms of the y-y growth rate of industrial sales volumes, in line with our expectation in the previous sector report.

As for passenger vehicles, segments differed: SUV continued to outshine others and small-and-medium (1.0-1.6L) sized cars had the better performance. We attributed the reasons to: (1) Low popularity rate in China's auto market, strong demand of the first purchasing in the third and fourth-tier cities; (2) The demand of the replacement of cars of consumers in the first and second-tier cities. We recommend those growing companies with certain growth of performance meeting the trend of the upgrade and development of consumption, such as GWM (2333), Brilliance Auto (1114), BYD (1211), and we suggest investors to hold such stocks continually, and focus on the companies` core competitiveness and the development of the industry.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()